What we’re reading (12/4)

“Don’t Put Your Eggs in One Basket. That Investing Principle Still Holds.” (New York Times). “There’s no shortage of reports from asset management firms arguing that hedge funds and private equity funds need to be added into the intelligent investor’s mix. And you can also delve into futures and options that can limit your losses, at a cost. Once you’ve started down this route, why not go further afield? Cryptocurrency: People in the industry claim that it’s an asset class and should be represented in your portfolio. I’ve not seen solid evidence that any of these things are needed as core investments.”

“Who Got A Lot Richer And Who Didn’t During The Pandemic” (Wall Street Journal). “The pandemic made Americans richer across every racial, ethnic and income group—though not equally. Home values shot up, and with fewer opportunities to spend money during lockdowns, many people paid down debt and boosted savings. Between 2019 and 2021, the median household’s net worth increased 30% to $166,900, according to a report out Monday from Pew Research Center.”

“Unknown Traders Appear To Have Anticipated October 7 Hamas Attack, Research Finds” (CNN Business). “Bets against the value of Israeli companies spiked in the days before the October 7th Hamas attacks, suggesting some traders may have had advance knowledge of the looming terror attack and profited off it, according to new research released Monday…Those bets against the value of the MSCI Israel Exchange Traded Fund (ETF) in the days before the October 7 attack ‘far exceeded’ the short selling activity that took place during the Covid-19 pandemic, the 2014 Israel-Gaza war and the 2008 global financial crisis, the paper finds.”

“Bill Gates: How I Invest My Money In A Warming World” (New York Times). “We’re not doomed, nor do we have all the solutions. What we do have is human ingenuity, our greatest asset. But to overcome climate change, we need rich individuals, companies and countries to step up to ensure green technologies are affordable for everyone, everywhere — including less wealthy countries that are large emitters, like China, India and Brazil.”

“William Rehnquist Proposed To Sandra Day O’Connor. She Said No.” (Washington Post). “Decades before they would serve together on the Supreme Court, William Rehnquist and Sandra Day O’Connor were engaged in a different type of courtship. The two grew close while attending Stanford Law School — they regularly shared notes and eventually became a couple. Although Sandra Day, as she was known then, eventually broke up with Rehnquist and married a different Stanford Law classmate, John O’Connor, an author revealed to NPR in 2018 that she first turned down a marriage proposal from Rehnquist, the future chief justice, in the early 1950s.”

What we’re reading (12/3)

“Will High Interest Rates Trigger A Debt Disaster?” (Project Syndicate). “Deficits and high debt-to-GDP ratios are not the problem. What matters is the difference between the interest rate and the growth rate. For many years, the US Congressional Budget Office has regularly projected that high interest rates and low growth rates would lead to a debt explosion. But those projections were always wrong – until the US Federal Reserve started jacking up interest rates last year.”

“Momentum Investing Has Struggled For 20 Years. Here’s Why” (Wall Street Journal). “From 1940 through mid-2002, a portfolio rebalanced monthly owning the 10% of stocks with the greatest trailing-year returns, while simultaneously shorting the 10% of stocks with the trailing year’s worst returns, appreciated at an annualized pace of 17.4%, before transaction costs. Since then, this portfolio has declined at a 3.6% annualized pace. In contrast, the trend of the overall stock market remained steady throughout both periods: 11.4% annualized appreciation before mid-2002 and 10.4% thereafter. What changed? A new study attributes the shift primarily to Morningstar in mid-2002 changing the methodology for its mutual-fund star-rating system.”

“There Really Was A Corporate Conspiracy To Inflate Egg Prices, And It's Been Proven In Federal Court” (Dealbreaker). “Some precedent now indicates that nefarious corporate scheming may indeed be possible within the U.S. egg market. On November 21, 2023, a federal jury in the Northern District of Illinois delivered its verdict finding that the two largest domestic egg producers, Cal-Maine Foods Inc. and Rose Acre Farms Inc., together with two egg-industry trade groups, conspired to reduce supply in order to artificially drive up the price of eggs.”

“Hundreds Of Stocks Have Fallen Below $1. They’re Still Listed On Nasdaq.” (Wall Street Journal). “As of Friday, 557 stocks listed on U.S. exchanges were trading below $1 a share, up from fewer than a dozen in early 2021, according to Dow Jones Market Data. The majority of these stocks—464 of them—are listed on the Nasdaq Stock Market, whose rules require companies to maintain a minimum share price of $1 or risk being delisted.”

“Gold Bars And Tokyo Apartments: How Money Is Flowing Out Of China.” (New York Times). “The outbound shift of money in part indicates unease inside China about the sputtering recovery after the pandemic as well as deeper problems, like an alarming slowdown in real estate, the main storehouse of wealth for families. For some people, it is also a reaction to fears about the direction of the economy under China’s leader, Xi Jinping, who has cracked down on business and strengthened the government’s hand in many aspects of society.”

November performance update

Hi friends, here with a monthly performance update for November:

Prime: +5.25%

Select: +8.22%

SPY ETF: +8.87%

Bogleheads Portfolio (80% VTI + 20% BND): +8.25%

Under typical circumstances I would be overjoyed about a 5.25 percent monthly return (~85 percent when annualized) for SPC’s flagship strategy and a 8.22 percent return for the “B-team” Select strategy. Of course, November was explosive for the market as a whole, with SPY up 8.87 percent, besting its average annual return historically. The macroeconomic backdrop would seem to have been unusually supportive of the value of corporate assets , with a consensus emerging this month that a so-called “soft-landing” (deceleration in consumer prices without a recession) is on offer.

