What we’re reading (3/13)

“Biden Team Scrambles To Contain Financial And Political Contagion” (CNN Business). “The Treasury Department and federal regulators insisted there was no systemic risk to the banking system as a whole that could cause a repeat of the cataclysmic 2008 meltdown as they raced against the opening of Asian markets with measures to head off a run on small or regional US banks.”

“Bank Shares Tumble in Wake of Failures” (New York Times). “The stocks of U.S. regional banks plummeted on Monday as investors reassessed how much such lenders were worth following the recent sudden collapses of Signature Bank and Silicon Valley Bank.”

“Investors Are Searching for Safe Spaces in Banking” (Wall Street Journal). “The megabanks aren’t totally free from worry about the interest-rate risk that was central to fears about Silicon Valley Bank. Many big banks have taken hits to their capital ratios due to rising interest rates and have their own unrealized investment securities losses. But investors appear to feel these banks—having the most resources, the most diverse business units and being the most regulated—are going to emerge as winners.”

“Signature Bank’s Collapse Spells Trouble For Cryptocurrency Industry” (Wall Street Journal). “The bank has long been an integral financial institution for the industry, hosting tools for facilitating digital transactions and counting notable crypto companies, such as the cryptocurrency exchange Coinbase, as its clients. It’s part of a slim group of mainstream banks catering to the needs of cryptocurrency firms and their clients, an area that was upended after the closing of another crypto-friendly bank, Silvergate Capital, last Wednesday.”

“SVB Doesn’t Deserve a Taxpayer Bailout” (Vivek Ramaswamy in WSJ). “Some claim that SVB’s failure would bring down other worthy startups and leave the U.S. less competitive. That’s wrong too. Presumably, these startups’ business models are the same today as they were last week. That means investors could infuse fresh equity capital to make up for any balance-sheet losses. That involves painful equity dilution for founders and venture capitalists, but that’s no justification for a public bailout.”

What we’re reading (3/11)

“Silicon Valley Bank Collapse Sets Off Blame Game in Tech Industry” (New York Times). “For once, the crisis didn’t seem to revolve around a cryptocurrency company. The sudden collapse of Silicon Valley Bank on Friday set off panic across the technology industry. But crypto executives and investors — who have endured a year of near-constant upheaval — seized on the moment to preach and scold.”

“Where Were The Regulators As SVB Crashed?” (Wall Street Journal). “The Federal Reserve was the primary federal regulator for both banks. Notably, the risks at the two firms were lurking in plain sight. A rapid rise in assets and deposits was recorded on their balance sheets, and mounting losses on bond holdings were evident in notes to their financial statements.”

“With SVB It Takes A Village...To Mess Things Up This Badly” (RealClear Markets). “SVB bought my business in 2001 and I worked there as a senior executive for 2 1/2 years. I’ll offer a little insight into what went wrong….Any bank has three main actors; the bankers, the customers (depositors and borrowers, which often are the same), and the regulators. Let’s start with customers, who in this case had to be incredibly naïve and irresponsible to believe deposits in any bank above the insured limit of $250K are riskless. But then VC’s and tech companies have a long history of being terribly neglectful custodians of cash. They believe that their purpose in life is to make great things, and cash management is just a nuisance. The vast majority of responsible corporations and money managers put excess cash in money market programs, which invest in highly-rated, short-term securities like T-bills. In fact, SVB had just such a program that the responsible, non-lazy corporations used, and those funds will be unaffected by the collapse of the bank.”

“Fewer People Are Going To College. That Could Be A Good Thing.” (Reason). “Fewer and fewer young people are enrolling in college after graduating high school. However, while many have presented this decline as tantamount to a national emergency, declining college attendance rates may actually be a good thing. Lower enrollment sends the message that four-year colleges need to lower their inflated prices. Plus, the decline may actually be coming from students who were already likely to drop out of school without a degree. By skipping school, many are saving themselves from accruing unnecessary debt for a degree they likely would never have obtained.”

“Do Non-Profits Drive Social Change?” (Comment). “If high-net-wealth coastal elites donate their money and time to non-profits, surely they must be important. The mainstream media helps cement this image. Ever seen the ‘How to Spend It’ section of the Financial Times, or comparable supplements from the Wall Street Journal or the New York Times? Though most media figures are not high net wealth and have little to do with non-profits, they are pandering to the high-net-wealth crowd. So if the high-net-wealth crowd has a psychological bias toward non-profits, both elite and mainstream media will track and reinforce that trend. These biases deserve to be challenged. Just how important are non-profits really? I think we still don’t know, and I have been involved with non-profits my entire life.”

What we’re reading (3/10): bank run edition

“Silicon Valley Bank Closed By Regulators, FDIC Takes Control” (Wall Street Journal). “Silicon Valley Bank collapsed Friday in the second-biggest bank failure in U.S. history after a run on deposits doomed the tech-focused lender’s plans to raise fresh capital. The Federal Deposit Insurance Corp. said it has taken control of the bank via a new entity it created called the Deposit Insurance National Bank of Santa Clara. All of the bank’s deposits have been transferred to the new bank, the regulator said.”

“Silicon Valley Bank Fails After Run Bby Venture Capital Customers” (New York Times). “If there is one enduring axiom in banking, it is this: Don’t run out of money.

Silicon Valley Bank, a lender to some of the biggest names in the technology world, did just that on Friday, becoming the largest bank to fail since the 2008 financial crisis. The move put nearly $175 billion in customer deposits, including money from some of the biggest names in the technology world, under the control of the Federal Deposit Insurance Corporation.”

