What we’re reading (8/24)

“How Costco Hacked The American Shopping Psyche” (New York Times). “In 2019, one quarter of U.S. consumers shopped at Costco. Today it is nearly one-third. Costco is the third-largest retailer in the world, behind only Amazon and Walmart. But the success of Costco goes far beyond hoarding. The company has hacked the psyche of the American consumer, appealing to both the responsible-shopping superego (‘Twelve cans of tuna for $18!’) and the buy-it-now id (‘I deserve that 98-inch flat screen’).”

“Preliminary Benchmark Revisions Wipe Out 30% Of Jobs Growth In The Past 16 Months” (Angry Bear). “Every month I write about the Jobs Report. But while it is timely, it is only an estimate. There is an actual census of over 95% of all employers that also gets reported, called the QCEW, and it is the “gold standard” of actual jobs growth (or loss). Its two drawbacks are that it is not seasonally adjusted, and it is reported almost 6 months after the end of the quarter it updates. Which is a lengthy introduction to saying that it was just reported through March of this year this morning. More importantly, the BLS preliminarily re-benchmarked all of its data beginning in March of last year. And which is a further introduction to saying that, as expected, job growth was a lot less late last year and earlier this year than we originally thought.”

“What We Know About Kamala Harris’s $5 Trillion Tax Plan So Far” (New York Times). “In a campaign otherwise light on policy specifics, Vice President Kamala Harris this week quietly rolled out her most detailed, far-ranging proposal yet: nearly $5 trillion in tax increases over a decade.”

“The Hell Of Self-Service Checkouts Is Becoming Kafkaesque” (The Telegraph). “The cost of living crisis hasn’t helped and supermarket chains are responding [to theft] with ever-more Kafkaesque security measures. For example, there are now shops where you can’t pass through an exit barrier until you’ve swiped your receipt. A friend recently went into a branch of Sainsbury’s on a futile quest for avocados, only to find she couldn’t leave as there were no assistants in sight and she had not forked out money. In the end, she had to buy some crisps solely to exit, which was effectively blackmail.”

“Messing Up The Closest Thing To A Sure Thing In The Stock Market” (Wall Street Journal). “Over the 10 years ended Dec. 31, 2023, Morningstar found, investors in the aggregate earned an average of 6.3% annually, or 1.1 percentage points less than the mutual funds and ETFs they owned. That echoes earlier findings from Morningstar and several academic and other studies. The consensus is clear: Investors typically underperform their investments, not just in mutual funds and ETFs, but in hedge funds and stocks as well.”

What we’re reading (8/19)

“Coming To A Cash-Strapped Company Near You: Creditor-On-Creditor Violence” (Wall Street Journal). “Grand alliances. Secret pacts. Betrayal. It’s all in a day’s work in the booming market for low-rated corporate debt. U.S. companies that struggle to repay their below-investment-grade bonds and loans have increasingly squeezed concessions from lenders by pitting them against one another. The private-equity firms and wealthy individuals who own most of the companies call the deals ‘liability management exercises,’ or LMEs. Debt investors call them ‘creditor-on-creditor violence.’”

“Alex Karp Has Money And Power. So What Does He Want?” (New York Times). “He’s not a household name, and yet Mr. Karp is at the vanguard of what Mark Milley, the retired general and former chairman of the Joint Chiefs of Staff, has called ‘the most significant fundamental change in the character of war ever recorded in history.’ In this new world, unorthodox Silicon Valley entrepreneurs like Mr. Karp and Elon Musk are woven into the fabric of America’s national security.”

“If The World Had A Hyperscale Datacenter Capital, It Would Be... Northern Virginia” (The Register). “If the internet can be said to have a geographic location, then perhaps it is Northern Virginia, which has the largest share of the hyperscale datacenter capacity within which the world's data is stored. Hyperscale companies accounted for 41 percent of the entire global bit barn presence last year, and this share is increasing, as The Register reported recently. Figures from Synergy Research Group show that Northern Virginia – close to Washington DC, and where the CIA is headquartered, FYI – accounts for nearly 15 percent of that entire hyperscale capacity – at least double that of where the next largest concentration can be found in Beijing, China.”

“Home Depot Issues A Warning About The Economy” (CNN Business). “The home improvement giant, a bellwether of consumer spending and the housing market, lowered its sales expectations for the year. It said customers were spending less on home improvement projects, pressured by higher interest rates and concerns that the economy is getting worse. Home Depot’s business is closely tied to the housing market, and high interest rates are putting a brake on housing turnover and consumers financing larger projects.”

