What we’re reading (10/23)

“Notes On A Statistical Scandal” (Financial Times). “Even a spreadsheet can become a victim of its own success. Just ask the World Bank’s Doing Business report. While many worthy publications from the World Bank are never downloaded, Doing Business has been a smash hit for years. No longer. Amid an ugly scandal about data manipulation that has left the head of the IMF, Kristalina Georgieva, fighting for her career, Doing Business has been cancelled.”

“WeWork Hits The Stock Markets” (WeWork). “After two years, a failed I.P.O., a plunging valuation and a pandemic that reset many workers’ relationships with the office, the co-working company WeWork [began] a new life [yesterday] as a publicly traded company. WeWork argues it’s a better company now. It has renegotiated or exited some 500 leases this year, saving over $400 million, according to its C.E.O., Sandeep Mathrani. And its deal to go public via a merger with a SPAC, BowX, will provide $1.3 billion in new capital.”

“Housing Is The Economy’s Energizer Bunny: It Keeps Going And Going” (CNN Business). “Even as some sectors of the economy remain muted, the housing boom keeps going and going. That's obviously good for builders, but it could also be great news for the broader economy and stock market — especially since this strength appears to be nationwide. ‘Residential is still pretty hot. Remodeling activity is good. Housing starts are good,’ said Mark Sheahan, CEO of Graco, which makes paint sprayers for home owners and contractors, on an earnings call Thursday. ‘I don't see any real negatives in the future. No storm clouds on the horizon, I would say, from our viewpoint,’ Sheahan added.”

“The Coming Electric Car Disruption That Nobody’s Talking About” (Bloomberg). “Making the massive batteries that line the bottom of electric cars promises to employ thousands. But where a conventional car’s engine and transmission have hundreds of parts, some electric-vehicle powertrains have as few as 17, according to the Congressional Research Service. That doesn’t take into account the radiators, fuel tanks or exhaust systems that electric vehicles don’t need. Once operating, an electric car has no spark plugs or oil that need changing or mufflers that wear out. And with so few moving parts, service stations could be relegated to changing tires and windshield wipers.”

“Powell Says Supply-Side Constraints Have Worsened, Creating More Inflation Risk” (Wall Street Journal). “Federal Reserve Chairman Jerome Powell indicated he is now somewhat more concerned about higher inflation and said that the central bank would watch carefully for signs that households and businesses were expecting sustained price pressures to continue. ‘Supply-side constraints have gotten worse,’ Mr. Powell said Friday at a virtual conference. ‘The risks are clearly now to longer and more-persistent bottlenecks, and thus to higher inflation.’”

What we’re reading (10/22)

“Just How High Could The Dow Go?” (New York Times). “It can be simultaneously true that capital has enjoyed an enviable position and that markets going up is not a sign of a rigged system. There are now about 4,000 publicly traded companies on the major exchanges in the United States — 20 years ago, there were around 7,000. Capital markets reward those that excel in eking out double-digit growth in a single-digit world. Only the strongest companies survive.”

“It’s Time For Americans To Buy Less Stuff” (Vox). “When the stuff we want is so hard to get ahold of, why go to such great lengths to buy it? Consumers have the option to not order items manufactured overseas, to source things locally from small businesses or artisans. We also have a choice that eliminates the potential for shipping or supply chain mishaps: We can just buy less.”

“Chipotle Earnings Crush Estimates As Sales Jump 22%, Higher Menu Prices Offset Rising Costs” (CNBC). “Chipotle Mexican Grill on Thursday reported quarterly earnings that crushed Wall Street’s estimates as its menu price increases helped the chain weather higher costs. Shares of the company rose more than 1% in extended trading…Chipotle is still experiencing some staffing challenges amid the labor crunch that’s hitting the broader industry. But Chief Technology Officer Curt Garner said in an interview that Chipotle was able to keep that from hitting its sales for the most part by keeping its restaurants open.”

“Deutsche Bank Whistleblower Gets $200 Million Bounty For Tip On Libor Misconduct” (Wall Street Journal). “A whistleblower whose information helped U.S. and U.K. regulators investigate manipulation of global interest-rate benchmarks by Deutsche Bank AG was awarded nearly $200 million for assisting the probe, according to people familiar with the matter. The payout is the largest ever by the Commodity Futures Trading Commission, which along with the Justice Department and U.K. Financial Conduct Authority settled enforcement actions against Deutsche Bank in 2015.”

“A Real-Time Revolution Will Up-End The Practice Of Macroeconomics” (The Economist). “[T]he age of bewilderment is starting to give way to greater enlightenment. The world is on the brink of a real-time revolution in economics, as the quality and timeliness of information are transformed. Big firms from Amazon to Netflix already use instant data to monitor grocery deliveries and how many people are glued to “Squid Game”. The pandemic has led governments and central banks to experiment, from monitoring restaurant bookings to tracking card payments. The results are still rudimentary, but as digital devices, sensors and fast payments become ubiquitous, the ability to observe the economy accurately and speedily will improve. That holds open the promise of better public-sector decision-making—as well as the temptation for governments to meddle.”

What we’re reading (10/21)

“Lessons From Oil On The New Crypto Futures Fund” (Fisher Investments). “Every investment decision is a tradeoff. When you buy stocks, you accept the risk of short-term volatility in exchange for the likelihood of high long-term returns. With a bitcoin futures ETF, we surmise you are accepting the risk of tracking error in exchange for the transparency and investor protections that come with owning a regulated fund. Some investors might think the tradeoff is worthwhile. Some might not. Some might want to avoid bitcoin entirely, concluding that speculating conflicts with their long-term goals.”

“The Great Resignation Is Accelerating” (The Atlantic). “Before the pandemic, the office served for many as the last physical community left, especially as church attendance and association membership declined. But now even our office relationships are being dispersed. The Great Resignation is speeding up, and it’s created a centrifugal moment in American economic history.”

“The Revenge Of The Essential Worker” (The New Republic). “Of all the images coming out of the current strike wave…the apparent chaos at the John Deere plants is among the most viscerally satisfying. Last week, more than 10,000 workers across 14 plants went on strike after rejecting the tractor maker’s contract offer, an offer that included a 4 percent increase in pay the year after its CEO made $15.6 million himself. To keep its business running, the company told The Washington Post, it ‘activated a continuity plan,’ which sounded reasonable until it became clear that the plan took salaried office workers, gave them punchy new titles like ‘tractor driver’ and ‘general repair,’ and put them on the shop floor.”

“PayPal Is In Late-Stage Talks To Acquire Pinterest” (CNBC). “PayPal has discussed acquiring the company for a potential price of around $70 a share, which would value Pinterest at about $39 billion, according to Bloomberg. Pinterest stock closed at $55.58 per share on Tuesday. PayPal and Pinterest declined to comment.”