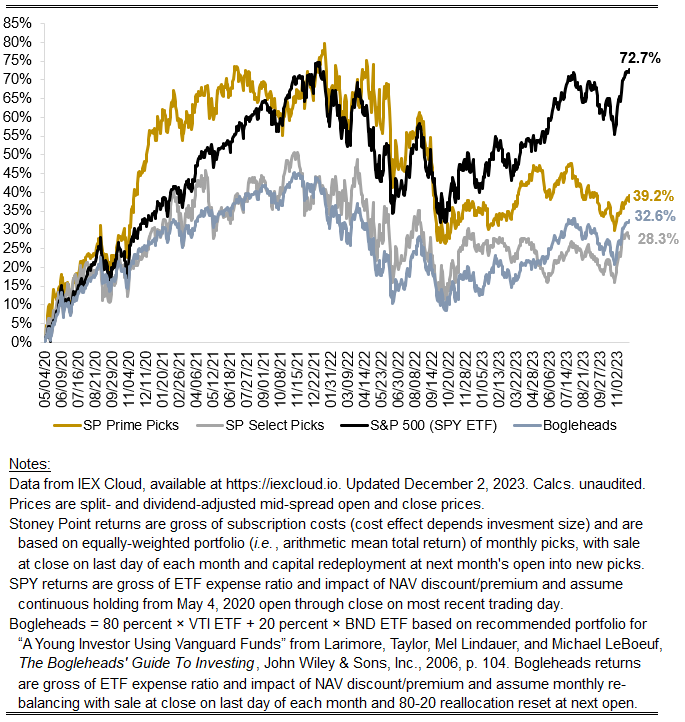

It’s worth dwelling on the picture below for a moment, which starts early in the pandemic and tells quite a story. There was a sharp rise in equity values concurrent with policy measures that rendered money unusually cheap (lowering hurdle rates and raising NPVs, in the case of monetary policy; raising profit expectations and thus raising NVPs, in the case of fiscal policy). This effect was not unique to corporate equities, of course — residential real estate equity investments experienced the same lift, for example, as did many other assets/products. Price appreciation across the economy is, by definition, inflation of the sort that concerns central bankers, warranting the reverse policy response (higher rates, lower NPVs) which is the story of 2022 in the chart. But here we are in 2023 and, despite more fits and starts, the trend kind of parrallels 2020/2021 (for the market overall), which is just kind of extraordinary! Consider what the 72.7 percent for the SPY ETF implies: the capital stock of the S&P 500 is worth nearly twice as much in aggregate as it was in May of 2020, three and a half years ago. That rate of appreciation dwarfs the base rate one would extrapolate from the history of that index dating back to the 20s, and probably similar composite indices that date back to the 19th century. I expect — but haven’t checked — that it dwarfs the rate of return on a hypothetical index one might construct that includes stocks all the way back to the 1700s and 1600s (e.g., V.o.C., B.o.E., etc.).

The comparison of the black line to the others also tells a story: compared to S&P 500, the Stoney Point strategies heavily weight indicia that characterize “value stocks” (low market values relative to fundamental/theoretical drivers of value). This is by design, though the market has rewarded it comparably less lately. The Bogleheads portfolio also differs from the SPY ETF in ways that are important for understanding the chart. Notably, the Vanguard VTI ETF (which gets 80 percent in the portfolio), tracks the CRSP US Total Market index, which reflects the performance of a much wider cross section of U.S. equities than the S&P 500, including mid- and small-cap companies. Smaller equities have also been rewarded less lately, particularly in 2022. But there are reasons to think that is changing alongside the emerging consensus about a soft landing: in November, the most widely followed U.S. small-cap index, the Russell 2000, was up nearly 12.5 percent, that is to say roughly a third better than the S&P 500.

One footnote I would be remiss not to mention: I’ve incorporated a few additional value indicators into the SPC model starting with December’s picks. Some of these are novel, some less so; the philosophy behind including them is to gain precision in identifying “value” stocks. The denominator for all of these “value” ratios is the same: current price. Realized returns are tautologically equal to End Price / Current Price - 1, so value ratios equal to x / Current Price (where x is some fundamental determinant of value) are all different ways of extracting information about the overall market’s expectation for future returns. Where value-oriented investors often disagree is what the best “x” is.

Stoney Point Total Performance History

December picks available now

The new Prime and Select picks for December are available starting now, based on a model run put through today (November 30). As a note, I will be measuring the performance on these picks from the first trading day of the month, Friday, December 1, 2023 (at the mid-spread open price) through the last trading day of the month, Friday, December 29, 2023 (at the mid-spread closing price).

What we’re reading (11/30)

“Cigna, Humana In Talks For Blockbuster Merger” (Wall Street Journal). “The companies are discussing a stock-and-cash deal that could be finalized by the end of the year, assuming the talks don’t fall apart, according to people familiar with the matter.”

“Carlyle GrouAand WP Carey Set To Join S&P MidCap 400; Others To Join S&P SmallCap 600” (PR Newswire). “S&P Dow Jones Indices will make the following changes to the S&P MidCap 400 and S&P SmallCap 600 effective prior to the open of trading on Thursday, November 30: Carlyle Group Inc. (NASD: CG) will replace ICU Medical Inc. (NASD: ICUI) in the S&P MidCap 400…WP Carey Inc. (NYSE: WPC) will replace Worthington Industries Inc. (NYSE: WOR) in the S&P MidCap 400. Worthington Industries will replace Avantax, Inc. (NASD: AVTA) in the S&P SmallCap 600.”

“Charlie Munger’s Life Was About Way More Than Money” (Wall Street Journal). “It’s 1931, and a boy and girl, both about seven years old, are playing on a swing set on N. 41st St. in Omaha. A stray dog appears and, without warning, charges. The children try to fight the dog off. Somehow, the boy is unscathed, but the dog bites the girl. She contracts rabies and, not long after, dies. The boy lives. His name? Charles Thomas Munger. Charlie Munger, the brilliant investing billionaire who died on Tuesday in a California hospital 34 days before his 100th birthday, told me that story when I interviewed him last month. I’d asked the vice chairman of Warren Buffett’s Berkshire Hathaway: What do you think of people who attribute their success solely to their own brilliance and hard work? ‘I think that’s nonsense,’ Munger snapped, then told his story, which I can’t recall him ever publicly recounting. ‘That damn dog wasn’t 3 inches from me,” he said. “All my life I’ve wondered: Why did it bite her instead of me? It was sheer luck that I lived and she died.’ He added: ‘The records of people and companies that are outliers are always a mix of a reasonable amount of intelligence, hard work and a lot of luck.’”

