What we’re reading (9/29)

“Stocks Could Slide Further As Interest Rates Rise And Big Tech Drags The Market” (CNBC). “Big Tech and growth names are sensitive to higher rates since their high valuations are based on future growth and cash flow. When interest rates rise, the value of that future cash flow is discounted. But Oppenheimer technical analyst Ari Wald said the fact that Big Tech is selling off means that those popular large cap growth stocks are joining the many other stocks that already had big downturns. ‘It hadn’t spilled over into the large cap and now it has. We see that as a sign of capitulation,’ he said. Wald added he sees more downside for the S&P 500′s July low of about 4,230.”

“Men Over 45 Who Identify As Having ‘Excellent Investment Experience’ Are More Likely To Panic Sell During A Market Downturn, MIT Study Finds” (Insider). “[A] study from MIT has identified the cohort of people that are most likely to panic sell at the worst possible time: men over the age of 45 who are either married or identify as having ‘excellent investing experience.’ Cohorts with more dependents or an account size of less than $20,000 are also more likely to ‘freak out’ and panic sell. The MIT paper analyzed the trading behavior of more than 600,000 brokerage accounts attached to more than 200,000 households to identify who is selling and potentially be able to predict when they might sell in the future.”

“Elizabeth Warren Will Oppose Fed Chair Powell’s Renomination, Calls Him ‘Dangerous Man’ To Lead Fed” (CNN Business). “Democratic Senator Elizabeth Warren announced Tuesday that she will oppose Federal Reserve Chairman Jerome Powell's renomination, making her the highest-profile lawmaker to do so. ‘Your record gives me grave concern. Over and over you have acted to make our banking system less safe. And that makes you a dangerous man to head up the Fed,’ Warren told Powell during a Senate Banking Committee hearing.”

“Houlihan Lokey Co-President Accused Of Double-Dealing As He Bought Jet With Tech CEO” (New York Post). “A top Wall Street banker is being accused of bizarre double-dealing at a California tech firm where he serves as a board member. Scott Adelson, co-president of the prominent investment bank Houlihan Lokey, allegedly leaked information to the would-be acquirer of QAD Inc. — a publicly traded software firm based in Santa Barbara, Calif. — even as he secretly entered a deal to buy a private jet with the company’s CEO, according to an explosive lawsuit.”

“Federal Judges With Financial Conflicts” (Wall Street Journal). “The Wall Street Journal analyzed nearly a decade’s worth of legal and financial records and discovered 131 federal judges who unlawfully heard cases where they had a financial interest…[o]ver the past several weeks, the Journal has informed these judges of their recusal violations. As a result, 56 federal judges have notified courts in 329 cases around the U.S. that they heard cases improperly and that parties to the case could ask for them to be reopened.”

What we’re reading (9/28)

“Why Do We Think That Inflation Expectations Matter For Inflation? (And Should We?)” (Jeremy Rudd, Federal Reserve). “Economists and economic policymakers believe that households’ and firms’ expectations of future inflation are a key determinant of actual inflation. A review of the relevant theoretical and empirical literature suggests that this belief rests on extremely shaky foundations, and a case is made that adhering to it uncritically could easily lead to serious policy errors.”

“Here Comes $90 Oil” (CNN Business). “The V-shaped recovery in the oil patch continues to take even the biggest bulls on Wall Street by surprise. Goldman Sachs ramped up its already optimistic forecast on Sunday, calling for Brent crude to hit $90 a barrel by the end of the year. That's up from its previous call for $80. The Wall Street bank expects US crude to hit $87 a barrel, up from $77 previously.”

“Are Investors Becoming Warier Of Chinese Assets?” (The Economist). “If investors expect Chinese policy to continue to be volatile, then they could start to demand an additional risk premium for holding a swathe of assets. ‘The intensity of policy change has caught investors off guard,’ says Chetan Ahya of Morgan Stanley, a bank. ‘It’s not clear to investors what the end game is for each sector, so there’s a lot of uncertainty, and it’s this uncertainty that adds to the risk.’ Indeed, a risk premium may already be becoming apparent for some assets.”

“Activist Hedge Fund Starboard Has Big Stake In Huntsman” (Wall Street Journal). “Activist hedge fund Starboard Value LP has a more-than-8% stake in Huntsman Corp. and plans to agitate for change at the chemicals producer, according to people familiar with the matter. Huntsman has a market value of roughly $6.3 billion, making Starboard’s stake worth around $500 million or more. Huntsman, based in The Woodlands, Texas, makes chemicals for a variety of uses including plastics, cars and construction materials. The exact changes Starboard intends to push for to improve its stock performance couldn’t be learned. Huntsman’s shares are little changed since the company’s 2005 initial public offering, closing Monday at $28.07 versus $24.50 on their first day of trading.”

“Goldman Sachs, Ozy Media And A $40 Million Conference Call Gone Wrong” (New York Times). “When YouTube learned that someone had apparently impersonated one of their executives at a business meeting, its security team started an investigation, the company confirmed to me. The inquiry didn’t get far before a name emerged: Within days, Mr. Watson had apologized profusely to Goldman Sachs, saying the voice on the call belonged to Samir Rao, the co-founder and chief operating officer of Ozy, according to the four people.”

What we’re reading (9/27)

“It's Hard To Be Bearish On The Stock Market As Risk-Happy Millennials Inherit $2 Trillion Per Year, Fundstrat's Tom Lee Says” (Insider). “‘Bull market until 2038? This is a possible base case...[i]f demographics are destiny, US stocks will do very well,’ Lee wrote in June, pointing out that every stock market peak since 1900 has coincided with a generation's peak. It is a theory shared by ARK Invest's Cathie Wood, who has cited Lee's research as evidence. ‘I do believe that both crypto and the equity markets are going to be powered by millennials,’ Wood said at a conference last week.”

“Individuals Embrace Options Trading, Turbocharging Stock Markets” (Wall Street Journal). “By one measure, options activity is on track to surpass activity in the stock market for the first time ever…[s]ome analysts say the zeal for options trading is translating to bigger swings in individual stocks, and fueling the momentum behind many rallies. When individual investors buy call options, the Wall Street firms that sell options often hedge their positions by buying the shares, further contributing to rising markets.”

“Going Public? Here Is A How-To Guide” (The Economist). “[G]oing public combines mixed emotions, much complexity and myriad idiosyncracies. Despite that, and undeterred by recent wobbles in equity markets, startups have been listing in droves. So far this year tech firms have raised $60bn, according to Dealogic, a data provider, more than at the height of the dotcom bubble in 2000. Include all types of business and the figure is close to $250bn…[o]ne headhunting agency is said to have more than 50 searches under way for finance chiefs at startups hoping to go public soon.”