“The S.E.C. Weighs In On Meme-Stock Mania” (DealBook). “ [A] long-awaited S.E.C. report about those events, released yesterday, concluded that the markets operated largely as intended, debunking conspiracy theories. The report proposed no policy changes…[t]he 45-page report was simply meant to describe events, a senior S.E.C. official told reporters. But many observers anticipated much more, considering that the S.E.C. chairman, Gary Gensler, has hinted at big changes to the way markets work.”

What we’re reading (10/20)

“The Wealthiest 10% Of Americans Own A Record 89% Of All U.S. Stocks” (CNBC). “The top 1% gained more than $6.5 trillion in corporate equities and mutual fund wealth during the Covid-19 pandemic, while the bottom 90% added $1.2 trillion, according to the latest data from the Federal Reserve. The share of corporate equities and mutual funds owned by the top 10% reached the record high in the second quarter, while the bottom 90% of Americans held about 11% of individually held stocks, down from 12% before the pandemic.”

“Credit Suisse To Pay $475 Million, Admits Defrauding Investors To Settle Mozambique Charges” (Wall Street Journal). “A subsidiary of the Swiss bank pleaded guilty to wire fraud conspiracy charges in New York federal court Tuesday. Credit Suisse, which previously had maintained it was a victim of rogue employees, admitted to defrauding investors who bought some of the debt and agreed to pay $275 million to resolve both a criminal probe by the Justice Department and a civil investigation by the Securities and Exchange Commission.”

“The $5 Trillion Insurance Industry Faces A Reckoning. Blame Climate Change.” (Vox). “The water has receded and the embers have died down from many of the disasters in the United States this year — leaving insurance companies that cover floods, fires, hail, and extreme cold on the hook for staggering losses. If current trends continue, they could suffer one of the costliest years in recent memory.”

“For Uber And Lyft, The Rideshare Bubble Bursts” (New York Times). “Underwritten by venture capital, Uber and Lyft hooked users by offering artificially cheap rides that often undercut traditional yellow cabs. But labor shortages and a desperate need to find some path to a profitable future have caused rideshare prices to skyrocket, perhaps to a more rational level. After burning through billions of venture capital dollars, Uber said it was on a path to profitability last year, using an accounting metric that ignores many of the costs that actually make it unprofitable. By the same measure, chief executive Dara Khosrowshahi is projecting this quarter could be profitable. That remains to be seen.”

“Long-Term NAEP Scores For 13-Year-Olds Drop For First Time Since Testing Began In 1970s — ‘A Matter for National Concern,’ Experts Say” (The 74). “Thirteen-year-olds saw unprecedented declines in both reading and math between 2012 and 2020, according to scores released this morning from the National Assessment of Educational Progress (NAEP). Consistent with several years of previous data, the results point to a clear and widening cleavage between America’s highest- and lowest-performing students and raise urgent questions about how to reverse prolonged academic stagnation.”

What we’re reading (10/19)

“Why The ‘Big Short’ Guys Think Bitcoin Is A Bubble” (The Intelligencer). “Hedge-fund mogul John Paulson, who was behind the ‘the greatest trade ever’ — in 2007, he personally made $4 billion on his short of subprime mortgages — thinks cryptocurrencies are a bubble that will prove to be ‘worthless.’ Michael Burry, the quirky hedge-fund manager made famous in The Big Short movie (played by Christian Bale), complains that no one is paying attention to crypto’s leverage. For months, he has been suggesting that bitcoin is on the precipice of collapse. And NYU professor Nassim Taleb, whose now-canonical book The Black Swan warned about the dangers of unpredictable events just ahead of the subprime crash, argues that bitcoin is functionally a Ponzi scheme.”

“A Triple Shock Slows China’s Growth” (The Economist). “When supply is tight, prices are supposed to rise, obliging customers to economise on their consumption. But as the price of coal shot up, power stations were unable to pass their higher costs on. The price they could charge the grid company that buys the bulk of their power could only fluctuate up to 10% above a regulated price, which was changed infrequently. And the tariff paid by end-users was based on a provincial catalogue of prices that was similarly inflexible. Some power stations simply stopped operating, refusing to generate power at a loss.”

“Apple Cements Break From Intel With Laptops Powered By Own Computer Chips” (Financial Times). “Apple cemented its move away from Intel on Monday, unveiling two new high-end laptop computers powered by its own ‘Apple Silicon’ chips. The new 14-inch and 16-inch MacBook Pro notebooks, which start at $1,999 and $2,499 each, respectively, both feature the ‘M1 Pro’ chip, an iteration on the first Apple-designed M1 processors introduced a year ago.”

“Rent The Runway Targets Valuation Of Up to $1.5 Billion In IPO” (Wall Street Journal). “Rent the Runway Inc. is seeking a valuation of as much as $1.5 billion in its initial public offering next week, in what would cap a comeback for the clothing-rental business. The New York company is aiming to sell shares at between $18 and $21 apiece for a fully diluted valuation of $1.24 billion to $1.46 billion, it said in a securities filing Monday. The roadshow for company management and their underwriters to pitch the shares to potential investors begins Tuesday and the shares are to start trading on the Nasdaq Stock Market next Wednesday.”

“Colin Powell’s Greatest Legacy Is In The People He Inspired” (Condoleeze Rice, Washington Post). “In 2003, sitting in Buckingham Palace during President George W. Bush’s state visit to Britain, Alma, Colin and I drank a toast to our ancestors. ‘They would never have believed it,’ I said. ‘No, but they are smiling now,’ he said. Colin believed that his life and all that he achieved were an affirmation of America’s possibilities. He didn’t take his success for granted and recounted stories of people he knew who never got out of his modest South Bronx neighborhood. He knew that he was talented — but he was humble enough to believe that he was also lucky.”

What we’re reading (10/18)

“Inflation: Persistently Transitory” (Charles Schwab). “If the global economy persistently goes from one transitory source of inflation to the next, it may keep inflation elevated for longer than markets currently anticipate. Following this year’s supply disruptions and recent climb in energy prices, markets may begin to price another potential source of inflation: workers demanding higher wages as strikes blanket the news. Yet, central banks’ attitude toward inflation has changed. This may mean that the lift to earnings from inflation could more than offset any compression on stock valuations from tighter financial conditions.”

“The Revolt Of The American Worker” (Paul Krugman, New York Times). “[s]omething…fundamental and lasting may be happening in the labor market. Long-suffering American workers, who have been underpaid and overworked for years, may have hit their breaking point…[w]hat seems to be happening instead is that the pandemic led many U.S. workers to rethink their lives and ask whether it was worth staying in the lousy jobs too many of them had.”