“Startup Bank Had A Startup Bank Run” (Matt Levine, Bloomberg). “You are the Bank of Startups, and startups are a low-interest-rate phenomenon…When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off….This is all even more true of crypto — I mean, the Fed raised rates once and the entire crypto industry vanished? — but it is not not true of startups. But if some charismatic tech founder had come to you in 2021 and said ‘I am going to revolutionize the world via [artificial intelligence][robot taxis][flying taxis][space taxis][blockchain],’ it might have felt unnatural to reply ‘nah but what if the Fed raises rates by 0.25%?’ This was an industry with a radical vision for the future of humanity, not a bet on interest rates. Turns out it was a bet on interest rates though.”

“Silicon Valley Bank Is A Very American Mess” (Financial Times). “Despite being the 16th largest bank in the US by balance-sheet size, SVB was apparently not subject to the “no more Dexias, no more HBOSes” regulation. The reason, as implied in the 10-K disclosure above, seems to be that a bank is only required to follow the NSFR and LCR rules if they have a certain amount of “short term wholesale funding”, and SVB’s liability side was dominated by deposits from corporate customers. Of course, as we’re seeing now, the fact that a risk isn’t covered by a regulatory ratio doesn’t mean it doesn’t exist. Although they grumbled and moaned back in the 2010s (NSFR compliance in particular was a big drag on European bank profitability), the European and UK banks basically managed to become compliant with the funding rules, which in many ways just codify sensible treasury management practices.”

“Silicon Valley Bank” (Marginal Revolution). “I am seeing estimates that over 97% of the funds are not FDIC insured, and many of those accounts are held by start-ups. An outright failure would be calamitous for the Silicon Valley start-up ecosystem…Note that every now and then the U.S. banking system is semi-insolvent, but matters work out because “on paper” losses do not have to be either realized or reported as such. Remember the 1980s? One danger is that if other banks start selling their bonds at a loss, the problems in the system will become increasingly transparent and compound themselves. That is not the most likely scenario, but it is something to watch out for.”

“Silicon Valley Bank Has Failed” (The Verge). “Silicon Valley Bank is important for venture capital firms and startups. But as the economy has changed, VC-funded companies burned through their available cash. Simultaneously, VC funding dried up. So Silicon Valley Bank’s deposits dropped faster than the bank anticipated.”

“‘It’s A Big F - - - - - - Mess’: How Silicon Valley Bank’s Collapse Is Creating Chaos” (New York Magazine). “Flow Health runs a network of diagnostic labs and provides COVID testing for clients in the entertainment industry. It’s headquartered in Culver City, California, with offices around the country. It employs about a thousand people, none of whom are getting paid this week. “We just have no way,” says Alex Meshkin, Flow Health’s CEO. ‘It’s a big fucking mess.’ He notified his employees this morning. They’re mad, and with good reason. Many are hourly workers living paycheck to paycheck. Some have threatened not to come to work or to quit. Others are just trying to figure out what the next week looks like. ‘You should see the messages in Slack,’ Meshkin says.”

“Silicon Valley Bank Dies But Its Disease Lives On” (Reuters). “Nearly three years with no U.S. bank failures just came to an unseemly end. Silicon Valley Bank, which counts among its customers half of all U.S. venture-capital backed startups, was taken into receivership by the Federal Deposit Insurance Corp on Friday after a slide in deposits and a hasty capital raising failed to restore confidence. By acting quickly, regulators have stopped one crisis, but may have laid the groundwork for more.”

“SIVB: Held-To-Mortem Governance” (Nongaap Investing). “With Silicon Valley Bank’s well-publicized blow-up underway, a question I have is when did insiders begin to realize they were potentially in trouble? Examining recent disclosures in the 2023 Preliminary Proxy, a governance-based argument could be made insiders were quite aware the situation was serious throughout 2022.”

What we’re reading (3/9)

“Markets Are Telling Investors Two Things At Once” (Wall Street Journal). “There is a big puzzle in today’s market: Treasurys appear to be anticipating a recession, while stocks and corporate bonds aren’t, despite recent falls. How can such big markets be sending such different signals? There are several decent answers—and none of them suggest an easy time for investors.”

“Home Prices Will Grow Again in 2024, Per Report” (UrbanTurf). “A recent survey of housing experts predicts that home prices will bottom out this year and start rising again in 2024. Zillow's latest Home Price Expectation (ZHPE) survey expects home prices to fall 1.6% through December, before rising again annually in the years ahead.”

“The Perks Workers Want Also Make Them More Productive” (FiveThirtyEight). “Three years after the start of the COVID-19 pandemic, remote and hybrid work are as popular as ever. Only 6 percent of employees able to do their jobs remotely want to return to the office full time, according to a Gallup survey published in August. The vast majority of “remote-capable” workers1 want to spend at least some of their workdays at home. When they’re forced to return to an office, they’re more likely to become burned out and to express intent to leave, according to Gallup.”

“Nikkei 225: A Long-Term Technical Pattern Like No Other In The World” (Knowledge Leaders Capital). “The Nikkei 225 (NKY) peaked in December 1989, and in local currency, has yet to reach the previous peak. But, I look at stocks from the standpoint of a US investor, meaning any foreign asset needs to be translated into USD. Yes, one can hedge foreign currency exposure, but it is difficult, expensive, and actually reduces the diversification benefits of international exposure.”

“Why JPMorgan Is Turning on an Ex-Star” (DealBook). “At JPMorgan Chase, James “Jes” Staley rose through the ranks, leading its asset management and investment banking businesses and becoming a top lieutenant to the banking giant’s chief, Jamie Dimon. But JPMorgan sued Staley on Wednesday, accusing him of failing to fully inform the bank about what he knew about Jeffrey Epstein, the disgraced financier who died in federal custody in 2019 and was a longtime client. If JPMorgan is found liable for providing banking services to Epstein, it wants its former executive to pay up.”