“Private-Equity Firms Desperate For Cash Turn To A Familiar Trick” (Wall Street Journal). “Private-equity firms eager to pay their investors are returning to an old habit: loading up companies with risky debt. The rush into junk debt is letting buyout firms deliver payments to investors—and themselves—during a sharp slowdown in deals that is making it hard to sell portfolio companies. The transactions, which rely on low-rated debt, are known on Wall Street as dividend recapitalizations.”

What we’re reading (8/18)

“The CEO Who Made A Fortune While His Hospital Chain Collapsed” (Wall Street Journal). “Steward Health Care System was in such dire straits before its bankruptcy that its hospital administrators scrounged each week to find cash and supplies to keep their facilities running. While it was losing hundreds of millions of dollars a year, Steward paid at least $250 million to its chief executive officer, Dr. Ralph de la Torre, and to his other companies during the four years he was the hospital chain’s majority owner.”

“How A.I. Can Help Start Small Businesses” (New York Times). “[F]or some entrepreneurs, generative A.I. is already a game changer. It is helping them write intricate code, understand complex legal documents, create posts on social media, edit copy and even answer payroll questions. The result, they say, is that A.I. allowed them to get their companies off the ground more quickly, and more efficiently, than they would have without it.”

“Perspective Into The Pentagon’s U.F.O. Hunt” (New York Times). “Luis Elizondo made headlines in 2017 when he resigned as a senior intelligence official running a shadowy Pentagon program investigating U.F.O.s and publicly denounced the excessive secrecy, lack of resources and internal opposition that he said were thwarting the effort. Elizondo’s disclosures at the time created a sensation. They were buttressed by explosive videos and testimony from Navy pilots who had encountered unexplained aerial phenomena, and led to congressional inquiries, legislation and a 2023 House hearing in which a former U.S. intelligence official testified that the federal government has retrieved crashed objects of nonhuman origin. Now Elizondo, 52, has gone further in a new memoir. In the book he asserted that a decades-long U.F.O. crash retrieval program has been operating as a supersecret umbrella group made up of government officials working with defense and aerospace contractors. Over the years, he wrote, technology and biological remains of nonhuman origin have been retrieved from these crashes.”

“‘Dr Doom’ Files To Launch ETF Based On His Calamitous Outlook” (Financial Times). “Nouriel Roubini, aka Dr Doom, has been dishing up his downbeat takes on the global economy and markets for decades. Now investors will finally get the chance to see how his gloomy insights translate into financial returns as Roubini, who earned his Dr Doom moniker for foreseeing the 2008 global financial crisis, turns to managing money for the first time at the age of 66.”

“Insider Trading By Other Means” (Harvard Business Law Review). “For more than thirty years, one of the most prevalent strategies for insider trading has gone undetected and unaddressed. This Article uncovers the techniques by which executives and directors sell overvalued stock worth more than $100 billion per year, shifting losses to ordinary investors. The basic idea is that insiders conceal their suspicious trades by publicly reporting them (as they are required to do) in ways that confuse or discourage investigators. We develop a taxonomy of concealment strategies, complete with suggestive examples. We then empirically test our taxonomy using a database of essentially all stock trades since 1992. We find that insiders who trade using the subterfuges we describe outperform the market by up to 20% on average. Worse yet, we find evidence that this simple subterfuge works. Essentially no one has ever been prosecuted for undertaking one of these suspicious trades. Nor do journalists or scholars seem to appreciate them. Accordingly, we call for scholars and prosecutors to cast a wider net in their studies and market surveillance, then discuss implications for the design of insider-trading reporting requirements and related legal rules.”

What we’re reading (8/17)

“The Extreme Renters Who Own Nothing, Not Even Their Jeans” (Wall Street Journal). “Brittany Catucci rents everything she can. Like lots of 20-somethings, she doesn’t own the place where she lives, a three-story townhouse in Emeryville, Calif. But she and her boyfriend, Eric Markley, also rent their queen-size bed, Catucci’s work clothes and repair tools from Home Depot or AutoZone.”