“Goldilocks Is Dying” (Nouriel Roubini, Project Syndicate). “The recovery in the first half of 2021 has given way recently to sharply slower growth and a surge of inflation well above the 2% target of central banks, owing to the effects of the Delta variant, supply bottlenecks in both goods and labor markets, and shortages of some commodities, intermediate inputs, final goods, and labor. Bond yields have fallen in the last few months and the recent equity-market correction has been modest so far, perhaps reflecting hopes that the mild stagflation will prove temporary.”

“The Supply-Chain Mystery” (The New Yorker). “Americans are not facing Soviet-style empty shelves, or having to scrap for the basics. In aggregate, we are hardly in a condition of scarcity. Still, supply-chain trouble suggests that something is off with the way we’re operating in the world, and that we don’t yet know the extent of our vulnerabilities. The issues can also be a serious impediment to a broader economic recovery.”

What we’re reading (9/26)

“What The ‘Smart Money’ Knows About China’s Evergrande Crisis” (Wall Street Journal). “Between its inception at the end of 1992 and this Aug. 31, the MSCI China stock index has returned an average of 2.2% annually, including dividends. Over the same period, the MSCI Emerging Markets index grew 7.8% annually; the S&P 500, 10.7%. That covers a nearly 30-year period in which China’s economy often grew by at least 10% a year. Nevertheless, you would have earned much better returns on U.S. Treasury securities than on Chinese stocks. Maybe China, which holds more than $1 trillion in U.S. Treasurys, knew something that Wall Street didn’t. And knowing what the Chinese government is thinking is harder than ever.”

“Costco, Nike And FedEx Are Warning There’s More Inflation Set To Hit Consumers As Holidays Approach” (CNBC). “Shipping bottlenecks that have led to rising freight costs are cooking up a holiday headache for U.S. retailers. Costco this week joined the long list of retailers sounding the alarm about escalating shipping prices and the accompanying supply chain issues. The warehouse retailer, which had a similar cautionary tone in May, was joined by athletic wear giant Nike and economic bellwethers FedEx and General Mills in discussing similar concerns. The cost to ship containers overseas has soared in recent months. Getting a 40-foot container from Shanghai to New York cost about $2,000 a year and a half ago, just before the Covid pandemic. Now, it runs some $16,000, according to Bank of America.”

“How Bad Are Supply Chains? Costco Is Renting Ships” (CNN Business). “Costco (COST), home of the ultimate big box store, is not mincing words about what it's like to run a consumer business in the middle of a pandemic. ‘Inflationary factors abound: higher labor costs, higher freight costs, higher transportation demand, along with container shortages and port delays, increased demand in certain product categories, various shortages of everything from computer chips to oils and chemicals, higher commodities prices,’ Chief Financial Officer Richard Galanti told analysts after markets closed Thursday. ‘It's a lot of fun right now.’ […] [S]upply chains are so badly tangled that the company said it has chartered three ocean vessels for the next year to transport containers between Asia and the United States and Canada.”

“Warren Buffett May Not Be Into Crypto, But His Granddaughter Is” (Institutional Investor). “For Nicole Buffett, creating NFTs of her paintings, especially during the pandemic, when in-person art shows and gallery openings have been a near impossibility, allowed her to expand her circle of buyers globally — a large proportion of them young, entrepreneurial, and tech-savvy. ‘NFTs are really art as money, art as currency, which means there’s more accessibility for artists and for people who want to buy art,’ she tells Institutional Investor. ‘It’s great just to have more eyeballs on the work…I will help people get set up so they can buy art on the blockchain, but the currency of the NFT space is Ethereum. I do still take dollars for physicals.’”

“A Hamster Has Been Trading Cryptocurrencies In A Cage Rigged To Automatically Buy And Sell Tokens Since June - And It's Currently Outperforming The S&P 500” (Insider). “A hamster in Germany is redefining ‘A Random Walk Down Wall Street’ author Burton Malkiel's belief that a blindfolded monkey throwing darts at a stock ticker list in the newspaper could do just as good as a human investment professional. The livestreamed hamster, named Mr. Goxx, has been independently trading a portfolio of various cryptocurrencies since June 12, and so far its performance has been impressive. As of Friday, the portfolio was up nearly 24%, according to the @mrgoxx twitter feed that documents daily performance, along with every trade made by the hamster. Mr. Goxx's performance outpaces bitcoin and the S&P 500 over the same time period.”

October picks available soon

We’ll be publishing our Prime and Select picks for the month of October before Friday, October 1 (the first trading day of the month). As always, we’ll be measuring SPC’s performance for the month of September, as well as SPC’s cumulative performance, assuming the sale of the September picks at the closing price (at the mid-point of the closing bid and ask prices) on the last trading day of the month (Thurs., September 30). Performance tracking for the month of October will assume the October picks are bought at the open price (at the mid-point of the opening bid and ask prices) on the first trading day of the month (Friday, October 1).

What we’re reading (9/25)

“The European Energy Crisis Is About To Go Global” (OilPrice.com). “It was only a matter of time, really. In a globalized world, energy crunches can hardly remain regionally contained for very long, especially in a context of damaged supply chains and a rush to cut investment in fossil fuels. The energy crunch that began in Europe earlier this month may now be on its way to America. For now, all is well with one of the world's top gas producers…[b]ut supply is tightening, Argus reported earlier this month. In July, according to the report, U.S. coking coal exports dropped by as much as 20.3 percent from June.”

“Here Come The Crypto Rules” (DealBook). “Financial regulators are racing to regulate stablecoins. These digital currencies pegged to a stable asset like the dollar are used in crypto trading, banking and decentralized finance, addressing the problem of price volatility that plagues Bitcoin and others. Stablecoins have become an important bridge between digital currencies and the traditional financial system. But despite their name, stablecoins may be shaky. The urgency among regulators to rein in the industry has, in turn, generated a flurry of crypto industry lobbying all over Washington…[i]n their short history, lightly regulated stablecoin issuers have shown that they don’t always have the cash reserves they claim.”

“China Declares Cryptocurrency Transactions Illegal; Bitcoin Price Falls” (Wall Street Journal). “China’s central bank said all cryptocurrency-related transactions are illegal, reinforcing the country’s tough stance against digital rivals to government-issued money. In a statement posted on its website on Friday afternoon, the People’s Bank of China said the latest notice was to further prevent the risks surrounding crypto trading and to maintain national security and social stability. Cryptocurrencies weakened following the statement.”

“Did I Miss The Value Turn?” (Research Affiliates). “When most liquid asset classes are set to deliver a negative or near-zero real return, value stocks stand out as the only asset class likely to generate a 5%–10% real return over the coming decade. The opportunity to buy value stocks may be short-lived and we may wait decades for an opportunity of a similar scale.”