“Hedge Fund Dollar Bulls Hold Fast Even As US Currency Erases Gains” (Bloomberg). “Hedge funds piled into bullish dollar bets this month despite the currency’s slide on softening US economic data and increasing expectations that the Federal Reserve’s most aggressive rate-hiking cycle in a generation is near an end.”

“Perhaps Intergenerational Mobility Has Not Declined In The United States After All” (Marginal Revolution). “From the latest American Economic Review: ‘A large body of evidence finds that relative mobility in the US has declined over the past 150 years. However, long-run mobility estimates are usually based on White samples and therefore do not account for the limited opportunities available for nonwhite families. Moreover, historical data measure the father’s status with error, which biases estimates toward greater mobility. Using linked census data from 1850 to 1940, I show that accounting for race and measurement error can double estimates of intergenerational persistence. Updated estimates imply that there is greater equality of opportunity today than in the past, mostly because opportunity was never that equal.’ That is from Zachary Ward of Baylor University. If that is true, and it may be, how many popular economics books from the last twenty years need to be tossed out? How many ‘intergenerational mobility is declining’ newspaper columns and magazine articles? Ouch. No single article settles a question, but for now this seems to be the best, most up to date word on the matter.”

What we’re reading (11/28)

“Charlie Munger, Who Helped Buffett Build Berkshire, Dies At 99” (Bloomberg). “Charles Munger, the alter ego, sidekick and foil to Warren Buffett for almost 60 years as they transformed Berkshire Hathaway Inc. from a failing textile maker into an empire, has died. He was 99.”

“Pressure Mounts On Private Equity-Backed Company Finance Chiefs As Market Shifts” (Wall Street Journal). “Private-equity firms have turned to smaller, tuck-in acquisitions to expand the companies they back as debt remains expensive and valuations for many larger businesses remain elevated. But some company CFOs are so used to focusing on managing day-to-day operations that they struggle to adapt to a sponsor’s more expansive objectives, according to Neely, who worked at several other private equity-backed companies before joining Specialty1. ‘[CFOs may think] I don’t even have my house in order yet and you want me to go look at this other house that you potentially want to buy?’ he said.”

“The Pension: That Rare Retirement Benefit Gets A Fresh Look” (New York Times). “Only about one in 10 Americans working in the private sector today participates in a defined-benefit pension plan, while roughly half contribute to 401(k)-type, defined-contribution plans, which are funded with their pretax dollars and, in many cases, employer contributions.”

“Home Prices Kept Rising Even As Mortgage Rates Surged, S&P Case-Shiller Says” (CNBC). “Nationally, prices were 3.9% higher in September compared with the same month a year earlier, up from a 2.5% annual gain in August, according to the S&P CoreLogic Case-Shiller Index. This occurred as the average rate on the 30-year fixed mortgage climbed toward 8%.”

“Shein’s Big I.P.O. Test” (DealBook). “The company and its underwriters are betting that investors will be more receptive to I.P.O.s, even though high-profile market debuts this fall largely fizzled out. Shein is also testing whether it can endure what’s likely to be an increase in political heat on the China-founded e-commerce giant.”

What we’re reading (11/27)

“Investors See Interest-Rate Cuts Coming Soon, Recession Or Not” (Wall Street Journal). “Wall Street is gearing up for rate cuts. Twenty months after the Federal Reserve began a historic campaign against inflation, investors now believe there is a much greater chance that the central bank will cut rates in just four months than raise them again in the foreseeable future. Interest-rate futures indicated Monday a 52% chance the Fed will lower rates by at least a quarter-of-a-percentage point by its May 2024 policy meeting, up from 29% at the end of October, according to CME Group data. The same data pointed to four cuts by the end of the year.”

“E-Commerce Stocks Rally After Black Friday Shoppers Spend Record Online” (CNBC). “Black Friday online spending reached a record $9.8 billion in the U.S., up 7.5% from a year earlier, according to Adobe Analytics. Online sales on Cyber Weekend, the days between Black Friday and Cyber Monday, surged 7.7% to $10.3 billion. Cyber Monday sales are expected to reach up to $12.4 billion, making it the biggest U.S. online shopping day of the year, according to Adobe.”

“Deutsche Bank Makes The Highest S&P 500 Forecast On Wall Street — And Says That May Be Too Conservative” (Morningstar). “A team led by Bankim Chadha, the chief U.S. equity & global strategist, said the S&P 500 SPX has seen solid earnings this year, but ‘perceptions’ remain lackluster, due to still low year-over-year earnings per share (EPS) growth and corporate uncertainty over the macroeconomic outlook. They say that could change in the fourth quarter when year-over-year earnings growth is expected to near 10%.”

“How This First-Time Founder Became A Chicken Tender Billionaire” (Inc.). “When Todd Graves first pitched the idea for Raising Cane's as a college student back in 1994, his Louisiana State University professor hated the concept. A fast-food restaurant that sold only chicken fingers went completely against industry norms. At that time, the sector was focused on adding more variety and healthy items to menus. The professor told Graves that he had not done enough research and gave his hypothetical business plan the lowest grade in the class, a B-. In reality, however, Graves had done plenty of research. ‘I'd basically written the Bible on a chicken finger restaurant. I even knew what our aprons would cost,’ recalls Graves, who spoke to Inc.”

“How Whitney Wolfe Herd’s Fateful Deal With A Russian Mogul Deprived Early Bumble Employees Of A Stock Windfall When She Became A Billionaire” (Business Insider). “For early Bumble employees…the company's unorthodox approach to equity, including selective use of an obscure form of compensation referred to internally as ‘shadow equity,’ remains a perplexing and bitter memory that is difficult to reconcile with Bumble's positive accomplishments and oft-repeated maxim — ‘Bee Kind.’”