“New Real Estate Rules Sow Confusion, At Least in Short Term” (New York Times). “The changes that went into effect this weekend decouple the two commissions: Sellers are no longer expected to pay buyers’ commissions, though they can still choose to do so, and the proposed commission split can no longer be advertised on the online database commonly used to sell homes, the M.L.S.”

“Inside The $93 Million Wall Street Heist That Stemmed From Russia” (CNBC). “The money Vladislav Klyushin made from stolen financial information literally piled up, filling a safe with stacks of hundred-dollar bills. At one point, he was hoarding over $3 million in illegal gains. In less than three years, Klyushin’s cybersecurity scam amassed more than $93 million. His company, M-13, acted as a front for Russian hackers to steal information under the guise of protecting it, getting their hands on American corporate earnings reports before the rest of the world could see them. Then, they traded based on that insight, buying and selling stock from well-known American companies like Skechers, Snapchat and Roku.”

“Alleged Ponzi Scheme Salesman Either A Bad Speller Or A Literate Masochist” (Dealbreaker). “There are some notable things about the nine-figure fraud allegedly perpetrated by St. Augustine’s Russell Todd Burkhalter. For one, his Drive Planning’s pitch deck noted that the “bridge loan opportunities” offered were backed by $113 million in cash and real estate—in other words, one-third of the money he raised, such that he could conceivably have actually backed those “opportunities” with that amount of collateral and still had nearly $200 million to spend on Ponzi payments and other things.”

“Democratic Favor Channel” (Dealbreaker). “A large body of literature in economics and political science examines the impact of democracy and political freedoms on various outcomes using cross-country comparisons. This paper explores the possibility that any positive impact of democracy observed in these studies might be attributed to powerful democratic nations, their allies, and international organizations treating democracies more favorably than nondemocracies, a concept I refer to as democratic favor channel. Firstly, after I control for being targeted by sanctions from G7 or the United Nations and having military confrontations and cooperation with the West, most of the positive effects of democracy on growth in cross-country panel regressions become insignificant or negatively significant.”

What we’re reading (8/15)

“Stock Indexes Rally After Data Calm Economic-Slowdown Fears” (Wall Street Journal). “The S&P 500 climbed 1.6% Thursday, rising for a sixth consecutive session. The tech-heavy Nasdaq Composite added 2.3%, while the Dow Jones Industrial Average rose 1.4%, or about 550 points. A trio of fresh data points reassured investors that consumer spending, the backbone of the U.S. economy, is holding up.”

“Investors Are Piling Into This Area Of Fixed Income For Protection Against Election And Market Volatility — And For Lower Taxes” (Business Insider). “Dan Close, head of municipals at the $1.2 trillion global investment manager Nuveen, is seeing increased appetite for these government-backed debt instruments. While 2022 and 2023 saw large net outflows from the muni market, 2024 has seen $12 billion of inflows year-to-date.”

“The Change That Realtors’ Powerful Trade Group Resisted For Decades Is Finally Happening” (CNN Business). “Starting this Saturday, the days of the standard 6% commission — two to three times what agents make in other developed economies — are effectively over. Sellers, who historically have paid both the listing agent and the buyer’s Realtor, will be on the hook for their agent’s fee. Buyers and their agents will negotiate a compensation plan upfront. ‘It’s a partial deregulation of a marketplace that was regulated not by government, but by the industry,’ said Stephen Brobeck, senior fellow at the Consumer Federation of America, a nonprofit advocacy group. ‘In the long run, it’s going to be a very good thing.’”

“The Unraveling Of A Crypto Dream” (New York Times). “But Mr. Pierce’s vision of a crypto-fueled economic turnaround has yet to materialize, according to hundreds of pages of court records and interviews with more than two dozen people familiar with his efforts in Puerto Rico. His business partners have turned on him, and some colleagues say he is running out of cash. There is no clear evidence that the arrival of tech entrepreneurs has helped the local economy.”

“Tax-Free Tips” (Marginal Revolution). “If the demand for labor is inelastic, the value of a wage subsidy is captured primarily by the employer. The wage subsidy arrives, and the employer does not start trying to hire more labor as a consequence. After all, the demand for labor is inelastic. Since the demand for labor has not gone up, the net wage does not go up in the final equilibrium. The employer can just keep the subsidy, or if the subsidy is given to the worker, the employer can lower wages (or the quality of working conditions), leaving the previous net wage intact and the worker will not leave. So if you think minimum wage hikes are a decent idea, you also ought to think that non-taxed tips will benefit the boss, not the workers.”