“Bar Talk: Informal Social Interactions, Alcohol Prohibition, And Invention” (Michael Andrews, working paper). “To understand the importance of informal social interactions for invention, I examine a massive and involuntary disruption of informal social networks from U.S. history: alcohol prohibition. The enactment of state-level prohibition laws differentially treated counties depending on whether those counties were wet or dry prior to prohibition. After the imposition of state-level prohibition, previously wet counties had 8-18% fewer patents per year relative to consistently dry counties.”

What we’re reading (9/24)

“Evergrande Debt Crisis Is Financial Stress Test No One Wanted” (Bloomberg). “Sunny Peninsula…was supposed to house 5,000 families in dozens of towers spread across an area the size of 30 soccer fields. Many of the buyers were white-collar workers benefiting from the fastest urbanization in human history. But the project now looks more like the set of a disaster movie. Half-finished apartment blocks stand empty and abandoned…China Evergrande Group, until recently the world’s largest property developer, owns dozens of stalled sites like Sunny Peninsula across China. Buckling under more than $300 billion in liabilities, the company is close to collapse, leaving 1.5 million buyers waiting for finished homes.”

“Who’s Buying Evergrande?” (New York Times). “International investors in Evergrande’s bonds are preparing for turmoil — and in some cases buying more. Evergrande’s debt is in the portfolios of man major investment firms, and some hedge funds have been adding more to their holdings as prices have tumbled. A group of bondholders has tapped restructuring advisers at Kirkland & Ellis and at Moelis. For its part, Evergrande has hired the firms Houlihan Lokey and Hong Kong Admiralty Harbour Capital. How might the negotiations play out?”

“Evergrande’s Struggles Reflect China’s Efforts to Rein in Multiyear Debt Boom” (Wall Street Journal). “China is hardly alone in its fondness for debt, but unlike the U.S., China doesn’t borrow to cut taxes or finance social transfers. It instead invests in manufacturing, infrastructure and property. It is a logical model so long as the investment genuinely makes the country more productive. For a long time, it did. But China isn’t immune to the law of diminishing returns. Since 2008, it has needed ever more debt to deliver the same increment to economic output. Between 2008 and 2019, total debt—government, household and business—rose from 169% to 306% of gross domestic product, but GDP growth fell from 10% to 6%.”

“Evergrande’s Crisis Highlights China’s Shortcomings” (The Economist). “Part of what makes China’s financial industry daunting is its size. Banking assets have ballooned to about $50trn and they sit alongside a large, Byzantine system of shadow finance. Total credit extended to firms and households has soared from 178% of gdp a decade ago to 287% today. The industry suffers from opacity, a lack of market signals and the erratic application of rules. Property is part of the problem. Families funnel their savings into apartments rather than casino stockmarkets or state-run banks. Real-estate developers raise debts in the shadow-banking system in order to finance epic construction booms. As well as being big, the system is inefficient at allocating capital, dragging down growth.”

“Why The Head Of The IMF Should Resign” (The Economist). “A new investigation has found that [World] [B]ank staff improperly altered the scores of China and three other countries. They wanted to spare China an embarrassing fall in the [Doing Business] rankings in 2017, just as its reforms were gathering steam. According to the investigation, the China tweaks were carried out at the behest of the bank’s then president, Jim Yong Kim, and his second-in-command, Kristalina Georgieva, who is now head of the IMF.”

What we’re reading (9/23)

“Fed’s Intentions On Rates Remain Muddled” (Wall Street Journal). “Getting to zero [in monthly asset purchases] is important to Fed officials because they effectively see completing the tapering process as a precondition to raising rates: They don’t want to find themselves in a situation where they need to hike while they are still purchasing assets. But they have tried to frame this as merely providing them with an option to tighten, a decision that will ultimately hinge on how much progress the job market has made, and how sticky the recent bout of inflation ends up being.”

“Fed Chair Powell Says He's Powerless To Protect The Economy If Congress Lets The US Default On Its Debt” (Insider). “The Federal Reserve won't come to the economy's rescue if the US defaults on its debt, Jerome Powell, the chair of the central bank, said Wednesday. Congress is, once again, coming dangerously close to a debt-ceiling crisis. Lawmakers have until mid-October to either raise or suspend the borrowing limit, or allow the US to default on its debt. The latter outcome would freeze spending on several critical public programs, spark massive job losses, throw financial markets into chaos, and likely plunge the US into a self-inflicted recession.”

“Beyond Evergrande’s Troubles, A Slowing Chinese Economy” (New York Times). “Global markets have watched anxiously as a huge and deeply indebted Chinese property company flirts with default, fearing that any collapse could ripple through the international financial system. China Evergrande Group, the developer, said on Wednesday that it had reached a deal that might give it some breathing room in the face of a bond payment due the next day. But that murky arrangement doesn’t address the broader threat for Beijing’s top leaders and the global economic outlook: China’s growth is slowing, and the government may have to work harder to rekindle it.”

“Crypto Equated To Toxic Pre-Crisis Swaps By Banking Watchdog” (Bloomberg). “The U.S. agency that had once been the great hope of the cryptocurrency world is now issuing strong warnings to the industry that it’s in danger of echoing the toxic culture before the 2008 financial crisis. Michael Hsu, the acting chief of the Office of the Comptroller of the Currency, argued Tuesday that cryptocurrencies and decentralized finance may be evolving into threats to the financial system in much the same way certain derivatives brought it near collapse more than a decade ago. Notorious credit default swaps were engineered by math wizards in much the same way crypto has emerged, he said. ‘Crypto/DeFi today is on a path that looks similar to CDS in the early 2000’s,’ Hsu told the Blockchain Association in a webcast.”

“Crypto Faces Existential Threat As Crackdown Gathers Steam” (Bloomberg). “Cryptocurrency firms are fighting for lobbyists and fielding subpoenas in what could be an existential fight over how the multitrillion-dollar industry should be regulated…[a]s the cryptocurrency industry gears up for a regulatory battle, some lobbyists, who asked to withhold their names to discuss client matters, said they were so deluged by crypto firms looking to hire them in August that they had to turn down some potential clients. Some of the crypto firms said they were being targeted by or expected to be targeted by regulators, the lobbyists said.”

What we’re reading (9/22)

“How Bad Is It?” (DealBook). “On top of Evergrande, a number of other Chinese property developers also appear “highly distressed,” said Jenny Zeng of AllianceBernstein. Goldman Sachs strategists estimate that an Evergrande collapse could cut China’s G.D.P. by $350 billion in the next year. But for now, the global repercussions of Evergrande’s troubles aren’t considered on the same scale as those that followed Lehman’s collapse, even if some of the debt owed by Chinese developers is held by foreign firms, who could get burned if the cash isn’t there.”