“A Secretive Hedge Fund Is Gutting Newsrooms” (The Atlantic). “In May, the [Chicago] Tribune was acquired by Alden Global Capital, a secretive hedge fund that has quickly, and with remarkable ease, become one of the largest newspaper operators in the country. The new owners did not fly to Chicago to address the staff, nor did they bother with paeans to the vital civic role of journalism. Instead, they gutted the place.”

“Rising Mortgage Rates Shift Lenders’ Focus To Home Buyers” (Wall Street Journal). “Lenders still packaged up hundreds of billions of dollars of refinance loans last quarter. But business is harder to come by these days, Mr. Menatian said. Instead of taking inbound calls, he has been phoning clients whose home values have risen enough that they can refinance out of their mortgage insurance policies.”

“China Tests New Space Capability With Hypersonic Missile” (Financial Times). “China tested a nuclear-capable hypersonic missile in August that circled the globe before speeding towards its target, demonstrating an advanced space capability that caught US intelligence by surprise. Five people familiar with the test said the Chinese military launched a rocket that carried a hypersonic glide vehicle which flew through low-orbit space before cruising down towards its target.”

A private equity puzzle

Private equity occupies a special place in the universe of investment alternatives. A nascent asset class only decades ago—at which point public equities had existed in their modern form since at least 1602*—the industry has grown substantially in size over time. Simple anecdotes illustrate the incredible stature the industry has achieved since its early days:

Today, pension funds around the world scramble to ‘get an allocation’ to the most highly regarded funds;

Scions of the industry regularly wax philosophical to a very friendly business press about ‘what it takes’ to be a great entrepreneur (and are listened to), or even have their own programs discussing their views on the world with notables like Secretaries of State and are held out as “peers” of said notable people;

Other former scions have run for high office, with at least one running for the highest office, with his experience in private equity occupying a central place in the narrative around his competence as a leader, and the central focal point of attack for his opposition;

Like clockwork, many of the best and brightest young minds at the world’s best collegiate institutions are motivated by (among other more innocuous things, like learning, etc., it should be said) the chance to eventually land in private equity in making a Faustian Bargain in which they will first spend 1-2 years enduring a job that in certain instances has been so unnecessarily stressful (M&A investment banking) that a non-negligible number of those in its employ die either from acts of self-harm or exhaustion;

There are now eager start-up private equity funds aiming to bring private equity investment opportunities to retail investors. Here is one such exemplar fund that, ironically, is funded by private equity.

But is this stature deserved? And, if it ever was, is it still today?

At the outset, it’s worth noting that many credible people have long said “no” to that question. Take Nobel Laureate Joseph Stiglitz, for example. His main qualm about the industry, reportedly, is that it is full of rent-seeking, e.g., the extraction of wealth from the economy to the benefit of the funds without an equal creation of incremental economic value. The steady stream of stockholder litigation involving private equity funds as defendants would seem—at a minimum—consistent with that assertion, even if you think many of these suits are frivolous efforts at rent-seeking in and of themselves.

Another relevant economic question is whether the industry’s returns are even that good.

A review of the returns of at least one of the most well-respected and prestigious private equity firms over the past several decades suggests the glory days might be over. In the case of that firm (who shall go nameless here), annual equity returns over the last 40+ years were about 50 percent, but only about 30 percent over the last decade+ or so, implying a near halving of annualized returns from its first three decades (when returns must have averaged a little over 57 percent) to the most recent decade for which I have data (which actually ended a few years ago). If you do a simple monthly trendline through these numbers using the exact dates in the data, it would suggest annual returns for the period ending this month are probably about 18 percent. Now, 18 percent per year sounds pretty good, but keep in mind that typical private equity investments are super leveraged, and leverage creates mechanical volatility. There is nothing all that special about that, because anybody can do it. De-levering the illustrative 18 percent equity return assuming 60-80 percent leverage implies the asset return for the firm is only about 4-7 percent. Nominal US GDP growth isn’t too far below that (~3 percent/year for 1948 to 2021) and easily-constructed portfolios of public equities commonly achieve growth at that level on a leverage-free basis.

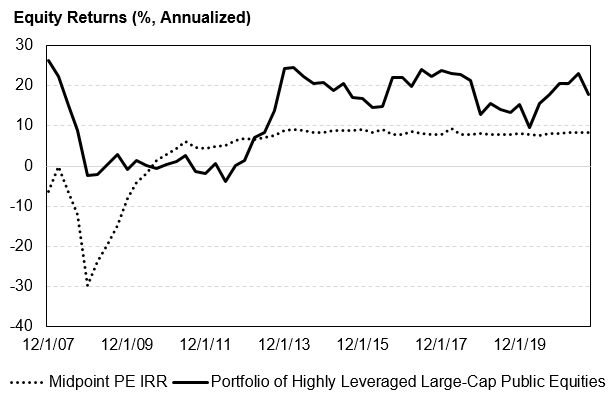

This is just one example, so it’s probably worth looking at the data more comprehensively. The chart below is a stab at that. I put this together pretty quickly, so take it with a grain of salt and as simply a conversation-starter (like everything else on this blog/site). The dotted line is the mid-point of the 2nd- and 3rd-quartile internal rates of return (IRR, or annualized equity return) of private equity funds in Bloomberg’s database. The solid line is the trailing five-year compound annual return of a portfolio of the 20 S&P 500-constituent stocks with the highest total debt/market capitalization, re-balanced monthly (i.e., it assumes that, each month, you re-rank the stocks in the S&P 500 index on the basis of total debt/market capitalization and select the top 20, selling any that have fallen out of the top 20 from the prior month and buying any that have entered the top 20). For the solid line, I’ve excluded financial institutions, since many of these have higher-than-even-private equity-level leverage and casual observation suggests they typically aren’t a focus for most private equity investments. I’ve used a five-year trailing return for the solid line as that is commonly suggested as a target holding period for private equity investments. The data for the solid line are from FactSet.

Both lines in the figure have the same general shape—there is a big decline in the aftermath of the financial crisis, followed by a strong improvement and subsequent consistency in returns. It is striking, however, how much higher the returns of the public equity portfolio are at most points in time. Over the whole period, the average is 3.7 percent for the private equity IRRs and 12.7 percent for the public equity portfolio. The implied annualized Sharpe ratio is 0.4 for the private equity line and 1.3 for the public equity line.**

Just to make sure my half-baked analysis isn’t directionally wrong even if is lacking in perfect rigor, I did a brief scan of the relevant literature and, sure enough, others who have studied this have said much the same thing. Bain & Co, along with HBS professor Josh Lerner, for example, recently found that “US buyout [i.e., private equity] returns have converged with public equity returns over the current cycle, closing a three-decade gap in performance[.]”