What we’re reading (3/8)

“Fear of a Recession Spooks the Market” (DealBook). “It seems even the most bullish on Wall Street now get the message: The Federal Reserve is prepared to raise interest rates until it feels it’s sufficiently beaten back inflation — even if those moves cool off the job market and send the economy into recession.”

“The Rally In Stocks Won’t Be Swayed By A Hawkish Powell, As Falling Inflation Still Points To A 20% Gain For The Market This Year, Fundstrat Says” (Insider). “The rally in stocks isn't going to be derailed by a hawkish Federal Reserve, as falling inflation still points to a 20% gain for the market this year, according to Fundstrat's head of research Tom Lee. In a note on Wednesday, Lee reiterated his bullish view on stocks despite Fed Chairman Jerome Powell's hawkish testimony before Congress on Tuesday.”

“Job Openings Declined In January But Still Far Outnumber Available Workers” (CNBC). “The Labor Department’s Job Openings and Labor Turnover Survey, or JOLTS, showed there are 10.824 million openings, down some 410,000 from December, the Labor Department reported. That equates to 1.9 job openings per available worker, or a gap of 5.13 million.”

“U.S. Shale Boom Shows Signs Of Peaking As Big Oil Wells Disappear” (Wall Street Journal). “The boom in oil production that over the last decade made the U.S. the world’s largest producer is waning, suggesting the era of shale growth is nearing its peak. Frackers are hitting fewer big gushers in the Permian Basin, America’s busiest oil patch, the latest sign they have drained their catalog of good wells. Shale companies’ biggest and best wells are producing less oil, according to data reviewed by The Wall Street Journal.”

“Can Policymakers Trust Forecasters?” (Institute for Progress). “Despite all this, the superforecaster phenomenon appears real: the very best forecasters are more skilled than others at predicting, in arbitrary domains, even given little prior knowledge. But where does that leave policymakers looking for insight into the future? If you’re a policymaker, how can you know when to seek expert counsel, invoke statistical models, query the forecasters, or do all of the above? Our problem is matching the right platform to the right policymaker, based on the information they need, and augmenting one method of forecasting with the others.”

What we’re reading (3/7)

“Fed Chair Opens Door To Faster Rate Moves And A Higher Peak” (New York Times). “Jerome H. Powell, the Federal Reserve chair, made clear on Tuesday that the central bank is prepared to react to recent signs of economic strength by raising interest rates higher than previously expected and, if incoming data remain hot, potentially returning to a quicker pace of rate increases.”

“A Bull Market Is In Full Swing – And Most Of Us Are In Denial” (New York Post). “This Pessimism of Disbelief – or PoD for short – starts with each new bull market, lasting about a third of its full duration. At this juncture, PoD has infected most investors.”

“Silicon Valley’s AI Frenzy Isn’t Just Another Crypto Craze” (Vox). “Apps like ChatGPT, created by the Microsoft-backed startup OpenAI, are just the beginning of generative AI’s full range of capabilities, according to its boosters. Many believe it’s a once-in-a-lifetime technological breakthrough that could impact virtually every aspect of society and disrupt industries from medicine to law.”

“Nice People Don’t Value Money? Your Personality May Reveal Your Savings Skills” (Study Finds). “It doesn’t hurt to be a little mean if you’re looking to save more money. A new study says nice people finish last when it comes to managing their finances, since they don’t value it as much. Researchers from Columbia University explain that those who are more agreeable are the least likely to save money, because they prioritize hanging out with people over material wealth. Meanwhile, highly conscientious people may be more motivated to plan for the future and save funds. Moreover, if your personality matches your saving goals you will keep more cash, the research shows.”

“The Supreme Court Should End Home Equity Theft” (Cato Institute). “Geraldine Tyler, age 94, owed Hennepin County $2,300 in unpaid property taxes on her Minnesota condominium. She eventually accrued another $12,700 in fees. Her local government then seized her condo and sold it to pay the taxes and fees. The condo sold for $40,000, and Tyler owed the county only $15,000. But the county didn’t return the excess $25,000 to Tyler. Instead, the county pocketed the excess equity in her home. Tyler sued the county to get the $25,000 back, but she lost in the Court of Appeals for the Eighth Circuit, which held that a Minnesota tax statute “abrogated” Tyler’s property right in her home equity. Effectively, the court held that the county had not taken any of Tyler’s “property” at all, because once the county seized her condo, a statute defined the home equity as no longer her property. Now the Supreme Court has taken Tyler’s case[.]”

What we’re reading (3/6)

“Billionaire Marc Andreessen Warns We’re Headed To A World Where A College Degree Costs $1 Million And A Flatscreen TV Costs $100” (Insider). “The Silicon Valley investor said that sectors provided or controlled by the government have become "technologically stagnant." Innovation in certain highly regulated sectors, like education and healthcare, "is virtually forbidden," causing high prices, he wrote. Andreessen said that over time the price of highly regulated products will continue to climb, while less-regulated products, like flatscreen TVs, will become cheaper.”

“The Dirty Little Secret Of Credit Card Rewards Programs” (New York Times). “In 2016, Chase launched its Sapphire Reserve card. The card comes with perks, bonuses and points multipliers that for big-spending travelers and diners are worth far more than its steep $550 annual fee. There was so much initial demand that Chase ran out of the metal slabs it prints the cards on. Sapphire’s enormous success set off a credit card perks war, with numerous banks flooding the market with sign-on bonuses worth thousands of dollars.”