What we’re reading (8/14)

“Venture Capital’s New Reality Check: ‘A Ton Of People Looking To Get Out Everywhere’” (Business Insider). “During the zero-interest-rate years, the ranks of the VC industry swelled…Now, the market downturn has cast many aspects of the industry in a harsh light. Rising interest rates, delayed initial public offerings, and a slump in public markets have hit the venture industry hard…Poor fund performance has made carry worthless, a growth-stage principal said. Many investors received meaningful carry in funds only a few years ago. But funds from the pandemic years didn't perform well because many companies were overvalued.”

“Mars’ Biggest Deal Clinched By Secretive, Deep-Pocketed Family” (Reuters). “A running joke among residents of McLean, Virginia is that the most secretive organization headquartered in their Washington D.C. suburb is not the Central Intelligence Agency, but rather a confectionery and pet products company. Here, the second-richest U.S. family runs Mars Inc, maker of M&M's candies and Pedigree pet food, out of a nondescript building with no corporate logo or any other identifying signage. The CIA's offices, on the other hand, even have a parkway exit sign…Mars, flush with cash and dominant in the food categories it is active in, decided to place its biggest ever bet on expansion -- the $36 billion acquisition of snack and cereal maker Kellanova it announced on Wednesday.”

“In Mars Megadeal, Big Food Wants To Get Bigger” (Wall Street Journal). “The agreement, one of the biggest on record among food makers, comes as consumers are balking at higher grocery prices and scrutiny is growing over the potential health impacts from processed food. Conditions are ripe for a fresh wave of consolidation as food companies’ sales growth slows and their stock-market valuations are depressed, according to Wall Street analysts and consultants. Pandemic-era pantry stocking and sharp price increases that continued in its aftermath fueled a sales boom for food companies. That growth has cooled, prompting executives to search for new ways to boost their businesses and cut expenses.”

“What Should We Do About Google?” (New York Times). “[C]onsider the remedies imposed on AT&T, the greatest tech monopoly of the 20th century. In 1956, the Justice Department settled a major antitrust suit against AT&T by requiring the company to stay out of computing — and to license, free, all of its 7,820 patents.”

“Temasek Spent Billions On US Tech Stocks Before July Selloff” (Yahoo! Finance). “Temasek increased the value of its holdings in 11 big tech firms by $3.3 billion in the three months ended June 30, according to an analysis of its two most recent 13F filings. The vast bulk of the increase — some $3.2 billion — went into six of those firms: Microsoft Corp., Apple Inc., Nvidia Corp., Alphabet Inc., Meta Platforms Inc. and Amazon.com Inc. By the end of July, however, most of those companies saw their stocks slide amid concern about the extent of AI-related gains and fears of a recession. Alphabet and Amazon’s share prices have fallen by about 12% since the end of June, while Microsoft’s are down around 7% over that period.”

What we’re reading (8/13)

“Markets Might Have Recovered. Investors’ Nerves Haven’t.” (Wall Street Journal). “[M]y guess is last Monday’s plunge shifted the psychology again. That’ll mean sellers appear more quickly when prices rise, and buyers are more reluctant to join in when prices fall. Watch out below.”

“Wall Street’s ‘Fear Gauge’ Might Be Lying To You About Last Week’s Market Turmoil” (Financial Times). “Based on the CBOE VIX’s intraday peak of 65.73, the market event that has been branded the ‘Summer Selloff’…was, as wags have been keen to point out, apparently one of the most significant volatility events to have ever hit US stocks. So was Monday August 5th really an event on par with the Covid-19 crash, the heights of the Notorious GFC, or Black Monday?”

“Starbucks Replaces CEO Laxman Narasimhan With Chipotle CEO Brian Niccol” (CNBC). “Starbucks announced Tuesday it’s replacing CEO Laxman Narasimhan with Chipotle CEO Brian Niccol, sending its stock soaring 24.5%, its best day ever. Chipotle’s stock fell over 10% on the news that Niccol would leave after a successful tenure at the burrito chain.”

“How To Read A Riot” (Financial Times). “What makes somebody riot? Why do people throw bricks at police while being filmed by dozens of phones, knowing it could get them a jail sentence that ruins their lives? Their decision may be political…[b]ut in fact, riots are not purely political events. They are more emotional than that. To understand them as a simple matter of rational actors calling for specific policies is to miss out a lot about why riots start, how they spread, and how authorities should respond.”