December picks available soon

I’ll be publishing the Prime and Select picks for the month of December before Friday, December 1 (the first trading day of the month). As always, SPC’s performance measurement for the month of November, as well as SPC’s cumulative performance, will assume the sale of the November picks at the closing price (at the mid-point of the closing bid and ask prices) on the last trading day of the month (Thursday, November 30). Performance tracking for the month of December will assume the December picks are bought at the open price (at the mid-point of the opening bid and ask prices) on the first trading day of the month (Friday, December 1).

What we’re reading (11/25)

“Black Friday Shoppers Spent A Record $9.8 Billion In U.S. Online Sales, Up 7.5% From Last Year” (CNBC). “Black Friday e-commerce spending popped 7.5% from a year earlier, reaching a record $9.8 billion in the U.S., according to an Adobe Analytics report, a further indication that price-conscious consumers want to spend on the best deals and are hunting for those deals online.”

“Home Prices Are Tumbling In These 25 Cities, Giving Hope To Buyers While Costing Owners Who Bought At The Peak Up To $223 Per Day” (Business Insider). “Property values are starting to slide across the nation — for better or worse. Houses are cheaper than they were last year in 25 of the 100 biggest US real estate markets, according to a November 20 report from real estate research site Point2.”

“Struggling Cities Face More Pain From AI Boom” (Tyler Cowen in Bloomberg). “Artificial intelligence is likely to transform our world in many ways, but one that hasn’t received much attention is the technology’s looming impact on real estate. As AI becomes an essential component of both business and daily life, the value of places where those who work on AI want to live will rise, provided these locales have reasonable infrastructure. At the same time, the value of lower-tier cities left out of the AI boom will diminish.”

“Tesla Vs. Toyota Is The New Hot Battle In Cars” (Wall Street Journal). “When Toyota began spreading its hybrid technology to vehicles beyond the Prius, it came at a hefty premium. In 2005, for example, Toyota’s Highlander hybrid cost almost $10,000 more than the base version of the sport-utility vehicle and was engineered to maximize efficiency at the expense of performance. Or, put another way, customers paid more for some noticeable compromises. Today, that’s changed. Toyota hasn’t said what the new Camry will cost, but the current hybrid version starts at a little less than $2,500 more than the base version of the sedan. And Toyota is touting the new hybrid will have more horsepower than the current base version.”

“Pro Dollarization” (John Cochrane). “With President Milei's election in Argentina, dollarization is suddenly on the table. I'm for it. Here's why…Start with "why not?'' Dollarization, not a national currency, is actually a sensible default. The dollar is the US standard of value. We measure length in feet, weight in pounds, and the value of goods in dollars. Why should different countries use different measures of value? Wouldn't it make sense to use a common standard of value? Once upon a time every country, and often every city, had its own weights and measures. That made trade difficult, so we eventually converged on international weights and measures. (Feet and pounds are actually a US anachronism since everyone else uses meters and kilograms. Clearly if we had to start over we'd use SI units, as science and engineering already do.) Moreover, nobody thinks it's a good idea to periodically shorten the meter in order to stimulate the economy, say by making the sale of cloth more profitable. As soon as people figure out they need to buy more cloth to make the same jeans, the profit goes away.”

What we’re reading (11/24)

“Mortgage Rates Fall For Fourth Week But Stay Above 7%” (CNN Business). “The 30-year fixed-rate mortgage fell to an average of 7.29% in the shortened week ending November 22, according to data from Freddie Mac released on Wednesday, a day earlier than normal due to the Thanksgiving holiday. That was down from 7.44% the week before. A year ago, the 30-year fixed-rate was 6.58%.”

“Voters See American Dream Slipping Out Of Reach, WSJ/NORC Poll Shows” (Wall Street Journal). “Only 36% of voters in a new Wall Street Journal/NORC survey said the American dream still holds true, substantially fewer than the 53% who said so in 2012 and 48% in 2016 in similar surveys of adults by another pollster. When a Wall Street Journal poll last year asked whether people who work hard were likely to get ahead in this country, some 68% said yes—nearly twice the share as in the new poll.”

“The Fight For The Soul Of A.I.” (New York Times). “As impressive as they all were [OpenAi employees], I remember telling myself: This isn’t going to last. I thought there was too much money floating around. These people may be earnest researchers, but whether they know it or not, they are still in a race to put out products, generate revenue and be first.”

“A Common, Illegal Tactic Retailers Use To Lure Consumers” (Washington Post). “It’s not hard to find a deal right now; the challenge is knowing whether it’s real. Retailers go into overdrive during the holiday season, flooding inboxes with roaring Black Friday discounts. But many markdowns are not what they seem, industry experts warn. Some sales for 30, 40 and 50 percent off are simply rollbacks, returning prices to their starting points — behavior that has gotten some retailers in legal trouble for violating consumer guidelines.”

“Rising Corporate Bankruptcies And Debt Defaults Are Another Headwind For The Economy, Experts Warn” (Business Insider). “There's a wave of corporate defaults and bankruptcies that could be coming as high interest rates batter US companies. Experts warn it could raise the odds of a recession as high interest rates take their toll on businesses and consumers alike. 516 companies have filed for bankruptcy as of the end of September, according to S&P Global. That number already surpasses the total number of bankruptcy filings recorded in 2021 and 2022.”

What we’re reading (11/23)

“Recession? The Inverted Yield Curve Is Stabilizing. What It Means.” (Barron’s). “The yield curve inversion appears to have stopped narrowing, and that’s not necessarily a bad thing.”

“25% Of Americans Still Have Holiday Debt From Last Year: ‘If You’re In A Hole, Stop Digging,’ Says Money Expert” (CNBC). “For some shoppers, the upcoming holiday season may lead to piling on more debt. About 25% of Americans are still paying off holiday debt from 2022, according to WalletHub’s November holiday shopping survey.”

“Electric Vehicles: Automakers Fail To Dent Tesla’s Lead” (The Week). “‘Normally a 50% increase in sales is considered very good,’ said Jack Ewing in The New York Times. But when it comes to electric vehicles, it’s an alarming slowdown. EVs are still selling ‘faster than any other major category of automobiles.’ They now account for 8% of the total market for new cars sold in the U.S., up from 6% a year earlier. But recently released sales numbers show growth dipping from a year ago, when EV sales were rising at a pace of about 70% year. The data cast ‘doubt on whether generous federal tax credits for EV buyers were working as well as policymakers had hoped,’ and General Motors and Ford, who have pledged billions toward manufacturing more battery powered cars, seem noticeably anxious. Ford recently paused $12 billion in planned spending on EV production, while GM has pushed back launches of a slate of electric trucks and SUVs.”