“Why the Recession Is Always Six Months Away” (Wall Street Journal). “The government’s stimulus measures left household and business finances in unusually strong shape. Shortages of materials and workers mean companies are still struggling to satisfy demand for rate-sensitive goods, such as homes and autos. And Americans are splurging on labor-intensive activities they avoided in recent years, including dining out, travel and live entertainment.”

“Blackstone Defaults On Nordic CMBS As Property Values Wobble” (Bloomberg). “Blackrock Inc. defaulted on a €531 million ($562 million) bond backed by a portfolio of Finnish offices and stores as rising interest rates hit European property values.”

“Arm Opts For New York Stock Listing In Blow To London” (BBC). “The Cambridge-based firm designs the tech behind processors - commonly known as chips - that power devices from smartphones to game consoles. Reports in January said Prime Minister Rishi Sunak had restarted talks with Arm's owner, Japanese investment giant SoftBank, about a possible UK listing. Arm says it decided a sole US listing in 2023 was ‘the best path forward’.”

What we’re reading (3/5)

“Stock Futures Are Little Changed As Investors Look Ahead To Powell Comments, Jobs Data This Week” (CNBC). “U.S. stock futures were little changed on Sunday night as Wall Street looked ahead to a week filled with economic data and the latest commentary from the Federal Reserve.”

“Wonking Out: Peering Through The Fog Of Inflation” (New York Times). “Predicting the future has always been hard, but these days it’s becoming tricky even to predict the past: The statistical agencies keep making large revisions to older data. At the beginning of this year, consumer price data seemed to show a significant decline in inflation over the course of 2022. Then the Bureau of Labor Statistics revised its seasonal adjustment factors, which had no effect on inflation for the year as a whole but made inflation look lower in early 2022 and higher later in the year. The numbers still show improvement, but it’s sufficiently less significant to curb many economists’ initial enthusiasm.”

“What Is A CEO’s Pay Actually Worth?” (Wall Street Journal). “The old approach, still in use, requires companies to show pay for top executives as it was valued when they received it. Stock options and restricted stock are valued as of the day of grant, often a year or more before it is disclosed and several years before it vests, or becomes fully the executive’s property. Companies generally haven’t detailed how award values change during that period.”

“A Do-Nothing Day Makes Life Better” (The Atlantic). “Despite the fact that a day of rest is a core tenet of several ancient religions, as Heller notes, setting it all aside has become so uncommon in American society that we need to actively work to do it.”

“The rise Of The Gen Z Side Hustle” (BBC). “Side hustles existed before the pandemic, but they were often borne from a place of necessity rather than passion. In the past several years, they’ve come in the form of gig-economy jobs, either in lieu of a full-time role, or as a means of supplementing wages. Even now, side hustles are necessary to supplement income for many people: one September 2022 survey of 4,000 UK workers, from insurance company Royal London, shows 16% of respondents had taken on an additional role to help pay for cost of living increases.”

What we’re reading (3/4)

“How The Market Has Changed In The 20+ Years I’ve Covered It” (CNN Business). “If I’ve learned anything in my nearly three decades as a financial journalist (I started my career just out of college in 1995 at the long-defunct Financial World magazine) it’s that ‘this time is different’ is perhaps the biggest myth in investing. There are variations on that theme but, to quote Led Zeppelin, ‘the song remains the same.’”

“Stronger Economic Momentum Will Induce More Rate Hikes In 2023” (Morningstar). “With inflation already easing substantially without a recession, we’re very confident that the U.S. economy is capable of a soft landing, but achieving it is contingent on avoiding monetary policy error. Near-term growth in economic activity is proving more resilient to monetary policy tightening than we had anticipated, which is inducing the Federal Reserve to continue hike rates.”

“A 120-Year-Old Company Is Leaving Tesla In The Dust” (New York Times). “But the more I dealt with Tesla as a reporter — this was before Mr. Musk fired all the P.R. people who worked there — the more skeptical I became. Any time I spoke to anyone at Tesla, there was a sense that they were terrified to say the wrong thing, or anything at all. I wanted to know the horsepower of the Model 3 I was driving, and the result was like one of those oblique Mafia conversations where nothing’s stated explicitly, in case the Feds are listening. I ended up saying, ‘Well, I read that this car has 271 horsepower,’ and the Tesla person replied, ‘I wouldn’t disagree with that.’ This is not how healthy, functional companies answer simple factual questions.”

“Higher Education Is Shockingly Right-Wing” (Steve Waldman). “If "left" and "right" have any meaning at all, "right" describes a worldview under which civilized society depends upon legitimate hierarchy, and a key object of politics is properly defining and protecting that hierarchy…Whatever else colleges and universities do in the United States, they define and police our most consequential social hierarchy, the dividing line between a prosperous if precarious professional class and a larger, often immiserated, working class. The credentials universities provide are no guarantee of escape from paycheck-to-paycheck living, but statistically they are a near prerequisite.”

“One Way U.S. Students Can Save Money On College Tuition: Head To Europe” (Wall Street Journal). “College tuition in the European Union tends to be far less than in the U.S., not only for locals but for students who come from outside the EU as well. Indeed, both undergrad and graduate-school degrees in Europe often can be earned at a fraction of what it costs in the U.S.”

What we’re reading (3/3)

“A ‘Perfect Storm’ Of Recession, Debt, And Out-Of-Control Inflation Is Coming For Markets This Year, ‘Dr. Doom’ Nouriel Roubini Says” (Insider). “A ‘perfect storm’ is brewing, and markets this year are going to get hit with a recession, a debt crisis, and out-of-control inflation, the economist Nouriel ‘Dr. Doom’ Roubini said. Roubini, one of the first economists to call the 2008 recession, has been warning for months of a stagflationary debt crisis, which would combine the worst aspects of ‘70s-style stagflation and the '08 debt crisis.”