“Reservoir Of Liquid Water Found Deep In Martian Rocks” (BBC). “Scientists have discovered a reservoir of liquid water on Mars - deep in the rocky outer crust of the planet. The findings come from a new analysis of data from Nasa’s Mars Insight Lander, which touched down on the planet back in 2018. The lander carried a seismometer, which recorded four years' of vibrations - Mars quakes - from deep inside the Red Planet. Analysing those quakes - and exactly how the planet moves - revealed ‘seismic signals’ of liquid water.”

What we’re reading (8/8)

“S&P 500 Jumps 2.3% in Best Day Since 2022” (Wall Street Journal). “The S&P 500 posted its best day in nearly two years after a better-than-expected jobless claims report helped ease fears that the labor market is weakening. U.S. stock futures and Treasury yields rose immediately after the release of data showing initial jobless claims, a proxy for layoffs, were 233,000 during the week ended Aug. 3, down from the prior week’s recent high of 250,000. That helped alleviate some of the concern about a U.S. labor-market slowdown that rattled markets after last week’s weaker-than-expected jobs report.”

“U.S. Mortgage Rates Drop Sharply, With 30-Year At 6.47%” (New York Times). “Mortgage rates have fallen to their lowest level in more than a year, a balm for prospective home buyers and sellers in a challenging real estate market. The average rate on 30-year mortgages, the most popular home loan in the United States, dropped to 6.47 percent this week, Freddie Mac reported on Thursday.”

“Is There An AI Bubble — And Is It About To Pop?” (Vox). “How much is the future worth? Usually to answer that question, you’d need to ask philosophers or economists. But if you’re a tech CEO, you have an actual number: about $1 trillion. That’s how much the tech industry as a whole is set to spend building out the artificial intelligence industry over the coming years. And even in Silicon Valley, where several companies have market capitalizations that start with ‘T,’ a trillion dollars is a lot of money. And while you won’t find more fervent evangelists for AI anywhere than in the C-suite of companies like Google and Microsoft, eventually, all that money has to be recouped. The alternative would be an economic meltdown of the sort we haven’t experienced for years.”

“Paramount’s TV Networks Are Collapsing In A $6 Billion Hole” (Business Insider). “On Wednesday, Warner Bros. Discovery told investors its TV business was in free-fall, and that it would take a $9 billion writedown on those assets. On Thursday, it was Paramount's turn: The entertainment conglomerate, which is about to be acquired by David Ellison and a consortium of investors, just took a $6 billion charge on its TV business. For context: Public investors value all of Paramount's equity at $7 billion.”

“Not To Be Sniffed At: Dolce & Gabbana Launches Luxury Dog Perfume” (HNGN). “No need to wrestle your dog into the bath anymore. Italian luxury fashion house Dolce & Gabbana has launched a new perfume for canine companions. The ‘alcohol-free scented mist for dogs’ is on sale for 99 euros ($108 USD) and comes with a free collar -- but also a warning from animal rights activists, who say it could cause pets distress.”

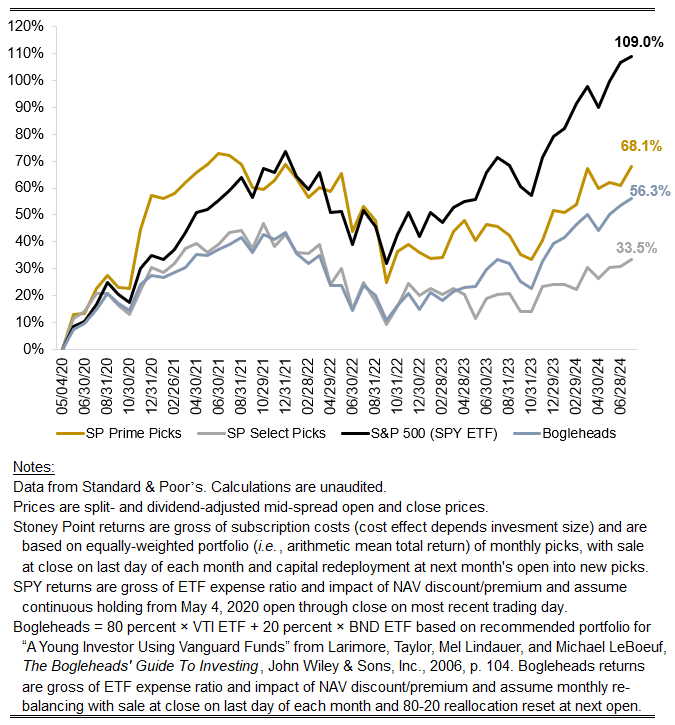

July (and June) performance update

Here with an overdue performance update (I was delayed in dealing with data provider issues for about a month or so — in short, IEX Cloud shut down its API for good).