“The Unproductive Entrepreneurship Of Silicon Valley” (Daniel Drezner). “[W]hat if the reason for government intervention comes from the incompetence and malfeasance of, you know, the entrepreneurs of Silicon Valley? Never forget that it was the likes of Andreessen that invested considerable amount of time and capital into cryptocurrencies, proclaiming that U.S. ‘hyperinflation’ meant a switch to crypto was inevitable. Ironically, it was precisely when U.S. inflation spiked that crypto crashed. The crypto market was not regulated much at all, and the result has been an awful lot of schemes, scams, and cons defrauding the uninformed. That accurately describes what Silicon Valley progeny Sam Bankman-Fried tried to do, and the outcome for him and his investors was pretty bad.”

“The Housing Market Will Be Stuck In A Rut For A Long Time Even If The US Avoids A Recession, Fannie Mae Says” (Business Insider). “The housing market isn't coming out of its deep freeze anytime soon, even if the US economy manages to steer away from a recession in the next year, according to Fannie Mae economists. The government-sponsored mortgage giant highlighted the stagnant US housing market, with existing home sales down 18.9% year per-year in June, according to Fannie Mae's estimate. Mortgage applications, similarly, have fallen to a 28-year-low.”

What we’re reading (11/22)

“Dow Closes Nearly 200 Points Higher Wednesday As Markets Head Into Thanksgiving” (CNBC). “More than half of the stocks trading on the New York Stock Exchange were up Wednesday, indicating widening breadth for the market rally. The tech-heavy Nasdaq also saw greater participation, with 62.9% of the stocks in the index rising. Small- and mid-caps outperformed Wednesday, rising 0.7% and 0.6%, respectively.”

“Binance Guilty Plea Shows What Crypto’s Really About” (Wall Street Journal). “So it turns out that of the two largest crypto exchanges, one was a fraud and the other was a money launderer. Whoever could have guessed? Skeptics of bitcoin and other cryptocurrencies have had their prejudices reinforced. The two main use cases—fraud and crime—have been exposed to the public in dramatic fashion, so now all we have to do is sit back and wait for the inevitable collapse in value.”

“Deutsche Bank, Which Revamped Its Compliance Department 18 Months Ago, Is Revamping Its Compliance Department” (Dealbreaker). “Just over a year-and-a-half ago, Deutsche Bank had a startling revelation: Perhaps, just possibly, the firm’s almost unfathomably awful decade, riddled as it was with fines and failures and regulators complaining about its compliance procedures, had something to do with weakness in, uh, its compliance procedures. Armed with the uncharacteristic bit of self-knowledge, Deutsche proceeded to overhaul those procedures. As the very same compliance department’s busy last 18 months show, said overhaul didn’t exactly work. So the Germans are going to take a page from its many, many regulatory detractors, and simply try the same thing in expectation of a different outcome.”

“The Fallout From Sam Altman’s Return To OpenAI” (Dealbook). “OpenAI’s board will be revamped. Gone are Tasha McCauley, Helen Toner and Ilya Sutskever, three of the four directors who ousted Altman. An “interim” board will take over, led by Bret Taylor, the former Salesforce co-C.E.O., and including Larry Summers, the former Treasury secretary, and Adam D’Angelo, the Quora C.E.O. and a holdover from the last board. That board will help select a bigger permanent one, according to The Verge, which may include representation for Microsoft, OpenAI’s biggest investor. Satya Nadella, Microsoft’s C.E.O., called the development “a first essential step on a path to more stable, well-informed, and effective governance.” It’s not clear what other changes are coming.”

“Dollarization For Argentina?” (Scott Sumner, EconLib). “With Javier Milei’s recent election victory, there is speculation that Argentina might drop the peso and dollarize its economy. I won’t speculate on how likely that is to occur, as I don’t know much about the political situation in Argentina. But I do have a few comments on the economics of dollarization: 1. Dollarization would solve the problem of hyperinflation. 2. If Argentina intends to dollarize, now would be a good time to do so. 3. Dollarization is not a panacea. Argentina still needs Chilean-style economic reforms, and there’s no guarantee that dollarization would lead to those reforms. 4. Dollarization is less risky than a currency board, but not completely free of risk.”

What we’re reading (11/21)

“Binance Crypto Chief Changpeng Zhao Pleads Guilty To Federal Charges” (Washington Post). “Changpeng Zhao, founder of the world’s largest crypto exchange, pleaded guilty Tuesday to violating the Bank Secrecy Act and has agreed to step down as chief executive of Binance, which will pay a $4.3 billion fine, according to court documents.”

“Nvidia’s Sales Surge, With No End In Sight For AI Boom” (Wall Street Journal). “In its latest period, its fiscal third quarter, sales more than tripled to $18.1 billion, well above Wall Street forecasts in a survey of analysts by FactSet. Profits also surged, rising to $9.2 billion compared with $680 million a year earlier and above estimates.”

“Microsoft Exec Says OpenAI Employees Can Join With Same Compensation” (CNBC). “It is not immediately known if the offer is contingent on Altman’s employment at Microsoft. Scott did not respond to CNBC’s request for comment on X. But, the comment gives some clarity to what Microsoft is willing to pay employees and how many it would hire.”

“US Stocks End Streak Of Gains As Fed Minutes Indicate A Restrictive Policy Outlook” (Insider). “US stocks fell on Tuesday with the S&P 500 snapping a five-session winning streak as the latest Fed minutes hinted at a hawkish-leaning central bank. The report dampened hopes for an imminent Fed pivot to rate cuts. Still, no further rate hikes are expected, and an overwhelming majority continue to expect rates to remain at the current 5.25%-5.50% range.”