“Fed’s Credibility Can’t Take A Soft Landing” (Manhattan Institute). “Someone is in denial over inflation — either investors or Federal Reserve policymakers. But no matter how things play out, the disconnect suggests the Fed has lost its credibility. Or perhaps it never had it to begin with. And if that’s the case, soft landing or hard, one casualty of this economy could be the Fed’s inflation-targeting regime.”

“Oil Companies Hit With Backlash After Bringing In $200 Billion In Profits Last Year” (CNBC). “Oil companies pulled in record profits in 2022, as oil prices skyrocketed. Revenues for the biggest integrated European and American oil companies nearly doubled during 2021. Profits soared. But that has also spurred backlash from consumer advocates and political leaders. ‘Oil companies’ record profits today are not because they’re doing something new or innovative,’ President Joe Biden said Oct. 31. ‘Their profits are a windfall of war — the windfall from the brutal conflict that’s ravaging Ukraine and hurting tens of millions of people around the globe.’”

“Crypto Companies Behind Tether Used Falsified Documents and Shell Companies to Get Bank Accounts” (Wall Street Journal). “In late 2018, the companies behind the most widely traded cryptocurrency were struggling to maintain their access to the global banking system. Some of their backers turned to shadowy intermediaries, falsified documents and shell companies to get back in, documents show.”

“Office Mandates. Pickleball. Beer. What Will Make Hybrid Work Stick?” (New York Times). “Business leaders are in a phase of trial and error that comes with staggering stakes. They are figuring out how many days to call employees back to the office, and on top of that how strictly to enforce their own rules. While some companies are in five days a week and others have gone remote forever, many more employers have landed on a hybrid solution, and as they announce these plans they are facing fierce resistance.”

What we’re reading (3/2)

“Fed Official Says Hotter Data Will Warrant Higher Rates” (Wall Street Journal). “The Federal Reserve will need to raise rates to higher levels than previously anticipated to prevent inflation from picking up if the recent strength in hiring and consumer spending continues, a central bank official said Thursday.”

“Costco Q2 Earnings: Stock Slips After Mixed Results” (Yahoo! Finance). “Costco (COST) posted fiscal second-quarter earnings results Thursday, March 2, after market close that mostly beat expectations. Shares were down more than 2% after the release.”

“Active Funds Continue To Fall Short Of Their Passive Peers” (Morningstar). “Brutal market performance in 2022 reignited the narrative that active funds can better navigate market turmoil than passive peers. Despite an uptick in success rates by U.S. stock-pickers, the latest evidence debunks these claims yet again. As Warren Buffett once said, ‘only when the tide goes out do you discover who’s been swimming naked.’ In 2022, it turned out that active bond and real estate funds were caught skinny-dipping.”

“Drilling For Oil On The NYSE” (Smead Capital Management). “As a young stockbroker in the 1980s, I was very enamored with T. Boone Pickens. Pickens recognized the huge value that built up in common stocks in the inflationary 1970s and began to use the financial backing of the Junk Bond King, Michael Milken, to become an activist on Wall Street. His little company, Mesa Petroleum, started investing in undervalued large cap oil stocks and threatened to do large leveraged buyouts (LBOs) with the assistance of Milken’s firm, Drexel Burnham Lambert (my employer). Pickens said, ‘It is cheaper to drill for oil on the New York Stock Exchange than it is to drill directly.’ After reading Pioneer Natural Resources CEO Scott Sheffield’s comments recently, we at Smead Capital Management believe we’ve reached that point again[.]”

“Once The World’s Largest, A Hotel Goes ‘Poof!’ Before Our Eyes” (New York Times). “This isn’t — or wasn’t — just any building. This was once the largest hotel on earth, with 2,200 rooms, shops, restaurants, its own newspaper, and a telephone number immortalized by the bandleader Glenn Miller with a 1940 song ‘Pennsylvania 6-5000[.]’”

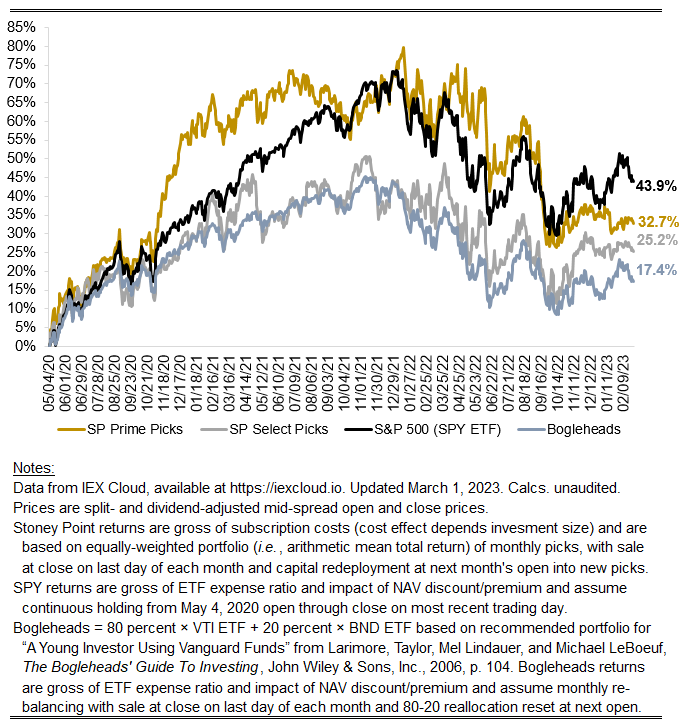

February (and belated January) performance update

Hi friends, here is February’s update. I neglected to provide a January update earlier this — I was swamped with my actual job. But I am caught up now, so I am including that update and the relevant numbers here.