For July:

Prime: +4.42%

Select: +2.06%

SPY ETF: +0.95%

Bogleheads Portfolio (80% VTI + 20% BND): +1.76%

For June:

Prime: -0.60%

Select: +0.14%

SPY ETF: +3.25%

Bogleheads Portfolio (80% VTI + 20% BND): +2.21%

June was another weak month for Prime and Select, but the rotation is July was notable and widely discussed. The AI megatrend driving the largest names in the S&P 500 seemed to deflate a bit and small-cap gains were explosive after years of weak returns relative to larger stocks. Those factors alone would not be likely to explain the outperformance of Prime and Select in July, but an improved outlook for value strategies more generally would.

August has been a bloodbath across U.S. equities so far, so let’s see how the rest of the month plays out.

Total Performance History

August picks available now

The new Prime and Select picks for August are available starting now, based on a model run put through Today (July 31). As a note, I will be measuring the performance on these picks from the first trading day of the month, Thursday, August 1, 2024 (at the mid-spread open price) through the last trading day of the month, Friday, August 30, 2024 (at the mid-spread closing price).

What we’re reading (7/30)

“It’s Not The End Of The World If The Fed Doesn’t Cut Rates Tomorrow” (CNN Business). “The Federal Reserve is all but certain to hold interest rates steady at its meeting this week. But a growing crowd of economists — among them, former Fed Vice Chair Alan Blinder and Nobel prize-winner Paul Krugman — are urging central bankers to cut now rather than at September’s meeting, when it is widely expected to do so.”

“Microsoft Has Investors Really Freaking Out About Big Tech’s AI Spending” (Business Insider). “Analysts had big expectations for Microsoft's cloud growth this quarter — and the tech giant seems to have fallen short of them even as it pumps money into its AI plans. Microsoft released its Q4 earnings Tuesday afternoon, and the company grew its Azure cloud unit's revenue by 29%. That came in slightly shy of Wedbush analysts' expectations for 30% growth in this ‘most important metric.’ Shares dropped in postmarket trading.”

“How YouTube Took Over Our Television Screens” (New York Times). “YouTube consistently ranks as the most popular streaming service on U.S. televisions, surpassing the companies it once tried to emulate. The platform’s unlikely ascent to the top of the leaderboard shows that more than a decade into the streaming era, the internet has continued to change the nature of TV and the habits of viewers.”

“OpenAI Rolls Out Voice Mode After Delaying It For Safety Reasons” (Washington Post). “OpenAI’s fans and customers have clamored for the voice mode, with some complaining online when the company delayed the launch in June. The new feature will be available to a small number of users at first, and the company will gradually open it up to all of OpenAI’s paying customers by the fall.”

“American Consumers Feeling More Confident In July As Expectations Of Future Improve” (Associated Press). “American consumers felt more confident in July as expectations over the near-term future rebounded. However, in a reversal of recent trends, feelings about current conditions weakened. The Conference Board, a business research group, said Tuesday that its consumer confidence index rose to 100.3 in July from a downwardly revised 97.8 in June. The index measures both Americans’ assessment of current economic conditions and their outlook for the next six months.”

What we’re reading (7/29)

“Investors On Alert For Fed Signals Of September Rate Cut” (Wall Street Journal). “The big question going into the Federal Reserve’s meeting Wednesday comes down to how strongly officials signal their desire to cut rates. The central bank is widely expected to hold its benchmark short-term interest rate steady—in a range between 5.25% and 5.5%, a two-decade high—while setting the table to begin a series of reductions at the next meeting in mid-September.”

“McDonald’s Earnings, Revenue Miss Estimates As Consumer Pullback Worsens” (CNBC). “Company executives acknowledged that diners considered their prices too high and said that they are taking a ‘forensic approach’ to evaluating value offerings and working with franchisees to make the necessary adjustments.”