“US Home Sales On Pace For The Worst Year Since 1993” (CNN Business). “Home sales may have their worst year in 30 years. Sales slumped in October and prices continued to climb, as mortgage rates surged last month and inventory remained extraordinarily low. That kept homebuyers out of the market, according to a monthly report from the National Association of Realtors released Tuesday.”

What we’re reading (11/16)

“Amazon Will Allow Auto Dealers To Sell Cars On Its Site, Starting With Hyundai” (CNBC). “Beginning in 2024, Amazon will let shoppers purchase a new car online, then pick it up or have it delivered by their local dealership. Consumers will be able to search for available vehicles in their area, make a selection, then check out on Amazon using their preferred payment and financing method. The company said the new feature will ‘create another way for dealers to build awareness of their selection and offer convenience to their customers.’”

“These Stocks Are Trailing The Market By The Widest Margin In 25 Years” (Wall Street Journal). “Smaller, speculative companies are in the midst of a furious autumn stock-market rally, but they still have an interest-rate problem. The S&P 600, an index of small companies with an average market value of $1.8 billion, has climbed 8% from its recent low on Oct. 27, slightly trailing the S&P 500. Yet for 2023, it is on pace to trail its large-cap counterpart by the widest margin in a calendar year since 1998. The S&P 600 is up 0.1%, while the S&P 500 has climbed 17%. The Federal Reserve’s interest-rate campaign has hurt small-caps more than their larger peers because small companies tend to issue more floating-rate debt.”

“One-Third Of U.S. Newspapers As Of 2005 Will Be Gone By 2024” (Axios). “The decline of local newspapers accelerated so rapidly in 2023 that analysts now believe the U.S. will have lost one-third of the newspapers it had as of 2005 by the end of next year — rather than in 2025, as originally predicted. Most communities that lose a local newspaper in America usually do not get a replacement, even online.”

“Forget Climate Change & NBFIs, The Biggest Systemic Risk Are The Unrealized Losses In The Banking System” (American Enterprise Institute). “I estimate that, as of June 30, 2023, there were 2372 banks that collectively held 54 percent of the total assets in the banking system with mark-to-market adjusted Tier 1 leverage ratios under 4 percent, the prompt corrective action threshold that classifies a bank as ‘significantly undercapitalized’.”

“America’s Top 1% Don’t Make As Much As You Might Think” (Tyler Cowen in Bloomberg). “Can a single self-published paper really refute decades of work by three famous economists? If the paper is the modestly titled ‘Income Inequality in the United States: Using Tax Data to Measure Long-Term Trends,’ then the answer — with qualifications — is yes…At the very least, the presumption in favor of Piketty, Saez and Zucman is now gone. For the time being, there are better arguments, based on better data, that suggest very different conclusions.”

What we’re reading (11/15)

“US Stocks Close Higher As Investors Cheer Fresh Data Showing Inflation Is Easing” (Business Insider). “US stocks closed higher on Wednesday, extending gains from Tuesday's sharp rally after fresh data showed a continued decline in inflation. The Producer Price Index fell 0.5% in October from the prior month, representing the largest decline since April 2020 and a sharp reversal from the 0.4% gain seen in September. On an annual basis, the PPI rose 1.3%, down from 2.2% in September. The reading follows Tuesday's Consumer Price Index report, which showed prices paid by consumers rose less than expected last month.”

“The Elusive Soft Landing Is Coming Into View” (Wall Street Journal). “Six months ago, the consensus among economists surveyed by The Wall Street Journal was that the economy would enter a recession over the next 12 months. In October’s survey, the average forecast of economists was for no recession. After Tuesday, the probability appears to have dropped further. That, at least, seems to be the verdict of investors who sent stocks up sharply and Treasury bond yields down on news that inflation was surprisingly docile in October. If they are right, it would be highly unusual. In the past 80 years, the Federal Reserve has never managed to bring inflation down substantially without sparking a recession.”

“The Inflation Rally Goes Global” (DealBook). “Market optimists have moved up their bets on rate cuts. Futures markets this morning pointed to the Fed starting to lower borrowing costs by May, sooner than previous estimates of closer to the end of 2024. Less aggressive is Mohit Kumar, the chief financial economist at Jefferies, who wrote today that big rate cuts would begin after the presidential election next year. Jefferies predicts the Fed’s prime lending rate going to 3 percent by the end of 2025 from its current level of 5.25 to 5.5 percent.”

“The Market Thinks The Fed Is Going To Start Cutting Rates Aggressively. Investors Could Be In For A Letdown” (CNBC). “While Fed officials haven’t indicated how many months in a row it will take of easing inflation data to reach that conclusion, 12-month core CPI has fallen each month since April. The Fed prefers core inflation measures as a better gauge of long-run inflation trends. Traders appear to have more certainty than Fed officials at this point. Futures pricing Wednesday indicated no chance of additional hikes this cycle and the first quarter percentage point cut coming in May, followed by another in July, and likely two more before the end of 2024, according to the CME Group’s gauge of pricing in the fed funds futures market.”

“The Rise And Fall Of The World’s Most Successful Joint Venture” (New York Times). “No one uses words like symbiotic today. In Washington, two political parties that agree on almost nothing are united in their depictions of China as a geopolitical rival and a mortal threat to middle-class security. In Beijing, leaders accuse the United States of plotting to deny China’s rightful place as a superpower. As each country seeks to diminish its dependence on the other, businesses worldwide are adapting their supply chains.”

What we’re reading (11/14)

“Cooling Inflation Likely Ends Fed Rate Hikes” (Wall Street Journal). “Inflation’s broad slowdown extended through October, likely ending the Federal Reserve’s historic interest-rate increases and sparking big rallies on Wall Street. Consumer prices overall were flat last month and rose 3.2% from a year earlier, a slower pace than in September, the Labor Department said Tuesday. Overall inflation hit a recent peak of 9.1% in June 2022.”