So what is going on? Surely, many things are, but I suspect one basic economic factor is key: competition. In the long run, competitive markets eliminate persistent abnormal excess profits such that the expected return on invested capital equals the cost of capital. There is nothing controversial about this concept. When a business arises that appears to crush it, new entrants soon follow, and competition whittles away the “excess” profits. After Uber came Lyft, after VRBO came AirBnB. The history of commerce is replete with easy-to-come-by examples. There is a hard constraint at 0 percent “excess” returns, because if the return on capital persistently falls below the cost of capital, competitors simply exit that line of business, so there is convergence toward the level of returns that is “just high enough” to fairly compensate the production inputs (labor, capital).

As it relates to private equity, stylized facts support this story. It was probably easier to find stable, cash-generating businesses whose owners were ready to cash out at less-than-full price back in the hey dey when there weren’t 200 other funds knocking down the door and investment bankers calling the owners every day and pitching their sell-side services. Since that time, private equity has grown a ton, with hundreds (thousands?) of new firms. Annual investor commitments to private equity funds in aggregate swelled from a rounding error in 1980 to almost $250 billion in 2019, with private equity assets under management in the same period rising from probably something less than $50 billion to over $1.4 trillion. As that happened, the average multiples paid in private equity buyouts rose from ~8x (enterprise value/EBITDA) in 1990 to something closer to 12x on average in 2019, according to Morgan Stanley. All of this is consistent with an increasingly competitive market, where the modal player really isn’t adding any value, even if there is still room for the best-of-the-best to outperform.

If that’s true, the obvious question is why do investors pay pretty substantial management and performance fees for exposure private equity if it’s not that much better on average than much cheaper-to-access public stocks. It’s not all that clear to me, but the theory of “conspicuous consumption” comes to mind. Private equity holds itself out as pretty prestigious and pretty smart. To date, we have all kind of accepted that story as true unquestioningly, and people want to be a part of that probably for the same reason people buy luxury goods in general. Perhaps we need a new theory of conspicuous investment.

Notes:

*Of course, private equity in the literal sense of private ownership of businesses existed long before even the 17th century and probably has always been the dominant legal form for commercial entities. Here, I am focused on “private equity” as the term is popularly used today, referring to private investment funds (as defined by the SEC) under an institutional arrangement that typically involves general partners managing day-to-day operations and investment decision-making and limited partners that contribute additional capital.

**Caveat emptor for the data nerds: these time series averages and Sharpe ratios are contaminated a bit by the fact that they embed overlapping periods. I also haven’t measured the Sharpe ratio in terms of excess returns above the risk-free rate, so it’s not theoretically perfect, but the risk-free rate was ~0% in most periods shown in the chart.

What we’re reading (10/17)

“The Dow Is On Track For Its Best October In 6 years And Third-Quarter Earnings Are Strong So Far. What Could Go Wrong?” (MarketWatch). “It is very early days, with only 8% of the S&P 500 index companies reporting third-quarter results thus far, but at least 80% of companies are beating expectations on earnings and revenue, according to John Butters, FactSet’s senior earnings analyst. Butters says that the blended growth rate (estimates and actual results) of reporting S&P 500 companies is 30%, which would, if it holds, represent the [best] [sic] earnings growth rate in over a decade.”

“A Bitcoin ETF Is Almost Here. What Does That Mean For Investors?” (Wall Street Journal). “ProShares filed plans Friday, laying the groundwork for the launch of its Bitcoin Strategy ETF. Other funds are expected to follow over the next two weeks as the Securities and Exchange Commission considers additional proposals made in August by asset managers Valkyrie Investments, Invesco and VanEck to sell bitcoin ETFs to investors. The companies don’t expect their proposals to be turned down, according to people familiar with them, though the SEC could approve, disapprove or defer any or all of the applications”

“Femtech Firms Are At Last Enjoying An Investment Boom” (The Economist). “Dame Jessica’s startup is part of a wave of “femtech” firms coming up with ways for women to overcome health problems specific to their sex. The market could more than double from $22.5bn last year to more than $65bn by 2027, reckons Global Market Insights, a research firm. Having ignored it for years—in 2020 femtech received only 3% of all health-tech funding, and a modest $14bn has been invested in it globally to date—venture capitalists are at last waking up to the opportunity. So far this year they have invested nearly $1.2bn in the industry, nearly half as much again as the annual record in 2019[.]”

“The United Nations Pension Fund Has Billions To Deploy In Private Markets” (Institutional Investor). “Pedro Guazo, the head of the $87 billion United Nations Joint Staff Pension Fund, revealed that the UNJSPF is poised to invest between $5 billion and $7 billion in the private markets in the coming years. Guazo, who spoke on the heels of the publication of the fund’s annual meeting report on October 5, said the new investments would be made possible by a shift in the organization’s asset allocation policy, among other changes.”

“Labor Flexes Its Muscle As Leverage Tips From Employers To Workers” (CNN Business). “Workers are saying enough is enough. And many of them are either hitting the picket lines or quitting their jobs as a result. The changing dynamics of the US labor market, which has put employees rather than employers in the driver's seat in a way not seen for decades, is allowing unions to flex their muscle.”

What we’re reading (10/16)

“Why Some People Invest And Others Don't” (Morningstar). “The research found that some obvious factors were at play in whether people invest or not, such as income and age. But what's different about this study was its examination of what's going on inside of people's heads, including their self-identity as an investor, the emotions they feel around investing, and their focus on preventing bad outcomes or achieving good ones.”

“Goldman Sachs Profit Rises On Deal Bonanza” (Wall Street Journal). “Goldman Sachs Group Inc. on Friday reported a 60% jump in profit and a 26% increase in revenue, beating analysts’ expectations. The Wall Street titan rounded out earnings season for the biggest U.S. banks, all of which reported double-digit profit gains. JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc. and Wells Fargo & Co. released some of the money they had set aside to deal with pandemic losses, a sign of their confidence in the bumpy economic recovery.”

“Why The IMF Is Intrinsically Conservative And Hard To Reform” (Marginal Revolution). “Successful international economic orders typically have been based on a fair degree of hegemony, whether it was the British-led gold standard of the 19th century, or the more recent post-World War II American dominance. Once you realize that, a lot of the current questions about the IMF answer themselves rather automatically. The real issue isn’t how to improve the IMF, but how we are going to cope as current hegemonies continue to lose their sway.”

“D.C. Mayor Muriel Bowser: ‘Bet On Cities’ Coming Out Of The Pandemic” (Fortune). “Washington, D.C., has been the site of multiple tumultuous events in the past year and a half, between a post-election insurrection on Jan. 6 at the U.S. Capitol and the economic fallout of the pandemic. D.C.'s mayor, Muriel Bowser (D), has dealt with it all as a working mother. But as the country strives to come out of the pandemic, she's also hopeful D.C. will be the site of something more positive: opportunity for business owners.”