“Why Everybody’s Hiring But Nobody’s Getting Hired” (Vox). “The Bureau of Labor Statistics says there are 8.4 million potential workers who are unemployed, but it also says there are a record 10.9 million jobs open. The rate at which unemployed people are getting jobs is lower than it was pre-pandemic, and it’s taking longer to hire people. Meanwhile, job seekers say employers are unresponsive.”

“Debt Ceiling Modest Proposal -- Perpetuities” (John Cochrane, The Grumpy Economist). “The Treasury computes the total amount of debt by its face or principal value, not its market value. If the Treasury issues a bond that pays $1 coupons each year for 10 years and then pays $100 at maturity, the treasury counts this as $100 additional debt. The Treasury ignores the coupon payments, and how much the bond actually sells for, i.e. how much the Treasury actually borrows, when the bond is auctioned. Now you see my answer: Perpetuities have coupons, but no principal…[t]oo clever? Maybe. OK, undoubtedly yes. But if economics lunchroom talk can consider trillion-dollar coins, we can talk about perpetuities. Or maybe a serious attempt to do this would bring US treasury accounting into the 1960s, with cutting-edge concepts like market values not face values, duration not average principal maturity, and interest cost concept that goes beyond coupons, so that the debt limit and treasury accounting is more economically meaningful.”

“Move fast And Bank Things: Crypto-Based ‘DeFi’ Takes On Wall Street” (Fortune). “As a largely unregulated part of the economy, DeFi has exploded in tandem with demand for cryptocurrencies like Bitcoin and Ethereum. Most of the action takes place on Ethereum, the second-biggest crypto network, whose blockchain comes with a built-in programming language, Solidity, that makes it easy to build so-called decentralized apps. For now, the ecosystem is populated primarily by people who range from comfortable with to rabidly passionate about crypto—with all its risk and legal uncertainty. “

“Who Owns Your Life Insurance Policy? It Might Be A Private-Equity Firm” (Wall Street Journal). “Americans own more than 160 million individual life insurance and annuity policies. A big, unexpected change is ahead for many of them. Traditional life insurers are leaving the business in droves. The responsibility for death benefits, which might be a half-century away, or for annuity income streams that run over decades, is increasingly in the hands of a new breed of insurance-company owner.”

Notable activist hedge fund’s recent returns not actually very good

Suppose you manage a pension fund on behalf of a big union and you want to reward members with at least at least market-average returns on their hard-earned savings. What’s one way to not achieve that goal? Apparently, allocate that capital Elliott Management, one of the most prominent, headline-grabbing, and (probably) expensive investment managers in the world (emphasis added):

Paul Singer’s Elliott Management has a fearsome reputation that has turned it into a $48 billion behemoth. But the hype surrounding the firm doesn’t match its results, according to a new report by the Communications Workers of America and the SOC Investment Group. The SOC Investment Group works with pension funds sponsored by unions affiliated with the Strategic Organizing Center, a coalition of four unions representing more than four million members with more than $250 billion in assets under management.

Not only is Elliott’s hedge fund an underperformer, so are the companies that its activism targets, the report claimed.

…

Whatever Singer’s standing among hedge fund honchos, the report noted that over the past several years, Elliott has underperformed both the S&P 500 and a 60-40 blend of stock and bond investments. As of March 31, over the prior 12 months Elliott gained 14.78 percent net of fees, while the S&P 500 gained 56.35 percent, and a 60-40 blend rose 31.67 percent, the report said.

“Elliott has not provided superior risk-adjusted returns and despite much marketing rhetoric, has yielded absolute returns inferior to conventional investments,” according to the report.

Over five years, it said the annualized performance of Elliott was 9.21 percent, compared with a 16.30 annualized gain for the S&P 500 and a 11.15 percent gain for the 60-40 blend.

What we’re reading (9/21)

“The Stock Market Is Afraid Again. Here's What That Means For Your Investments” (CNN Business). “It's been a wobbly week on Wall Street and CNN Business' Fear and Greed Index is flashing ‘Fear.’ The stock market is in a weird place. It has fallen in most of the trading sessions this month. The S&P 500 (SPX), which is the broadest measure of the US stock market, only has four higher closes this month, and one of those was more or less flat. Meanwhile, the Fear & Greed Index is sitting at 35, which signals fear.”

“How Evergrande Could Turn Into ‘China’s Lehman Brothers’” (Caixin). “For the past two months, hundreds of people have been gathering at the 43-floor [of] Zhuoyue Houhai Center in Shenzhen, where China Evergrande Group’s headquarters occupy 20 floors. They held banners demanding repayment of overdue loans and financial products. Police with riot shields had to be on site to keep things under control.” Per ZeroHedge: “at its core, [Evergrande] is just one giant shadow-banking black box whose time has finally run out.”

“SEC Is Investigating Activision Blizzard Over Workplace Practices, Disclosures” (Wall Street Journal). “Federal securities regulators have launched a wide-ranging investigation into Activision Blizzard Inc., including how the videogame-publishing giant handled employees’ allegations of sexual misconduct and workplace discrimination, according to people familiar with the investigation and documents viewed by The Wall Street Journal. The Securities and Exchange Commission has subpoenaed Activision, known for its Call of Duty, World of Warcraft and Candy Crush franchises, and several of its senior executives, including longtime Chief Executive Bobby Kotick, according to the people and documents.”

“The Trillion-Dollar Fantasy” (Institutional Investor). “As ESG investing has been accelerating, the planet has experienced the warmest two decades on record, Antarctica has been melting, U.S. income inequality has been gapping, and species have been disappearing at rates unseen for millennia. And the Dow Jones Industrial Average is hitting new highs and asset managers are collecting attractive fees to oversee a popular new investment category.”

“After Merkel” (The Economist). “Mrs Merkel has at times seemed more monarch than chancellor. She will leave office with sky-high approval ratings. Three of the four coalitions she led were ‘grand’ ones with the Social Democratic Party (spd), which suited her centrism but tranquilised politics. She has so dominated the centre that outright criticism of her has come to seem almost lèse-majesté. That has inspired a wave of free-speech martyrs on the conservative fringes, the closest Germany gets to a culture war. In Europe Mrs Merkel has been the indispensable leader. Beyond it, her stout defence of liberal values and her modest demeanour have been reassuring in an age of noisy populism and nationalist showmen.”