“S&P 500 Notches Best Day Since April, Dow Leaps Nearly 500 Points On Soft Inflation Report” (CNBC). “Stocks rallied Tuesday, building on their strong November gains, as Wall Street cheered new U.S. inflation data that raised hopes of the Federal Reserve wrapping up its rate-hiking campaign. The Dow Jones Industrial Average jumped 489.83 points, or 1.43%, to end at 34,827.70. The S&P 500 rallied 1.91%, briefly trading above the key 4,500 level, to settle at 4,495.70. It was the best day since April for the broad-market index. The Nasdaq Composite jumped 2.37% to close at 14,094.38.”

“RIP Goldman Sachs” (Business Insider*). “‘It's not the swashbuckling traders of old, and I do think there's some lost romance there,’ says Dees, my fellow analyst who now heads global banking and markets for Goldman. ‘There's a lot of people who look and say, ‘Ah, that period of yesteryear where someone could put a trade on distressed credits in Thailand and make a billion dollars and beat his chest’ — I get it. But that's not realistic. They're nostalgic for a thing that can't exist today at any bank, under the current regulatory system. This place is still about excellence. It's just going to have to be in a different format.’”

“Macro Outlook 2024: The Hard Part Is Over” (Goldman Sachs). “We continue to see only limited recession risk and reaffirm our 15% US n recession probability. We expect several tailwinds to global growth in 2024, including strong real household income growth, a smaller drag from monetary and fiscal tightening, a recovery in manufacturing activity, and an increased willingness of central banks to deliver insurance cuts if growth slows.”

“Investor Michael Burry Of ‘Big Short’ Fame Has Closed Bets Against S&P 500, Nasdaq” (Yahoo! Finance). “Burry's hedge fund Scion Capital disclosed Tuesday in a federal filing with the SEC that it had closed out "put" positions on the SPDR S&P 500 ETF (SPY) and Invesco QQQ Trust (QQQ), which tracks the Nasdaq 100 index, as of the end of September. Those bearish bets amounted to more than $1.6 billion as of the last trading day of the second quarter. The indexes fell 3.6% and 3%, respectively, during the third quarter.”

* Note: As of today, Insider is apparently going back to going as “Business Insider” (see letter from the editor, here).

What we’re reading (11/13)

“Silicon Valley VCs Wanted To Believe SBF’s Lies. Now They Want You To Believe Their Excuses” (Los Angeles Times). “Sequoia Capital wants you to know that it was ‘deliberately misled and lied to’ by convicted cryptocurrency scam artist Sam Bankman-Fried during the discussions that led to its $213.5-million investment in Bankman-Fried’s firm, FTX, last year. That’s an extraordinary admission, given that Sequoia is one of Silicon Valley’s oldest and largest venture investing firms, with an estimated $28.3 billion in assets under management. Yet that’s what Sequoia partner Alfred Lin, who was involved in advancing the FTX investment, asserted following Bankman-Fried’s conviction on seven fraud counts Thursday. ‘Today’s swift and unanimous verdict confirms what we already knew,’ Lin tweeted that day: ‘that SBF misled and deceived so many, from customers and employees to business partners and investors, including myself and Sequoia.’”

“What Is The Goal Of The 60/40 Portfolio?” (Manhattan Institute). “No one can agree whether the main purpose is to diversify or to reduce risk — and they aren’t quite the same thing. I am not a fan of one-size-fits-all financial strategies. Yes, I see the value of making investment as simple as possible, but the right balance of risk and reward is a personal decision, and the most common strategies are either arbitrary or agnostic about crucial details. Which brings me to the subject of this column: the popular yet endlessly criticized 60/40 asset allocation strategy. With bond prices tanking and correlations flipping, last year the 60/40 portfolio had its worst returns in decades. Then again, maybe that was just a blip and investors just need to wait it out.”

“Strip Clubs, Lewd Photos And A Boozy Hotel: The Toxic Atmosphere At Bank Regulator FDIC” (Wall Street Journal). “A toxic work environment at the FDIC, one of the nation’s top banking regulators, has for years caused employees to flee from an agency they say enabled and failed to punish bad behavior, according to a Wall Street Journal investigation based on interviews with FDIC employees as well as legal filings, union grievances, Equal Employment Opportunity complaints, emails, text messages and other internal documents.”

“Inside The Strange, Secretive Rise Of The ‘Overemployed’” (Insider). “[L]ess than a year into the job at IBM, when a recruiter from Meta came calling, [Bryan] Roque had a thought. The normal thing would be to quit his old job and accept the new position, which was also fully remote. But what if he kept his old job, and secretly took on the new one, too? All he had to do was two-time IBM, and he could double his income as well as his job security.”

“Airlines Predict Record Thanksgiving US Holiday Travel” (Reuters). “Airlines for America, an industry group representing American Airlines United Airlines, Delta Air Lines and others, forecasts 29.9 million passengers between Nov. 17-27, an all-time high and up 9% over the 27.5 million in the same period last year -- and up 1.7 million passengers over pre-COVID record levels.”

What we’re reading (11/12)

“Is The Stock Market Rally About To Rev Up?” (Wall Street Journal). “FOMO in the stock market is back. A lightning-fast rebound has driven the S&P 500 up in nine of the past 10 sessions and 7.2% over the past two weeks, the best such stretch of the year. Now, many investors are betting the rally has legs. Some have piled into funds tracking U.S. stocks, while others have abandoned trades that would profit in times of market turmoil. Many have slashed bearish wagers against the S&P 500 and tech-heavy Nasdaq-100 index, fearful of getting caught flat-footed if the big gains continue.”

“Welcome To Hochatown, The Town Created By Airbnb” (New York Times). “But the company’s [AirBnB’s] report also contained a data point that is reverberating through Airbnb boom towns like Hochatown: For the first time since the pandemic recovery, Airbnb’s supply of rental homes is outpacing demand, with supply increasing 19 percent year over year, compared to just 14 percent for demand. That gap can spell disaster for hosts, particularly those who bought houses at the peak of the market with the idea of renting them out. In extreme cases, they are being forced to sell at a loss.”