“Rising Rents Are Fueling Inflation, Posing Trouble For The Fed” (New York Times). “As buyers bid up prices on single-family homes and condominiums, many people who would have otherwise moved toward homeownership found themselves unable to afford it, increasing demand for apartments and home leases. Rents have been further boosted by the large number of people searching for places with more space and home offices during the pandemic, and as millennials in their late 20s and early to mid-30s look for more autonomy.”

What we’re reading (10/15)

“Powell Says Fed Faces ‘Difficult Trade-Off’ If Inflation Doesn’t Moderate” (Wall Street Journal). “‘Almost all of the time, inflation is low when unemployment is high, so interest rates work on both problems,’ he said. That isn’t the case right now. Inflation is well above the Fed’s 2% target, and the economy is ‘far away, we think, from full employment,’ Mr. Powell said. “That’s the very difficult situation we find ourselves in.”

“Everything Is Getting More Expensive” (DealBook). “As the central bank prepares to remove emergency stimulus measures to support the economy, sustained inflation could force the Fed to move faster than it would like, before the labor market is fully healed. In newly released minutes from their latest policymaking meeting, Fed officials appear split, with ‘various’ members arguing that interest rates should stay near zero for a couple of years, while ‘a number’ said that rates would need to go up next year, with inflation most ‘likely to remain elevated in 2022 with risks to the upside.’ A recent Fed survey suggests that consumer expectations for inflation are running at historic highs.”

“Oil Spills” (Our World in Data). “Over the past four and half decades – the time for which we have data – oil spills from tankers decreased very substantially…[w]hile in the 1970s there were 24.5 large (> 700 tonnes) oil spills per year, in the 2010s the average number of large oil spills decreased to 1.7 oil spills per year. Both, large oil spills and medium sized oil spills (7-700 tonnes) are decreasing. This happened as the worldwide trade of petroleum and gas products increased.”

“China Has At Least 65 Million Empty Homes — Enough To House The Population Of France. It Offers A Glimpse Into The Country's Massive Housing-Market Problem.” (Insider). “If you drive an hour or two outside Shanghai or Beijing, you'll find something odd. The cities are still tall, and they're still modern. They're also, generally, in good condition. But unlike their bustling, Tier 1-city counterparts, they're basically empty. These are China's ghost cities.”

“Cities Aren’t The Innovation Incubators They Used To Be” (Works In Progress). “It’s time to reassess this idea [that innovation is accelerated when knowledge workers are located close to each other] in light of new evidence and new technologies for diffusing information. A steady stream of research suggests the importance of local knowledge is waning, because increased travel and online communication has facilitated the circulation of ideas across a much wider geographic domain.”

What we’re reading (10/14)

“Fed Worried About Inflation Risk As It Firmed Up Tapering Plan” (Wall Street Journal). “Minutes of their Sept. 21-22 Fed meeting, released Wednesday, revealed a stronger consensus over scaling back the $120 billion in monthly purchases of Treasury and mortgage securities amid signs that higher inflation and strong demand could call for tighter monetary policy next year. The bond purchases have been a key piece of the Fed’s effort to stimulate growth since the coronavirus pandemic disrupted the U.S. economy last year.”

“Wages Are Surging Across The Rich World” (The Economist). “When covid-19 first struck, most forecasters expected bosses to slash bonuses and yearly rises, or even to cut basic pay, as they did after the global financial crisis in 2007-09. Although wage growth did slow modestly early in the pandemic, that restraint has since been abandoned. Oxford Economics, a consultancy, finds that pay in the rich world is growing at a rate well north of its pre-pandemic average. The acceleration in compensation per employee across the OECD, a club of mostly rich countries, is equally arresting.”

“China Is Probably the Most Overvalued Property Market in the World. Evergrande is a Symptom of That” (The Market). “[E]conomically, it’s very hard to justify an economy that is two thirds of the size of the US, with having property that is worth twice as much as US property is worth. It’s not as if US property is cheap. It’s probably too expensive in the US too, which means it’s incredibly expensive in China. The amount of income it takes to buy an ordinary apartment in China is several times what it would take even in Switzerland.”

“Busting the Tech-Stock, Bond-Yield Connection Myth” (Morningstar). “It turns out that when the numbers are crunched, over the past 15 years there has only been a small inverse correlation between technology stocks and bond yields. In other words, when bond rates rise, there is a slight tendency for tech stocks to fall.”

“The Problem With America’s Semi-Rich” (Vox). “There are some defining characteristics of today’s American upper-middle class [between the proverbial 0.1 percent and the lower 90 percent.] They are hyper-focused on getting their kids into great schools and themselves into great jobs, at which they’re willing to work super-long hours. They want to live in great neighborhoods, even if that means keeping others out, and will pay what it takes to ensure their families’ fitness and health. They believe in meritocracy, that they’ve gained their positions in society by talent and hard work. They believe in markets. They’re rich, but they don’t feel like it — they’re always looking at someone else who’s richer.”

What we’re reading (10/13)

“Doing Economics As If Evidence Matters” (Paul Krugman, New York Times). A bold, provocative claim from a bold, provocative Nobel Laureate: “the political use of economic theory has tended to have a right-wing bias. But now we have evidence that can be used to check these arguments, and some don’t hold up. So the empirical revolution in economics undermines the right-leaning conventional wisdom that had dominated discourse. In that sense, evidence turns out to have a liberal bias.”

“BofA Warns The Fed Won’t Rush To Stock Market’s Rescue This Time” (Yahoo! Finance). “‘The Fed may be less willing to so easily deviate from tapering plans and talk the market back up as during the last cycle,’ BofA strategists including Riddhi Prasad and Benjamin Bowler said in a note. As reasons for their skepticism they cite equity valuations and returns accelerating to ‘extremes,’ and ‘increasingly real’ risks of inflation overshooting.”

“IMF Cuts Global Growth Forecast Amid Supply-Chain Disruptions, Pandemic Pressures” (Wall Street Journal). “Supply-chain disruptions and global health concerns spurred the International Monetary Fund to lower its 2021 growth forecast for the world economy, while the group raised its inflation outlook and warned of the risks of higher prices. In the IMF’s latest World Economic Outlook report, released Tuesday, economists cited the spread of the Covid-19 Delta variant and said the foremost policy priority is to vaccinate an adequate number of people in every country to prevent dangerous mutations of the virus.”

“Cathie Wood Says Exodus From High-Cost Cities Will Push Down Inflation As Ark Heads To St. Petersburg” (CNBC). “Wood has been vocal about her theory on deflation. While many market participants are concerned about rising prices, the Ark Invest founder expects deflation amid a breakdown in commodity prices, gridlock on tax policy in Washington and innovation trends taking off.”