The numbers for February are below (with January’s returns in parentheses).

Prime: +0.18% (-1.71%)

Select: -1.84% (+2.15%)

SPY ETF benchmark: -2.21% (+5.75%)

Bogleheads benchmark (80% VTI + 20% BND): -2.29% (+5.50%)

Prime was flattish in February, a little more than 200 bps higher than the market, though in the January-February combined period the market properly trounced the strategy. Select was roughly in line with the market in February and lower in January, so on the whole it is fair to assess my picks as comparably bad in 2023 so far.

Peeling the onion back one layer, what looks anomalous to me is the market’s extraordinary performance in January. I have noted before that the average return on the market overall is a high-single-digit percentage number. For example, Kroll reports that the historical mean equity risk premium (return on stocks above a long-term government bond yield) was 5.26 percent for the 1798 to 2022 period. Adding yesterday’s 10-year U.S. Treasury yield of 3.92 percent implies a reasonable “expected” market return of 9.18 percent per year. Against that backdrop, the market’s 5.75 percent return in January was abnormal. Were it not, it would imply an expected annualized return of ~96% (= (1+5.75 percent)^12 months-1), or a doubling in corporate value in a one year period. Needless to say, that is implausible. In contrast, an equal-weighted portfolio of Prime and Select picks would have produced a 0.22 percent return in January, or about 3 percent when annualized. That is lower than the market’s base rate, but certainly within the range of reasonable estimates of what the market’s true normal return is.

Looking at the picks, specifically, what jumps out is that our model is leaning into the sorts of names typically recommended by investment professionals in periods of heightened economic uncertainty. In January, for example, that included Hershey, McDonald’s, Mondelez, Conagra, Coca-Cola, Pepsi, etc. The model has consistently flagged companies like this as desirable since the fall, and continues to do so. Intuitively, that doesn’t “feel” wrong for the environment we are in, where concerns abound about the prospect of higher-yet rates, slowing demand across the economy, rising delinquencies across consumer loan books, weak corporate earnings guidance, etc. These concerns have accelerated recently, compared to January when the prospect of a “soft-landing” emerged as a widespread, if not consensus, prediction among market pundits. That view likely benefited the large, high-duration technology stocks that dominate the weighting in the S&P 500 index, but what matters now is whether that is the lay of the land today. One needn’t work too hard to find reliable evidence that it is not the state of affairs today, since nearly all of said technology companies have initiated deep reductions in force and seem generally quite pessimistic on analyst calls these days. February seems like a bit of vindication when it comes to all of this — with Select a bit better than the market and Prime significantly better than the market — but we’ll see how the coming months play out.

Stoney Point Total Performance History

March picks available now

The new Prime and Select picks for March are available starting now, based on a model run put through today (February 28). As a note, we’ll be measuring the performance on these picks from the first trading day of the month, Wednesday, March 1, 2023 (at the mid-spread open price) through the last trading day of the month, Friday, March 31, 2023 (at the mid-spread closing price).

What we’re reading (2/27)

“Markets History 101: It’s Time to Buy Bonds” (Wall Street Journal). “In both the 1973 and 1980 falls—and in every recession and major downturn since—bonds far outperformed stocks. This time, stocks and bonds have fallen together, with the MSCI USA down 16.7% from its high in January last year, and benchmark 10-year Treasurys down 16% since then, both with income reinvested.”

“Warren Buffett Calls Stock Buyback Critics ‘Economic Illiterate’ In Berkshire Hathaway Annual Letter” (CNBC). “‘When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive),’ the 92-year-old investor said in the much-anticipated letter released Saturday.”

“The Price You Pay: A Look At Equity Valuations” (Charles Schwab). “A hallmark of this current reporting season is analysts' aggressive cuts to estimates for growth. Nearly a year ago, the consensus expectation for fourth-quarter growth was +10.4%; that has since been cut to -2.8% as analysts have come to terms with stickier input costs and a decline (albeit uneven across sectors) in revenue growth.”

“Inside The New York Times Blowup Over Transgender Issues” (Vanity Fair). “The Times’ journalistic mission, as framed by the masthead that day, may have seemed cut-and-dried. And yet a week later, the newsroom would be embroiled in debates over objectivity and ‘activism,’ as criticism of the paper’s coverage of transgender issues sparked a series of exchanges involving Times leaders, staffers, contributors, and the paper’s union. The current dispute, ostensibly about transgender coverage, has reignited past concerns about how the Times covers marginalized groups, as well as whether younger, so-called ‘woke’ staff are helping shift the paper’s journalistic values.”

“I Do ‘Bare Minimum Mondays’ At Work To Help Beat The ‘Sunday Scaries' And Avoid Burnout. It’s Completely Changed My Life And How I Approach My Job.” (Insider). “One day last March, I gave myself permission to do the absolute bare minimum for work, and it was like some magic spell came over me. I felt better. I wasn't overwhelmed, and I actually got more done than I expected.”

What we’re reading (2/26)

“Lab Leak Most Likely Origin Of Covid-19 Pandemic, Energy Department Now Says” (Wall Street Journal). “The U.S. Energy Department has concluded that the Covid pandemic most likely arose from a laboratory leak, according to a classified intelligence report recently provided to the White House and key members of Congress. The shift by the Energy Department, which previously was undecided on how the virus emerged, is noted in an update to a 2021 document by Director of National Intelligence Avril Haines’s office.”