What we’re reading (9/20)

“Natural-Gas Prices Surge, And Winter Is Still Months Away” (Wall Street Journal). “It is supposed to be offseason for demand, and prices haven’t climbed so high since blizzards froze the Northeast in early 2014. Analysts say that it might not have to get that cold this winter for prices to reach heights unknown during the shale era, which transformed the U.S. from a gas importer to supplier to the world…[t]he number of rigs drilling for gas has been basically flat since spring despite much higher prices. When prices rose above $5 in 2014, there were more than three times as many rigs drilling gas wells as the 100 operating now, according to Baker Hughes Co.”

“How Did Investors End Up On the Other Side of This Trade?” (Institutional Investor). “The stock market selloff in early 2020 took with it a number of high-profile volatility-trading funds that were designed to do the opposite: provide a source of uncorrelated returns. Now Markov Processes International has produced new research indicating that at least one fund was behaving as though it was selling risky hedges, or insurance in simple terms, against a stock selloff to other market participants. That’s the opposite of many of the funds’ objectives, according to investors familiar with the funds. It’s unlikely that investors intended to be in the business of providing tail-risk hedges. But that may be exactly what they did[.]”

“Amazon Is Piling Ads Into Search Results And Top Consumer Brands Are Paying Up For Prominent Placement” (CNBC). “Search for ‘toothpaste’ on Amazon, and the top of the web page will show you a mix of popular brands like Colgate, Crest and Sensodyne. Try a separate search for ‘deodorant’ and you’ll first see products from Secret, Dove and Native. Look a little closer, though, and you’ll notice that those listings are advertisements with the “sponsored” label affixed to them. Amazon is generating hefty revenue from the top consumer brands because getting valuable placement on the biggest e-commerce site comes with a rising price tag.”

“You Can Kill Single-Family Zoning, But You Can’t Kill The Suburbs” (Slate). “ Symbolically, the passage of SB 9 is a huge deal in the national movement to break down the apartment bans that effectively segregate American cities and shows just how far the policy window has shifted in the past five years…[o]n the ground, however, the reality will not be instant housing abundance—or the destruction of the suburbs, for better or for worse. Zoning is a powerful obstacle to denser, more affordable development—but reforming zoning can only do so much.”

“Why Taxing Stock Buybacks Is the Wrong Fix For Executive Pay” (DealBook). “The system of public capital depends on corporations’ selling stock, but we do not require that companies sell stock. There is no public duty (except in regulated industries such as banking) to maintain any specific level of capital. Here’s one way to think about it: If it is not wrong for a corporation to sell $3 billion in stock, is it wrong for it to sell $4 billion and later buy back $1 billion? In the end, it is the same thing. Buybacks are simply a means, via the intermediary of investors, of reallocating capital from companies with a surplus to companies with a capital need. And too much capital can be just as harmful as too little, leading to a misallocation and a waste of social resources.”

What we’re reading (9/19)

“Don’t Lose Sight Of The Inflation Monster” (Washington Post). “Americans are sitting on trillions of dollars of savings they accrued during the pandemic…[i]t’s been so long since the United States has suffered from endemic inflation that most adults are unprepared for what it will do. Annual 5 percent inflation may seem low, but it’s not. Because each price rise is built on the previous one, a 5 percent annual rate means that prices would double every 14 years.”

“Inflation Challenges Stock-Market Underpinnings As Investors Look Ahead To Fed Meeting” (MarketWatch). “Investors worry inflationary pressures will spill into company earnings, possibly as soon as the third quarter, challenging the underpinnings of the “phenomenal” stock-market performance in the pandemic, explained [Jensen Investment Management CIO Eric] Schoenstein. He sees Jensen clients seeking to tilt toward higher quality stocks, as they want exposure to ‘resilient’ companies that can handle the risks of a rising cost environment.”

“Banks Strike Back, But Returns Remain Strong With Fintech” (Wall Street Journal). “Down the road, banks might have some tailwinds. Deposits will likely stay cheap for some time, even as interest rates start to tick higher and perhaps gum up capital markets. As credit costs creep back up to normal levels, losses might eat into net yields on loans, making it less attractive to share any economics with an outside partner. Yet at the same time, any technology partner that is able to demonstrate an ability to keep credit losses minimized could be even more valuable to banks and investors. And banks might stay hungry enough for loan growth that the costs of partnerships are justified.”

“U.S. Banking Lobby Groups Oppose Proposed Tax Reporting Law” (Reuters). “The largest U.S. banking lobby groups banded together on Friday to make another push to kill a proposed bank account reporting law being drawn up as part of the congressional reconciliation package.”

“Geriatric Millennials Have The Most Power In The Workforce Right Now” (Insider). “According to a recent analysis by the Harvard Business Review that looked at 9 million employee records from more than 4,000 companies, midcareer employees are driving the [Great Resignation]. Resignation rates are highest among 30- to 45-year-old employees, increasing on average by more than 20% over the past year…[t]he reasons for the resignations are plenty, per the HBR: Employers may be less inclined to hire less experienced workers, creating more demand for mid-level workers; this cohort may have postponed switching jobs until some of the dust settled from the pandemic's economic effects; and the pandemic has caused some to reevaluate what they want in both their job and in life.”

What we’re reading (9/18)

“Where Has All the Money Gone?” (Project Syndicate). “Amid all the talk of when and how to end or reverse quantitative easing (QE), one question is almost never discussed: Why have central banks’ massive doses of bond purchases in Europe and the United States since 2009 had so little effect on the general price level?…A plausible generalization is that increasing the quantity of money through QE gives a big temporary boost to the prices of housing and financial securities, thus greatly benefiting the holders of these assets. A small proportion of this increased wealth trickles through to the real economy, but most of it simply circulates within the financial system.”

“China Faces A Potential Lehman Moment. Wall Street Is Unfazed” (CNN Business). “The implosion of Lehman Brothers, 13 years ago this week, showed how the collapse of a single entity can send shockwaves around the world. Echoes from that event are resounding today as a massive property developer on the other side of the world teeters on the brink of default. The risk is that the collapse of Evergrande, a Chinese real estate company with a staggering $300 billion of debt outstanding, could set off a chain reaction that spreads overseas.”

“There And Back Again: The COVID Global Market Roundtrip In Map Form” (Vident Financial). “Last year, the world went through a sudden, terrifying pandemic which involved massive government shutdowns and one of sharpest economic contractions in history. Markets responded in kind. And then they made the long trip back home to something resembling normal.”

“Amid COVID Surge, States That Cut Benefits Still See No Hiring Boost” (Reuters). “The August slowdown in U.S. job creation hit harder in states that pulled the plug early on enhanced federal unemployment benefits, places where an intense summertime surge of coronavirus cases may have held back the hoped-for job growth.”