“Loans Will Be The Key To Banks’ Future Fortunes” (DealBook). “Loan growth was way down at the beginning of the pandemic and has so far been slow to recover. Consumers and businesses benefited significantly from government stimulus efforts, which reduced demand for credit and helped them pay off their debts or amass more cash. But Richard Ramsden, an analyst at Goldman Sachs, wrote in a recent report that demand for loans was showing signs of increasing. ‘We believe that we have reached the inflection point,’ he wrote. “We see the outlook as increasingly encouraging.’”

What we’re reading (10/12)

“JPMorgan's Dimon Blasts Bitcoin As ‘Worthless’, Due For Regulation” (Reuters). “‘No matter what anyone thinks about it, government is going to regulate it. They are going to regulate it for (anti-money laundering) purposes, for (Bank Secrecy Act) purposes, for tax,’ Dimon said, referring to banking regulations in a conversation held virtually by the Institute of International Finance.”

“Thorstein Veblen’s Theory Of The Leisure Class—A Status Update” (Quillette). “In the past, people displayed their membership of the upper class with their material accoutrements. But today, luxury goods are more affordable than before. And people are less likely to receive validation for the material items they display. This is a problem for the affluent, who still want to broadcast their high social position. But they have come up with a clever solution. The affluent have decoupled social status from goods, and re-attached it to beliefs. “

“The Eviction Tsunami That Wasn't” (Reason). “When the U.S. Supreme Court struck down an eviction moratorium issued by the Centers for Disease Control and Prevention (CDC) in late August, housing activists, researchers, and politicians warned that an eviction tsunami would be the inevitable result…[e]conomic projections of how many evictions could be expected without a national moratorium painted an equally dire picture…Nevertheless, a month after the end of the federal eviction moratorium, these millions of evictions have yet to materialize. Indeed, while filings have increased, they remain well below historical averages almost everywhere in the country.”

“The Trillion-Dollar Coin Scheme, Explained By The Guy Who Invented It” (Vox). “In 2013, even former US Mint Director Philip Diehl agreed it would work, and over the years, influential voices like financial journalist Joe Weisenthal and New York Times columnist Paul Krugman have also promoted the idea. But all these people did not simply stumble upon this law. It was brought to their attention by Beowulf, a blog commenter and ‘reply guy’ better known as Atlanta-area attorney Carlos Mucha. Mucha conceived of the idea in a short comment on financier Warren Mosler’s blog posted on May 24, 2010, at 8:29 pm[.]”

“The Nobel Prize In Economics Celebrates An Empirical Revolution” (The Economist). “[T]heory [once] ruled the roost and empirical work was a poor second cousin. ‘Hardly anyone takes data analysis seriously,’ declared Edward Leamer of the University of California, Los Angeles, in a paper published in 1983. Yet within a decade, new and innovative work had altered the course of the profession, to such an extent that the lion’s share of notable new research today is empirical. For helping enable this transition David Card of the University of California at Berkeley shares this year’s economics Nobel prize, awarded on October 11th, with Joshua Angrist of the Massachusetts Institute of Technology and Guido Imbens of Stanford University.”

What we’re reading (10/11)

“A Nobel Prize For The Credibility Revolution” (Marginal Revolution). “The Nobel Prize goes to David Card, Joshua Angrist and Guido Imbens. If you seek their monuments look around you. Almost all of the empirical work in economics that you read in the popular press (and plenty that doesn’t make the popular press) is due to analyzing natural experiments using techniques such as difference in differences, instrumental variables and regression discontinuity. The techniques are powerful but the ideas behind them are also understandable by the person in the street which has given economists a tremendous advantage when talking with the public. Take, for example, the famous minimum wage study of Card and Krueger (1994) (and here). The study is well known because of its paradoxical finding that New Jersey’s increase in the minimum wage in 1992 didn’t reduce employment at fast food restaurants and may even have increased employment. But what really made the paper great was the clarity of the methods that Card and Krueger used to study the problem.”

“We May Have Reached Peak Earnings” (CNN Business). “Corporate profits soared in the first half of this year, largely because of favorable comparisons to last year's weak earnings. The Covid shutdown of the economy hit major companies hard in the first half of 2020. But as companies get set to report their third-quarter results in the next few weeks, some Wall Street analysts are concerned the rate of earnings increases will start to slow. This may be the peak for the foreseeable future.”

“There Is Shadow Inflation Taking Place All Around Us” (New York Times). “Many types of businesses facing supply disruptions and labor shortages have dealt with those problems not by raising prices (or not by only raising prices), but by taking steps that could give their customers a lesser experience. A hotel room might cost the same as a year ago — but no longer include daily cleaning services because of a shortage of housekeepers. Some restaurants are offering limited service, with waiters stretched thin. Would-be car buyers are being advised to be flexible on the color and even make and model, lest they face a long wait to get their new wheels.”

“San Francisco Fed's Daly: Too Soon To Say Job Market 'Stalling'“ (Reuters). “The U.S. job market will continue to feel the effects of COVID-19, but it is too soon to say it is ‘stalling,’ San Francisco Federal Reserve President Mary Daly said on Sunday. ‘It's going to have these ups and downs, especially with the Delta variant,’ Daly said on the CBS weekend news program ‘Face the Nation’ when asked about a second straight month of disappointing job growth in September.’

“Is It Time For A New Economics Curriculum?” (The New Yorker). “Jonathan Gruber, who teaches introductory economics at M.I.T., felt that core might introduce too much complexity for a foundational course. He worried that so much emphasis on the ethical and political dimensions of economics might make the subject feel like a different discipline altogether. ‘The question is, do you want the students to feel like they’re coming out of, you know, to be blunt, a sociology class or an economics class?’ Gruber said. Still, he welcomed the greater emphasis on the imperfections of markets. ‘Economics is a right-wing science,’ he told me. ‘We teach students that the market is always right. And that’s just wrong.’”

What we’re reading (10/10)

“Is The ‘Unicorn’ Boom Turning Into A Bubble?” (Fortune). “The number of pre-IPO startups worth more than $1 billion has skyrocketed globally…[a] total of 136 startups achieved unicorn status in Q2 of 2021 alone, more than in all of 2020. After the initial meeting with a founder, investment decisions are made "in a matter of days, or maybe even a week,” says Sumi Das, partner at Alphabet’s private equity arm, CapitalG. A couple years ago, that was typically a two- or three-week process. And it’s not just VCs sloshing money into startups: Hedge funds, mutual funds, and sovereign wealth funds are entering the private market, both inside and outside the U.S.”

“A Bunch Of Fitness Companies Have Jumped Into The IPO Market This Year. It’s Not Working Out.” (MarketWatch). “Has the U.S. IPO market reached peak fitness? It may have, based on Thursday’s market, which saw the latest fitness company to go public — Life Time Group Holdings — flounder in early trade, while another expected this week, iFit Health & Fitness, postponed its deal, citing adverse market conditions.”