“Salesforce Stock Gets Activist Interest Ahead Of Earnings; Software Titans Snowflake, Workday, Splunk Set To Report” (Investor’s Business Daily). “Salesforce (CRM) and Splunk (SPLK) headline a busy week of earnings reports in the software sector. Salesforce stock has started to drift lower after powering above its 40-week moving average in late January.”

“The Furniture Hustlers of Silicon Valley” (New York Times). “Ms. Susewitz, who started Reseat in 2020, is one of an increasing number of behind-the-scenes specialists in the Bay Area who are carving out a piece of the great office furniture reshuffling. There are professional liquidators, Craigslist flippers and start-ups spouting buzzwords like ‘circular economy.’ And a few guys with warehouses full of really nice chairs. All of them are capitalizing on a wave of tech companies that are drastically shrinking their physical footprints in the wake of the pandemic-induced shift to remote work and the recent economic slowdown.”

“Covid Shrank The Restaurant Industry. That’s Not Changing Anytime Soon” (CNN Business). “In 2020, Covid restrictions ground the nation’s bustling restaurant industry to a halt. Since then, there have been significant signs of a rebound: Dining rooms have reopened and customers have returned to cafes, fine-dining establishments and fast food joints. But there are fewer US restaurants today than in 2019. It’s not clear when —if ever — they’re coming back.”

“Investors Are Bracing For Surge In Market Volatility” (Wall Street Journal). “After lying relatively dormant for months, the VIX, also known as Wall Street’s fear gauge, rose above 23 last week, its highest level since the first few trading days of the year. Readings below 20 typically signify complacency, while those above 30 signal investors are scurrying for protection.”

What we’re reading (2/25)

“‘I Feel Like I Got Catfished’: Young VCs Who Left Investment Banking And Consulting Jobs Are Having Career Second Thoughts In The Downturn” (Insider). “Young VCs who were formerly investment bankers or consultants told Insider that faltering deal flow and cost-cutting within firms have led to increased competition and stress among their peers. A number of these sources spoke under the condition of anonymity because they were not authorized to discuss these internal matters publicly.”

“Americans In Their 30s Are Piling On Debt” (Wall Street Journal). “American millennials in their 30s have racked up debt at a historic clip since the pandemic. Their total balances hit more than $3.8 trillion in the fourth quarter, according to the Federal Reserve Bank of New York, a 27% jump from late 2019. That is the steepest increase of any age group. It is also their fastest pace of debt accumulation over a three-year period since the 2008 financial crisis.”

“The Pay Gap Between Hospital CEOs And Nurses Is Expanding Even Faster Than We Thought” (Vox). “The pay disparity between hospitals’ administrative staff and clinical staff is exploding: Some of the individual hospital CEOs covered in the study saw their salaries increase by more than 700 percent in just a few years, while doctors and nurses got a fraction of that salary increase, 15 to 20 percent, across an entire decade.”

“The E.S.G. Fight Has Come To This: Bankers Suing Lawyers” (New York Times). “So what is E.S.G., anyway? As investors rename their firms and their funds in a race to ride the E.S.G. wave, cynics see the debate over the term’s definition as degenerating into everyone seeing gibberish. Because funds can define E.S.G. nearly any way they want, they have come to resemble an extra-strange goulash. Sometimes, these new or newly rebranded operations are just elegantly simple greenwashing and nothing more.”

“Peacetime Would Be A Black Swan Event For Energy” (New York Times). “It is too early to talk about an end to the war, even with a new Chinese peace proposal on the table. All the signs point to Russia and Ukraine digging in for a long battle. But energy companies that are considering pouring billions of dollars into projects with 10- or 15-year time horizons have to consider what might happen to Russian fossil fuels in peacetime.”

March picks available soon

We’ll be publishing our Prime and Select picks for the month of March before Wednesday, March 1 (the first trading day of the month). As always, we’ll be measuring SPC’s performance for the month of February, as well as SPC’s cumulative performance, assuming the sale of the February picks at the closing price (at the mid-point of the closing bid and ask prices) on the last trading day of the month (Tuesday, February 28). Performance tracking for the month of March will assume the March picks are bought at the open price (at the mid-point of the opening bid and ask prices) on the first trading day of the month (Wednesday, March 1).

What we’re reading (2/23)

“Meet The $10,000 Nvidia Chip Powering The Race For A.I.” (CNBC). “Companies like Microsoft and Google are fighting to integrate cutting-edge AI into their search engines, as billion-dollar competitors such as OpenAI and Stable Diffusion race ahead and release their software to the public. Powering many of these applications is a roughly $10,000 chip that’s become one of the most critical tools in the artificial intelligence industry: The Nvidia A100.”

“Wall Street Backs New Class Of Psychedelic Drugs” (Wall Street Journal). “Wall Street is betting tens of millions of dollars on psychedelic drugs that backers say could treat mental illness for a fraction of what it costs to do therapy with better-known treatments. Transcend Therapeutics Inc. raised $40 million from venture-capital investors in January to develop a post-traumatic stress disorder treatment that its 29-year-old CEO Blake Mandell says would require about half the amount of therapy as MDMA, or ecstasy, a popular hallucinogen. Gilgamesh Pharmaceuticals Inc. and Lusaris Therapeutics Inc. have announced capital raises of about $100 million since November for similar products addressing depression.”

“Google Changed Work Culture. Its Former Hype Woman Has Regrets.” (New York Times). “Claire Stapleton joined Google in 2007, during the height of the techno-optimism boom, and fell in love with the company. Over the next 12 years, she created corporate messaging and managed the company’s image, internally and externally. But during this time, she also witnessed it fall painfully short of its utopian promises, and as the world soured on Big Tech, she did, too. Stapleton left Google in 2019.”