“BlackRock Fund Manager Says He’s Cut Gold Holdings To ‘Almost Zero.’ Here’s Why.” (MarketWatch). “Near term, he [BlackRock’s Global Allocation Fund Manager Russ Koesterich] said there are likely ‘better hedges against inflation in the equity market and rather than own an asset that doesn’t produce cash flow, we would rather hedge some of the near term upside with stocks that have pricing power.’”

What we’re reading (9/17)

“They're Ignoring That There's Too Little Money Now” (Real Clear Markets). “As Keynes had written more than a decade before, in the early twenties, the greatest monetary evil is this: the shortage of money and its deflation which quite vigorously savages labor most of all. The entire economy suffers, of course, but it is the unfortunate single worker who has no protection from these far-reaching and, from the worker’s perspective, incorporeal ills. Whenever money is too dear, the actual wealth of any nation is undercut because money rather than sustainable enterprise is prioritized. Heightened liquidity preferences reorient the very nature of business; risk taking, or animal spirits, diminish if not disappear near entirely.”

“The Housing Crisis Is The Top Concern For Urban Residents” (Vox). “Housing costs and homelessness in America’s cities are so bad that people in growing metro areas now appear more concerned about those issues than Covid-19, public safety, taxes, education, and jobs, according to a new poll by the Manhattan Institute and Echelon Insights. The poll surveyed 4,000 adults from August 11-20, sampling 200 people each in the ‘20 metropolitan areas with the largest numerical population growth from 2010-2019.’”

“Are 401(k)s Worth It?” (U.S. News & World Report). “401(k) plans typically come with a number of expenses which might include management fees and recordkeeping fees. ‘Plans are required to distribute fee disclosures annually,’ says Julian Schubach, vice president of wealth management at ODI Financial in Lynbrook, New York. Still, it can be difficult to find these communications. ‘Most participants have no idea what fees they are paying,’ Schubach says.”

“World Bank Cancels Flagship ‘Doing Business’ Report After Investigation” (Wall Street Journal). “The Doing Business report has been the subject of an external probe into the integrity of the report’s data. On Thursday, the bank released the results of that investigation, which concluded that senior bank leaders including Ms. Georgieva [current head of IMF; full disclosure: my former employer] were involved in pressuring economists to improve China’s 2018 ranking. At the time, she and others were attempting to persuade China to support a boost in the bank’s funding.”

“Bud Light hopes This Beer Is The Next Big Thing” (CNN Business). “Anheuser-Busch has announced the launch of Bud Light Next, the company's first-ever zero-carb beer. The beverage, which hits shelves in early 2022, comes as health-conscious customers have gravitated toward light beers in recent years — and beer in general is in the middle of a big resurgence.”

What we’re reading (9/16)

“The Housing Theory Of Everything” (Works In Progress). “Try listing every problem the Western world has at the moment. Along with Covid, you might include slow growth, climate change, poor health, financial instability, economic inequality, and falling fertility. These longer-term trends contribute to a sense of malaise that many of us feel about our societies. They may seem loosely related, but there is one big thing that makes them all worse. That thing is a shortage of housing: too few homes being built where people want to live. And if we fix those shortages, we will help to solve many of the other, seemingly unrelated problems that we face as well.”

“U.S. Housing Regulator Proposes Tweaks To Capital Rules For Fannie Mae, Freddie Mac” (Reuters). “The regulator overseeing housing giants Fannie Mae and Freddie Mac proposed on Wednesday changes to recently imposed capital and leverage requirements on the pair.”

“Stock Buybacks Beat Capital Spending For Many Big Companies” (Wall Street Journal). “Spending on share buybacks increased much faster than capital expenditures in the first half of the year, after pullbacks in both categories last year amid the pandemic, S&P said in response to a Wall Street Journal data request. Share repurchases at companies in the S&P 500 increased to $370.4 billion, up 29% from the first six months of 2020. Capital spending—which usually goes toward assets such as land, buildings and technology—rose to $337.17 billion, up 4.8% from the year-earlier period.”

“Citigroup, JPMorgan Expect Lower Third-Quarter Markets Revenue” (U.S. News & World Report). “Citigroup Inc expects third-quarter markets revenue to decline by a ‘low-to-mid teens’ percentage from a year earlier and JPMorgan Chase & Co expects a decrease of about 10%, according to executives of the two big banks. The lower revenues are a result of trading that has ‘normalized’ from exceptionally high levels last year, when the pandemic was in full force, the executives said on Tuesday at a virtual investor conference held by Barclays.”

“Hedge-Fund Billionaire Ray Dalio Says Regulators Will ‘Kill’ Bitcoin If It Gets Too Successful” (Insider). “Ray Dalio, founder of Bridgewater Associates, said on CNBC he foresees regulators taking control of bitcoin if there's mainstream success for the cryptocurrency. ‘I think at the end of the day if it's really successful...they will try to kill it. And I think they will kill it because they have ways of killing it,’ Dalio said on CNBC during the SALT conference in New York.”

What we’re reading (9/15)

“What’s Your Raise Really Worth? Inflation Has Something to Say About It.” (Wall Street Journal). “This should be the best of times for low-wage workers, as pandemic-induced labor shortages force employers to sharply raise pay. Yet for many, it doesn’t feel that way, because those same disruptions have pushed inflation to near its highest rate in over a decade.”

“What to Expect From Gary Gensler’s Testimony” (DealBook). “The S.E.C. chair Gary Gensler will testify before the Senate Banking Committee today, after five months on the job. Since his confirmation, his public statements have generated much debate, many headlines and more than a few market movements. This morning, based on his prepared remarks, he’ll make the case for additional resources to achieve a more expansive agenda than many of his predecessors at the commission.”

“America Is Substantially Reducing Poverty Among Children” (The Economist). “It seemed like a blustery overpromise when President Joe Biden pledged in July to oversee, “the largest ever one-year decrease in child poverty in the history of the United States”. By the end of the year, however, he will probably turn out to have been correct. Recent modelling by scholars at Columbia University estimates that in July child poverty was 41% lower than normal.”

“Hedge Fund Activist Jeff Ubben Asks SEC To Mandate Carbon Pricing Disclosures” (Institutional Investor). “Jeff Ubben, the activist hedge fund manager who founded Inclusive Capital Partners a little more than a year ago, is calling for the Securities and Exchange Commission to make companies include a price for carbon as part of their climate-related ESG disclosures. Ubben, who is also a board member of ExxonMobil, made his comments in a September 8 letter to the SEC. It was one of thousands sent since SEC Commissioner Allison Herren Lee earlier this year asked for public comments regarding upgrades to the SEC’s climate change disclosures.”

“Does The Market Care About Ethical Investment? It Depends” (The Hill). “Corporate ESG actions can be voluntary or involuntary, and this distinction is important in understanding the true impact of ESG on company value. But new government mandates to pursue ESG goals are likely to prove costly to American shareholders and workers.”