“Cotton Prices Just Hit A 10-Year High. Here’s What That Means For Retailers And Consumers” (CNBC). “Cotton prices surged to a 10-year high on Friday, reaching $1.16 per pound and touching levels not seen since July 7, 2011. The price of the commodity rose roughly 6% this week, and is up 47% year to date. Analysts note that gains are being intensified further from traders rushing to cover their short positions.”

“An SEC Rule Was Meant To Protect Individual Investors. Chaos Ensued.” (Wall Street Journal). “ [A] rule from the Securities and Exchange Commission went into effect at the end of September, generally preventing brokers from providing public price quotations on securities issued by companies that don’t release current financial information…[u]nder the SEC rule, many brokers have stopped offering price quotes on…[thousands of] companies that don’t provide public information.”

“We Have No Theory Of Inflation” (Value Added). “Right now, the debate about how transitory or temporary the global spike in inflation will be is the hottest topic in macro. Between them, Goodhart and Rudd have done a good job of demonstrating that the best answer might be ‘we don’t know’. None of the existing models provide a solid basis for forecasting. Many of the people claiming that inflation is definitely staying high have been saying much the same thing for a decade or more, while many of those insisting that it is transitory failed to spot the coming spike.”

What we’re reading (10/9)

“Wall Street Isn't Sweating The Mixed Jobs Report” (CNN Business). “America added far fewer jobs in September than expected, but investors didn't seem too disappointed: Stocks were mostly unchanged Friday as Wall Street took solace that the unemployment rate continues to drop after the pandemic-fueled spike last year.”

“Markets Are Telling The Fed To Start Tapering Now After Big Miss On September Jobs Report, Says Mohamed El-Erian” (Insider). “‘…[T]he message from the market to the Fed is: 'Go ahead and taper, we expect you to.’…El-Erian has been banging the drum for months on the need for the Fed to taper as soon as possible. Last month, he blamed the central bank for bond-market turmoil, saying markets would begin to question the Fed's judgment on inflation the longer it waited to taper.”

“Global Supply-Chain Problems Escalate, Threatening Economic Recovery” (Wall Street Journal). “Earlier this year it cost more than five times as much to ship goods from China to South America compared with last year’s pandemic low, according to U.N. Conference on Trade and Development data. Freight rates on the more heavily trafficked China-North America route more than doubled.”

“The Bretton Woods Credibility Crisis” (Project Syndicate). “[F]ollowing the 2018 report, there were complaints about the data that had been used, leading the World Bank to commission the highly regarded law firm WilmerHale to investigate. Its report, issued last month, found serious irregularities with respect to China’s ranking in the 2018 report. The investigators report that Kristalina Georgieva, the Bank’s then-CEO (second in command) who has since become managing director of the IMF, urged staff to reconsider the results for China, and then ‘explored … ways to change the methodology to raise China’s ranking.’ The report also points out that the Bank had an interest in placating China, because it was seeking Chinese support for a capital increase at the time.”

“Why Tesla Bought Bitcoin” (Works In Progress). “Bitcoin has weathered its fair share of theoretical criticisms over the years. It’s just like tulips. It’s insecure. It’s technically unsound. It’s on the wrong side of a global macroeconomic network effect. It’s economically unworkable. It’s wasteful. It’s dangerous. It’s stupid. Besides, if it does eventually overcome these problems, the government will shut it down. And yet, there Bitcoin stands—thriving.”

What we’re reading (10/8)

“America's CEOs Are Losing Confidence In The Economy” (CNN Business). “US business leaders are still upbeat about the economic recovery. But they're not as confident as they were just a few months ago, and they blame the Delta variant and a super tight labor market for the drop in sentiment. The Conference Board, a leading business research think tank, reported Thursday a steep slide in its CEO confidence index for the third quarter.”

“Builders Hunt For Alternatives To Materials In Short Supply” (Wall Street Journal). “Shortages of key construction materials are forcing some builders and contractors to turn to substitutes and hunt for alternative suppliers as they rush to meet high demand for new housing. Construction companies are looking for replacements and new sources for everything from wood paneling to ceiling joists to pipes, saying that potentially higher costs and added complications to design and construction can be preferable to putting a project on hold for months while waiting for planned supplies.”

“Banks Don’t Want Your Money Right Now” (Vox). “US interest rates and inflation are on the rise again, which means Americans can expect to pay higher rates for mortgages, auto loans, and credit cards. But don’t expect it to lead to higher interest on your savings account anytime soon. Banks don’t want your money. That’s why they’re offering such low rates.”

“Yet Another Covid Victim: Capitalism” (New York Times). “Professor Stiglitz — winner of the 2001 Nobel Memorial Prize in Economic Sciences, a former chief economist at the World Bank and a professor at Columbia University — said in a pre-conference interview that the private sector had proven incapable of responding alone to the global health challenge and that government had a big role to play.”

“Want to Pick the Best Stocks? Pick the Happiest Companies.” (Institutional Investor). “According to a paper published on October 1, a portfolio that includes companies with high employee-satisfaction ratings can measurably outperform a portfolio that doesn't feature such firms. And these returns were even better in crisis periods. Researchers Hamid Boustanifar and Young Dae Kang at EDHEC Business School in Nice, France, said the paper, entitled Employee Satisfaction and Long-run Stock Returns, 1984-2020, builds on a similar 2011 study by expanding the dataset and controlling for more variables.”

What we’re reading (10/7)

“Central Banks And The Looming Financial Reckoning” (Project Syndicate). “Across the advanced economies (and in many emerging markets), risk assets, notably equity and real estate, appear to be materially overvalued, despite recent minor corrections. The only way to avoid this conclusion is to believe that long-run real interest rates today (which are negative in many cases) are at or close to their fundamental values. I suspect that both the long-run real safe interest rate and assorted risk premia are being artificially depressed by distorted beliefs and enduring bubbles, respectively. If so, today’s risk-asset valuations are utterly detached from reality.”

“You Know Who Don’t Want To End Banking As We Know It? Banks.” (Dealbreaker). “You’d have thought Gary Gensler was bad enough. Rohit Chopra in Mick Mulvaney’s seat? Even worse. The decreasing likelihood that Jay Powell will at least be around to keep an eye on their interests? Tough to take. But this communist [Saule Omarova] who wants to “end banking as we know it” as head of the most important banking regulator in the country? That is simply too much for the banks to take.”

“Why Wall Street Cheers China, Despite Growing Business Unease” (The Economist). “This year has been unsettling for Chinese business. The ruling Communist Party has gone after the private sector industry by industry. The stock markets have taken a huge hit. The country’s biggest property developer is on the verge of collapse. But for some of the biggest names on Wall Street, China’s economic prospects look rosier than ever. BlackRock, the world’s biggest asset manager, urged investors to increase their exposure to China by as much as three times.”

