August/September Performance Update

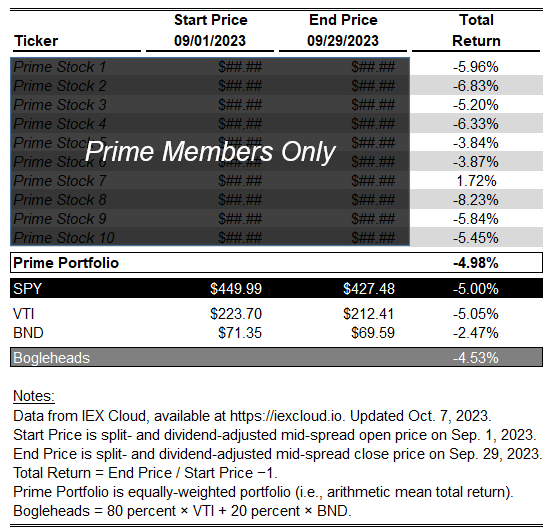

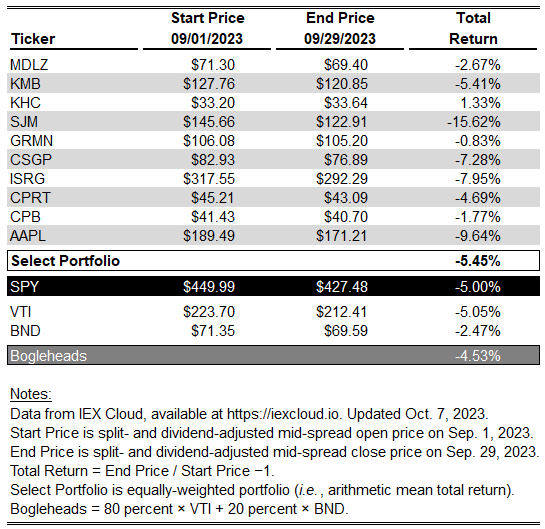

Here with a performance update for the last two months, but I don’t have much of substance to report as the Prime and Select strategies’ performance, in combination, were not materially different from the market’s.

In August, Prime underperformed by about 100 bps; on the other hand, Select outperformed by over 160 bps. In September, Prime was almost exactly in line with the market, while Select gave back some of the prior month’s relative gains. In repeated samples (more than the two reported here) performance matching the market’s would support an inference that the factors Prime and Select index on don’t matter much. A subtly different inference would be that those factors don’t seem to matter much right now, perhaps because other systematic risk factors (rates, the resolution of macro growth uncertainty) are dominating the performance of all equities. Believers in the Halloween Effect would note that we are now entering the six months of the year where stocks tend to perform relatively better. Based on the market’s performance year-to-date, 2023 would seem to be another data point supporting that theory. Stay tuned!