Is a stock market “correction” coming?

I don’t spend a lot of time talking about asset allocation on this blog, because this blog is focused on equities. For the moment, this blog is mostly agnostic about other asset classes and when and how people move money among them. A priori, I don’t think most people are very good at timing the market (including me!)—and, why would they be, since no one can predict the future very well, much less predict it better than everyone else they are competing with in capital markets, which is what you need to be able to do to be very, very good at that sort of thing.

With that said, a lot of people think U.S. stocks are due for a big correction:

Here is what Jim Cramer has to say: “September is the cruelest month, and it’s playing out that way once again, with rolling corrections all over the place”;

And here is CNN: “After notching heady gains this year, US stocks could be in for a back-to-school reality check. What's happening: The S&P 500 has been in the red for five consecutive trading sessions, its longest losing streak since February”;

Here is Reuters: “Investors are girding their portfolios for potential stock market volatility, even as equities hover near fresh highs after logging seven straight months of gains”;

And here is Yahoo! Finance: “Don't let the hardcore bulls tell you otherwise, the proof is in the pudding (large companies' warnings).”

They aren’t alone: equity analysts at BofA, Deutsche, Morgan Stanley, and others have all said as much in recent weeks.

“Correction” is a word the business press and equity research analysts throw around casually, but it is in fact a very specific word and a very controversial word in this context. “Correction” does not mean “returns are likely to be modest” or “things are getting riskier and volatility is likely to be higher”. Forecasting a “correction” means you have high conviction in a material decline in stock prices. It means your expected return is significantly negative over some relevant period in the future, and that negative return is likely to manifest in a sudden and sharp (rather than gradual) drop-off in valuations. It means that you think prices are not just higher than they have been in the past, but higher than they should be (i.e., higher than intrinsic values). And it means that you think prices are systematically—that is, across the market—higher than they should be.

“Correction” is kind of a euphemism for a belief that all of those very strong assumptions are simultaneously true, and true right now at that. The finance media doesn’t usually get into all of that (equity analysts tend to be a little more specific, but just barely). And the arguments they do offer tend to be specious. Consider the sampling above:

Theoreticians have been looking for a basis to justify Cramer’s belief that summer/early fall is a bad time for asset prices for quite literally 400 years and still haven’t found any (see my post on the so-called “Halloween anomaly”). I guess he gets points for observing that, empirically, results this time of year have tended not to be great, but only in the same way that Ptolemy gets points for his observations about the cosmos despite ultimately being completely wrong about the underlying structure governing his observations. The latter is what makes predictions reliable.

CNN’s claim about “five consecutive trading sessions” being “in the red” is meaningless in light of the fact that stock prices follow a random walk (past price paths don’t—or at least shouldn’t—have any bearing on future price paths).

Reuter’s suggestion that investors are nervous because stock prices keep hitting highs doesn’t make a lot of sense in light of the fact that the stock market has a positive average expected return (due to inflation, the time value of money, compensation for risk, etc.). Given that, stocks should be hitting new highs all the time without it signaling imminent peril. This concern is weirdly recited all the time, probably because it has some surface-level intuitive appeal.

Yahoo! Finance’s reasoning is the most compelling to me: companies’ management may have private info that you and I and the market don’t know about, so their warnings could be prescient. BUT the market has heard their warnings and the supposed correction hasn’t manifested despite them. Is there some reason I, specifically, should interpret their warnings as meaning stock prices are dropping 10% ASAP when thousands (millions?) of other U.S. stock market participants are yawning at them?

At the end of the day, if you believe a correction is coming, you need to believe not only that cash flows are going to soften or risk levels will increase, but further than cash flows are going to soften more or faster than the market already believes and/or that risk is increasing more or faster than the market already believes.

Whatever we are in for, “correction” probably isn’t the right word for it. Cash flows may soften more or faster than expected and/or risk might rise more or faster than expected, but if we already knew about it, the correction would already be here. Alas, it is not.

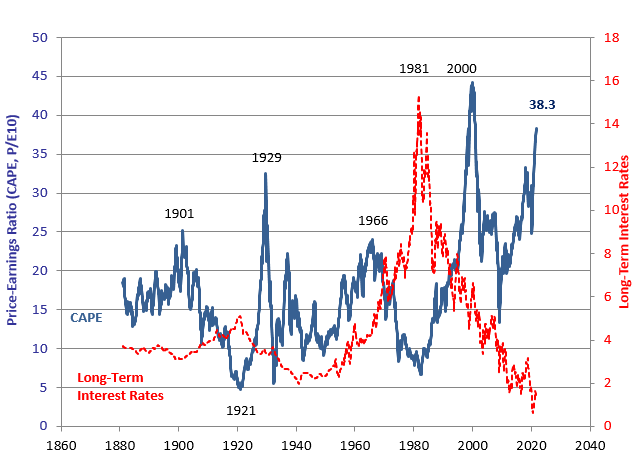

Among the cautious observers, the more sophisticated ones are probably thinking a lot about the following chart, from Nobel Laureate Robert Shiller’s website. The chart shows the price-to-earnings ratio for the stock market as a whole, where earnings are normalized by taking a simple average over the trailing 10-year period (adjusted for inflation). Earnings and prices should be linked—since prices at any moment in time should just be the capitalized value of the future earnings stream—such that the P/E ratio should mean-revert. As the chart makes clear, the ratio is high right now. For it to revert back to the long-term average, expected earnings need to rise faster than prices or, equivalently, prices need to fall faster that expected earnings. So far this year, the story has been that high expected growth in earnings would justify the high level of prices such that the prices at current levels (or higher) could be sustained with the ratio still mean-reverting. But now there is concern that real earnings growth might not be as robust as previously expected in light of the delta variant (and other emerging coronavirus variants), higher-than-expected inflation, etc. If these concerns manifest in reality, price appreciation should be lower than in recent periods.

Shiller Cyclically Adjusted Price-To-Earnings

It’s worth keeping in mind, though, that even if that story is right, it doesn’t necessarily imply some sort of dramatic, sudden double-digit depreciation in prices the likes of which the media and equity analysts are forecasting now. Another chart from Shiller makes that point clear. The chart first converts the P/E ratio described above to an implied annualized yield (higher current P/E ratio implies lower yield, lower current P/E ratio implies higher yield, all else equal). Then, the chart compares that yield to subsequent average annual stock market returns over the next 10 years. The chart is pretty clear that lower current P/E-implied yields (i.e., higher P/E ratios) correlate to lower-than-average subsequent returns.