“Do Pandemics Normally Lead To Rising Inflation?” (The Economist). “That covid-19 might usher in a prolonged spell of high inflation would buck a historical trend. A recent paper by Dennis Bonam and Andra Smadu, two economists at the Dutch central bank, looks at the effect of pandemics on inflation and concludes that they typically lead to lower, not higher, price pressures. Using data going baIck to the 14th century, covering six European countries and 19 pandemics, the authors find that such events have historically caused inflation to fall for more than a decade, on average, yielding an inflation rate about 0.6 percentage points lower than if the pandemic had not occurred. The more prolonged and severe the outbreak, the more pronounced and persistent the negative effects on trend inflation.”

“‘I Found A Flaw In Your System, And I Took Advantage Of it.’ Florida Man Filed 745 Tax Returns In 4 Years, Collecting $235K In Bogus Refunds” (MarketWatch). “Most people dread having to file their taxes, but not Damian Barrett, authorities say. Over a four-year period, the Florida man filed 745 tax returns in 19 different states, according to the IRS. The payoff: $235,000 in tax refunds he wasn’t entitled to. Barrett, 40, who pleaded guilty in July to mail fraud, identity theft and filing false tax returns, was sentenced this week to 4 ½ years in federal prison, according to prosecutors in Oregon, where he had filed 348 returns alone.”

What we’re reading (10/6)

“Is The Stock Market Open At 3 a.m.? This Startup Says It Should Be” (Wall Street Journal). “Under decades-old conventions, the bulk of stock trading takes place between 9:30 a.m. and 4 p.m. ET on weekdays, and exchanges shut down for holidays, such as Good Friday and Washington’s Birthday. In contrast, 24 Exchange would operate like the foreign-exchange and cryptocurrency markets, which run continuously. The three-year-old startup already offers trading in FX and crypto. Its parent company, 24 Exchange Bermuda Ltd., is incorporated in Bermuda, but the proposed stock exchange would be run by a U.S. subsidiary.”

“The Fractionalization Of Everything” (Vox). “With emerging technologies such as blockchain, the increasing power and importance of retail traders, and a growing appetite for new assets, everything from shoes to artwork to classic cars is being broken up into pieces and offered to investors in bite-sized portions through a process called fractionalization…[o]ne interesting caveat to most fractional investments aimed at retail investors is that buyers don’t actually own the things they buy. They’re simply buying a stake in the asset, betting that it will rise in value and they’ll be able to sell their portion at a higher price than what they paid.”

“Bond Yields Are Disconnected From Economic Fundamentals. Investors Shouldn’t Expect That To Change.” (Institutional Investor). “Interest rates relative to inflation aren’t getting back to normal anytime soon. That’s because institutions, including sovereign reserve managers, commercial banks, and pension funds are buying bonds for regulatory reasons or to match their future liabilities, breaking the relationship between a bond’s price and the underlying fundamentals, according to the newly formed Strategic Investment Advisory Group of J.P. Morgan Asset Management.”

“Natural Gas Crisis Pushes U.S. Prices To Highest Since 2008” (Bloomberg). “Natural gas futures jumped to the highest settlement price in 12 years in New York as global gas supply shortages stoke concerns for U.S. shortages…As the northern hemisphere heads into winter-heating season, low U.S. auxiliary supplies have sparked concerns about potential shortages as demand for the furnace fuel ramps up. Gas futures rose 9.5% to close settle at $6.312 per million British thermal units on the New York Mercantile Exchange, the highest close since December 2008.”

“A Look At The Lavish Real Estate Revealed In The Pandora Papers” (Architectural Digest). “Unlike some other famed documents revealing the corruption encouraged by the world’s most prominent power players, this specific collection of 12 million confidential files centers on the financial secrets—luxury property machinations—of global political leaders. Everyone from Pakistani Prime Minister Imran Khan to former British Prime Minister Tony Blair appear in the report. Indeed, the Pandora Papers extend far beyond these public officials and heads of state; the Papers span their entire inner circle.”

What we’re reading (10/5)

“Stock, Bond And Real Estate Prices Are All Uncomfortably High” (Robert Shiller, New York Times). “The prices of stocks, bonds and real estate, the three major asset classes in the United States, are all extremely high. In fact, the three have never been this overpriced simultaneously in modern history. What we are experiencing isn’t caused by any single objective factor. It may be best explained as a result of a confluence of popular narratives that have together led to higher prices.”

“Do Inflation Expectations Matter For Inflation?” (Marginal Revolution). “Many people (NYT) are talking about the new paper by Jeremy Rudd on exactly this topic — Rudd is skeptical that they matter very much. So I went to read the paper, and I have to say I am baffled. It didn’t change my priors at all. I didn’t see new empirical estimates, or new theoretical arguments, and furthermore I didn’t see the most relevant factors discussed much. I did see a lot of pokes at Friedman, Phelps, and Lucas (and there is also an introductory assertion that, even given enough time, markets with flexible prices do not clear. Then he goes on to deny that the theory of household choice is sufficient to derive downward-sloping demand…why do that???).”

“The Age Of Fossil-Fuel Abundance Is Dead” (The Economist). “In recent weeks…it is a shortage of energy, rather than an abundance of it, that has caught the world’s attention. On the surface, its manifestations are mostly unconnected. Britain’s miffed motorists are suffering from a shortage of lorry drivers to deliver petrol. Power cuts in parts of China partly stem from the country’s attempts to curb emissions. Dwindling coal stocks at power stations in India are linked to a surge in the price of imports of the commodity. Yet an underlying factor is expected to make scarcity even worse in the next few years: a slump in investment in oil wells, natural-gas hubs and coal mines”

“Empty Buildings In China’s Provincial Cities Testify To Evergrande Debacle” (Wall Street Journal). “Rows of residential towers, some 26 stories high, stand unfinished in this provincial city about 350 miles west of Shanghai, their plastic tarps flapping in the wind. Elsewhere in Lu’an, golden Pegasus statues guard an uncompleted $9 billion theme park that was supposed to be bigger than Disneyland. A planned $4 billion electric-vehicle plant, central to local leaders’ economic dreams, remains a steel frame with overgrown vegetation spilling into the road.”

“‘Some Are Just Psychopaths’: Chinese Detective In Exile Reveals Extent Of Torture Against Uyghurs” (CNN Business). “The methods included shackling people to a metal or wooden ‘tiger chair’ -- chairs designed to immobilize suspects -- hanging people from the ceiling, sexual violence, electrocutions, and waterboarding. Inmates were often forced to stay awake for days, and denied food and water, he said.”