“Sam Bankman-Fried’s Bond Guarantors Reveal The Surprisingly Lucrative World Of Legal Academia” (Dealbreaker). “The case of Sam Bankman-Fried has been a fascinating one for the legal industry. Sure, the collapse of FTX is a potential harbinger of doom for the crypto market (and a potential boon for the Biglaw litigators that count crypto clients in their book of business). But the way SBF has continually spoken to the media — despite the advice of counsel — has been riveting. Add in that SBF is the child of two legal academics — Barbara Fried and Joseph Bankman, both of Stanford Law School — and you can see there’s plenty to hold the industry’s attention. Now that Southern District of New York judge Lewis Kaplan has unsealed the names of the two anonymous sureties who supplemented the $250 million personal recognizance bond (co-signed by SBF’s parents), it’s even more intriguing.”

“The SEC Is Starting A Massive Database Of Every Stock Trade” (CATO Institute). “The Consolidated Audit Trail is intended to collect and accurately identify every order, cancellation, modification, and trade execution for all exchange‐listed equities and options across all U.S. markets, allowing the Securities and Exchange Commission (SEC) to track orders and identify who made them. The SEC ordered the CAT to be created in 2012 after regulators had difficulty identifying the causes of the 2010 ‘flash crash.’ At the time, then‐SEC Chair Mary Schapiro described the CAT as providing regulators with the ‘data and means to exponentially enhance [their] abilities to oversee a highly complex market structure.’ And in years since, the CAT has been championed as necessary for the SEC’s enforcement efforts.”

What we’re reading (2/22)

“The Maze Is In The Mouse” (Praveen Seshadri). “Google has 175,000+ capable and well-compensated employees who get very little done quarter over quarter, year over year. Like mice, they are trapped in a maze of approvals, launch processes, legal reviews, performance reviews, exec reviews, documents, meetings, bug reports, triage, OKRs, H1 plans followed by H2 plans, all-hands summits, and inevitable reorgs. The mice are regularly fed their “cheese” (promotions, bonuses, fancy food, fancier perks) and despite many wanting to experience personal satisfaction and impact from their work, the system trains them to quell these inappropriate desires and learn what it actually means to be ‘Googley’ — just don’t rock the boat. As Deepak Malhotra put it in his excellent business fable, at some point the problem is no longer that the mouse is in a maze. The problem is that ‘the maze is in the mouse’.”

“BlackRock US ESG Flows Fall On Tech Rout, Anti-Green Backlash” (Bloomberg). “Cash flows into US sustainable funds plummeted last year as the broader market took a beating and anti-ESG crusaders targeted money managers including BlackRock Inc. for ‘woke capitalism.’”

“Rising Bond Yields Rattle 2023 Stock Rally” (Wall Street Journal). “Last year’s markets boogeyman is back. U.S. government debt has reversed its early-year rally, sending Treasury yields higher than where they finished 2022. That is threatening to end a brief reprieve for stocks and riskier types of bonds, which both languished last year as yields climbed rapidly.”

“Millions Of Millennials Could Soon Enter A Midlife Crisis. But They're Going To Spend And Divorce Less — And Value Experiences More — Than Prior Generations.” (Insider). “Millions of millennials — whose ages range between 27 and 42 — will turn 40 this year, with many more following them in the years to come. And while there's nothing inherently treacherous about this milestone, there's reason to believe many of them could experience some form of a midlife crisis as they reach middle-age.”

“Cyberattack On Food Giant Dole Temporarily Shuts Down North America Production, Company Memo Says” (CNN Business). “A cyberattack earlier this month forced produce giant Dole to temporarily shut down production plants in North America and halt food shipments to grocery stores, according to a company memo about the incident obtained by CNN.”

What we’re reading (2/21)

“Office Landlord Defaults Are Escalating As Lenders Brace For More Distress” (Wall Street Journal). “The number of big office landlords defaulting on their loans is on the rise, fresh evidence that more developers believe that remote and hybrid work habits have permanently impaired the office market.”

“How ChatGPT Breathed New Life Into The Internet Search Wars” (The Week). “Amid the growing frenzy around ChatGPT, other tech companies have begun announcing their rival chatbots. Executives at Google declared a ‘code red’ in response to OpenAI's software, fast-tracking the development of many AI products to close the widening gap between itself and its emerging competitors. Shortly after, the company unveiled and began offering select users a look at its own chatbot, Bard, which — similar to ChatGPT — uses information from the internet to generate textual responses to users' queries.”

“What’s Really So Wrong About Secretly Working Two Full-Time Jobs At Once?” (Slate). “Managers have an instinctive horror at the thought of someone secretly working a second job during their work hours for the first, but if they can’t point to any problems resulting from it … why? Maybe it’s time to rethink that.”

“Hedge Fund Billionaire Extracts Billions More To Retire” (New York Times). “[N]either Mr. Dalio, known for his creed of “radical transparency,” nor Bridgewater said at the time, or since, that he had hardly gone without a fight. His exit — partly spurred by controversial remarks he had made on television about China’s human rights record — followed more than six months of frantic behind-the-scenes wrangling over how much money his successors at the firm were willing to pay the billionaire to go away. In the end, Mr. Dalio, with an estimated net worth of $19 billion, agreed to surrender his control over all key decisions at Bridgewater only if the firm agreed to give him what could amount to billions of dollars in regular payouts over the coming years through a special class of stock.”

“Walmart Warns It’s In For A Tough Year” (CNN Business). “Walmart forecast slower sales and profit growth, disappointing investors and sending its stock down during morning trading Tuesday. However, Walmart notched an 8.3% sales increase during its latest quarter at US stores open for at least one year, the company said Tuesday, with more customers buying its private label brands and more higher-income households shopping at its stores.”