But—and here’s the key point—high P/E ratios don’t imply sudden, shockingly catatonic returns. Just lower-than-average returns. Specifically, if you regress the subsequent returns on current P/E-implied yield, what you’ll find is that the data since 1871 implied annualized average real returns of about 3.5% percent. And that’s an average across the distribution of the entire market. That allows plenty of room for finding good opportunities without sitting in cash.

No doubt, things could change and the big decline folks have in mind could happen; but it is not likely it would occur based on things we know now. And the things we don’t know now are pretty tough to predict.

Shiller Cyclically Adjusted Price-to-Earnings Yield and Subsequent Annualized 10-Year Excess Returns

What we’re reading (9/14)

“Democrats Release Details Of Proposed Tax Increase” (Wall Street Journal). “House Democrats spelled out their proposed tax increases on Monday, pushing higher rates on corporations, investors and high-income business owners as they try to piece together enough votes for legislation to expand the social safety net and combat climate change. The plan would increase the top corporate tax rate to 26.5% from 21%, impose a 3-percentage-point surtax on people making over $5 million and raise capital-gains taxes—but without the changes to taxation at death sought by the Biden administration.”

“Harvard Says It Will Not Invest In Fossil Fuels” (New York Times). “The announcement, sent out on Thursday, is a major victory for the climate change movement, given Harvard’s $42 billion endowment and prestigious reputation, and a striking change in tone for the school, which has resisted putting its full weight behind such a declaration during years of lobbying by student, faculty and alumni activists.”

“Meritocracy's Cost” (Charles Murray in the Claremont Review of Books). “As Young predicted, far too many members of today’s elites really do believe that they deserve their place in the world. They have gotten too big for their britches. They are unseemly, albeit in different ways. The billionaire’s 30,000-square-foot home is visibly unseemly. But so is a faculty lounge of academics making snide remarks about rednecks—meaning the people without whom the academics would have no working mechanical transportation, be in the dark after sundown, have to use chamber pots, and, literally, starve. Today’s elites have a remarkable obliviousness about the lives and contributions of ordinary people that bespeaks an unseemly indifference—not to mention disdain—for those people.”

“Pandemics Initially Spread Among People Of Higher (Not Lower) Social Status: Evidence From COVID-19 And The Spanish Flu” (Social Psychological and Personality Science). “According to a staple in the social sciences, pandemics particularly spread among people of lower social status. Challenging this staple, we hypothesize that it holds true in later phases of pandemics only. In the initial phases, by contrast, people of higher social status should be at the center of the spread. We tested our phase-sensitive hypothesis in two studies. In Study 1, we analyzed region-level COVID-19 infection data from 3,132 U.S. regions, 299 English regions, and 400 German regions. In Study 2, we analyzed historical data from 1,159,920 U.S. residents who witnessed the 1918/1919 Spanish Flu pandemic. For both pandemics, we found that the virus initially spread more rapidly among people of higher social status. In later phases, that effect reversed; people of lower social status were most exposed. Our results provide novel insights into the center of the spread during the critical initial phases of pandemics.”

“9,000 Years Ago, Funerals In China Involved A Lot Of Beer” (Ars Technica). “At a 9,000-year-old burial site in China called Qiaotou, archaeologists recently unearthed a number of ceramic vessels. Some of the vessels were shaped like the long-necked, round-bellied bronze pots that people used for alcoholic drinks millennia later. And that made Dartmouth College anthropologist Jiajing Wang and his colleagues wonder whether these earlier clay versions might have once held beer, too. Bits of the residue left inside eight of the 13 pots turned out to contain phytoliths (fossilized plant remains) from rice, tubers, and a plant called Job’s tears. Starch molecules in the residue showed signs of being heated and fermented. Wang and his colleagues also found yeast and mold, key ingredients in fermentation.”

What we’re reading (9/13)

“U.S. Stock Market Faces Risk Of Bumpy Autumn, Wall Street Analysts Warn” (Wall Street Journal). “Analysts at firms including Morgan Stanley, Citigroup Inc., Deutsche Bank AG and Bank of America Corp. published notes this month cautioning about current risks in the U.S. equity market…[S]everal analysts said that they believe there is a growing possibility of a pullback or, at the least, flatter returns. Behind that cautious outlook, the researchers said, is a combination of things, including euphoric investment sentiment, extended valuations and anticipation that inflation and supply-chain disruptions will weigh on corporate margins.”

“Stocks Look Dangerously Overvalued And Are At Risk Of A Sharp Correction As Investors Misjudge The Sustainability Of Explosive Earnings Growth, DB Says” (Insider). “US stocks are priced for perfection following a robust year of post-pandemic earnings growth, but high valuations suggest a sharp market sell-off could be imminent, according to a Thursday note from Deutsche Bank. On nearly every valuation metric, US stocks are trading at "historically extreme" levels, according to the bank. Trailing and forward price to earnings, enterprise value to EBITDA, and cash flow valuation metrics are well into the 90th percentile, Deutsche Bank highlighted.”

“The Stock Market Fails A Breathalyzer” (Wall Street Journal). “Joby Aviation, which plans to begin an electric air taxi service in 2024, is worth more than Lufthansa, EasyJet or JetBlue. Does that seem right? In this market, why not? Heck, earlier this year, Tesla was worth more than the next nine car manufacturers combined, though now only the next six. Beyond Meat, made with pea protein, is worth more than the entire market for peas eaten globally—like the bumper sticker says: Imagine whirled peas. Do fundamentals even matter? I can go on. Used-car sales platform Carvana is worth more than Volvo, Honda, Ford or Hyundai. Airbnb is worth more than Marriott and Hilton combined. Crypto-exchange Coinbase is worth more than the Nasdaq.”

“A Perfect Storm For Container Shipping” (The Economist). “A giant ship wedged across the Suez canal, record-breaking shipping rates, armadas of vessels waiting outside ports, covid-induced shutdowns: the business of container shipping has rarely been as dramatic as it has in 2021. The average cost of shipping a standard large container (a 40-foot-equivalent unit, or FEU) has surpassed $10,000, some four times higher than a year ago…[t]he spot price for sending such a box from Shanghai to New York, which in 2019 would have been around $2,500, is now close to $15,000. Securing a late booking on the busiest route, from China to the west coast of America, could cost $20,000.”

“What Did Institutions Really Do?” (Economic History Research). “Landowners [in 18th/19th century Britain] remained the paramount faction in national politics and, until the end of the nineteenth century, they were the economic winners of industrialization. Already buoyed by rising land values around coal and water power sites, they continued to extract significant rents from their legislative dominance. As tax receipts accelerated—five times faster than national product—during the eighteenth century, the land tax barely changed. The aristocracy passed on the costs of fighting Britain’s wars to the commercial middle class through the excise and customs, the extraction of which was aided by a quadrupling in the size of the fiscal bureaucracy.”