“Ray Dalio’s Response To ‘The Fund,’ A New Book That Dissects Bridgewater Associates” (Institutional Investor). “Dalio and Bridgewater, which threatened legal action against Copeland and his publisher before the book came out, blasted it Tuesday. In a LinkedIn post, Dalio said the book is ‘another one of those sensational and inaccurate tabloid books written to sell books to people who like gossip. The only thing that’s different about this one is that it’s about me and Bridgewater.’ The billionaire went on to say that Copeland applied for a job at Bridgewater and was rejected before he went on to become a reporter who ‘made a career of writing distorted stories about me and Bridgewater.’ Dalio has said similar things in the past about Copeland and his unfavorable reporting about the founder and the firm. Copeland is an award-winning investigative journalist for The New York Times, who previously spent 10 years covering hedge funds for The Wall Street Journal and worked at Institutional Investor.”

“Your 401(k) Is Falling Behind. Here’s What You Should Do.” (Wall Street Journal). “As tempting as it may be to meddle with your investments, history suggests most investors have a lousy record of timing the market. Financial advisers say the vast majority of Americans should stick to time-tested advice and simply do nothing.”

“36-Hour Shifts, 80-Hour Weeks: Workers Are Being Burned Out By Overtime” (NBC News). “From firehouses and police stations to hospitals and manufacturing plants, workers say they are being required to work increasing overtime hours to make up for post-pandemic worker shortages — leaving them sleep-deprived, scrambling to cover child care duties, and missing birthdays, holidays and vacations. While the extra hours can provide a financial boost, some workers say the trade-off is no longer worth it as they see no end in sight to a problem that has now lasted for several years.”

What we’re reading (11/11)

Happy Veterans Day!

“Claudia Sahm: ‘We Do Not Need A Recession, But We May Get One’” (Financial Times). “What I do know is that the US economy is leaving 2023 in a better place than when it came into it, and a better place than the vast majority of commentators thought it would be in. On balance, inflation is still higher than we had expected, but for almost two years running we’ve had unemployment below 4 per cent, [strong] inflation-adjusted GDP growth and real consumer spending, too. So if you take it all together, that’s really good. And the thing that happened this year that wasn’t supposed to happen was inflation came down markedly and unemployment stayed low. That opens up a conversation of whether we need to have a recession. I have said the whole time that we do not need a recession, but we may get one.”

“Bonds vs. Bond Funds: How Higher Rates Are Changing The Calculation” (Wall Street Journal). “During the yearslong period of near-zero interest rates, the answer seemed simple: Funds had low fees and were easy to buy and sell, and share values rose alongside bond prices. If any one bond defaulted, losses were minimal. The historic declines suffered by major bond funds last year highlighted the risks of that approach. Rising rates crushed funds’ share prices. That is because bond prices drop when new higher-yielding bonds come on the market and make older, lower-yielding bonds less attractive. Because funds’ share values are based on the market price of their bonds, someone who bought shares a few years ago could end up cashing out today with less money than they put in.”

“Google In-House Attys Joked About ‘Fake Privilege,’ Jury Told” (Law360). “Two in-house Google lawyers communicating on an internal company chat joked about ‘fake privilege’ — a practice of unnecessarily involving a lawyer in a matter to make it confidential — an attorney for Epic Games showed jurors in a California federal antitrust case against the tech giant.”

“Xi Jinping’s ‘Old Friends’ From Iowa Get A Dinner Invitation” (Bloomberg). “A group of Chinese President Xi Jinping’s “old friends” from Iowa have been invited to a dinner he will attend in California next week — 38 years after they welcomed the then-unknown party official for a hog roast, farm tours and a Mississippi River boat ride as they showed him how capitalists do agriculture.”

“Inside An OnlyFans Empire: Sex, Influence And The New American Dream” (Washington Post). “In the American creator economy, no platform is quite as direct or effective as OnlyFans. Since launching in 2016, the subscription site known primarily for its explicit videos has become one of the most methodical, cash-rich and least known layers of the online-influencer industry, touching every social platform and, for some creators, unlocking a once-unimaginable level of wealth…If OnlyFans’s creator earnings were taken as a whole, the company would rank around No. 90 on Forbes’s list of the biggest private companies in America by revenue, ahead of Twitter (now called X), Neiman Marcus Group, New Balance, Hard Rock International and Hallmark Cards.”

What we’re reading (11/10)

“How Risky Is Private Credit? Analysts Are Piecing Together Clues” (Wall Street Journal). “‘If rates stay higher for longer—or higher forever—then these companies are not equipped,’ said Ramki Muthukrishnan, head of U.S. leveraged finance at S&P Global. He said companies would struggle to pay their debt. Just 46% of the companies in the analysis would generate positive cash flow from their business operations under S&P’s mildest stress scenario, in which earnings fell by 10% and the Fed’s benchmark rates increased by another 0.5 percentage point, the ratings firm said.”

“Citadel’s Ken Griffin Sees High Inflation Lasting For Decades” (MarketWatch). “…Ken Griffin, head of the Miami-based hedge-fund manager Citadel, said higher baseline inflation may go on for decades, caused by structural changes that are pushing the world toward de-globalization.”

“Moody’s Cuts U.S. Outlook To Negative, Citing Deficits And Political Polarization” (CNBC). “‘In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues,’ the agency said. ‘Moody’s expects that the US’ fiscal deficits will remain very large, significantly weakening debt affordability.’”

“Has IBM Built The Next Generation’s 401(k) Plan?” (Morningstar). “Whatever its name, the introduction of the RBA converts IBM’s employee-retirement plan into a hybrid scheme. It will now consist partially of a defined-contribution plan and partially of a defined-benefit plan. Such arrangements are not unique, but they are unusual—particularly when openly coupled with the decision to cancel the company’s 401(k) match program.”

“How To Hijack A Quarter Of A Million Dollars In Rare Japanese Kit Kats” (New York Times). “These particular Kit Kats would become the key players in an ultimately frustrating saga of shell email accounts, phantom truckers, supply-chain fraud and one seriously bewildered cargo freight broker. Interviews and emails shared with The New York Times tell the story of just one instance of ‘strategic theft,’ a growing corner of the criminal world that the F.B.I. has said accounts for some $30 billion in losses a year — with food being among the top targets.”