“Texas Crude Oil Pipelines Full To The Brim, Getting Worse” (Bloomberg). “Crude oil pipelines connecting the busiest Texas oil fields to a critical export hub across the state are nearly out of space, threatening to cap US oil exports at a time when the world needs more.”

“Ethiopia Floats Its Currency In A Bid To Secure Loans” (Semafor). “Ethiopia’s government has allowed its currency to be traded on the open market instead of at a fixed rate as part of reforms aimed at securing loans from international lenders to stabilize its economy. The birr’s value against the dollar fell by 30% after it was allowed to float on Monday, said the country’s biggest lender, Commercial Bank of Ethiopia. Removing the central bank’s fixed rate is part of sweeping reforms aimed at easing the chronic shortage of foreign currency that have plagued its economy.”

“The Problem Of The Tariff In American Economic History, 1787–1934” (CATO Institute). “‘The pursuit of free trade as national policy in the United States predates the Constitution. Responding to a Spanish government inquiry in 1780, John Jay expressed the fledgling nation’s commitment to a principle of unimpeded exchange: “every man being then at liberty, by the law, to cultivate the earth as he pleased, to raise what he pleased, to manufacture as he pleased, and to sell the produce of his labor to whom he pleased, and for the best prices, without any duties or impositions whatsoever.’ Jay’s sentiments captured the Founding generation’s unease with Britain’s habit of manipulating its colonies’ trading patterns through political interventions—a stated grievance of the Declaration of Independence some four years prior.”

August picks available soon

I’ll be publishing the Prime and Select picks for the month of August before Thursday, August 1 (the first trading day of the month). As always, SPC’s performance measurement for the month of August, as well as SPC’s cumulative performance, will assume the sale of the July picks at the closing price (at the mid-point of the closing bid and ask prices) on the last trading day of the month (Wednesday, July 31). Performance tracking for the month of August will assume the August picks are bought at the open price (at the mid-point of the opening bid and ask prices) on the first trading day of the month (Thursday, August 1).

What we’re reading (7/22)

“Nike Is In Trouble. Can the Olympics Save It?” (Newsweek). “Nike is going for gold this summer as an official supplier for Team USA's competition uniforms for the Paris 2024 Olympic following a string of problems with the company, including poor financial performance, job cuts and criticism over its products. The sportswear brand took a kicking this spring for its Major League Baseball uniforms, with players complaining of color mismatches, see-through pants and fabric that changed after coming into contact with sweat.”

“Paul Singer Thinks There’s More That Sucks About Starbucks Than The Coffee” (Dealbreaker). “He may have been annoyed that the bacon-egg-and-gouda sandwich he’d been craving to go alongside cinnamon dolce latte was out of stock. Perhaps he popped in to one of a recent trip to China and noticed how empty it was compared the growing number of competing roasteries around it. That or, like founder Howard Schultz, he noticed that its stock was down by nearly a quarter this year and decided it was Starbucks itself rather than his own swimming head that required a pick-me-up.”

“The Spectacular Rise And Surprising Staying Power Of The George Foreman Grill” (The Hustle). “This year marks the 30-year anniversary of the grill, officially known as the George Foreman Lean Mean Fat Reducing Grilling Machine. After a slow start, it became an indelible part of ‘90s consumer culture and the world’s most popular product for cooking hamburgers, hot dogs, salmon, and just about everything else (Oprah Winfrey preferred it for bacon).”

“Global Computer Collapse Is A Chilling Look At What’s To Come” (New York Post). “In recent years, there have been an increasing number of widescale internet outages, whether from Amazon’s cloud platform collapsing, misconfigurations in fundamental network infrastructure, or actual hardware. The CrowdStrike outage was worse than any of these because it didn’t just hit the backbone of the internet, but individual endpoint computers, knocking out crucial services not just from a central failure, but by taking down everything it touches.”

“The 401(k) Rollover Mistake That Costs Retirement Savers Billions” (Wall Street Journal). “Workers miss out on billions in investment gains by pulling retirement savings out of the stock market after switching jobs—often without meaning to. When people roll 401(k) balances from their old company’s plan into an individual retirement account, the money is frequently held as cash until they select new investments. Many never do, according to new research from Vanguard Group. Nearly a third who rolled savings into IRAs at Vanguard in 2015 still had the balance sitting in cash seven years later.”

What we’re reading (7/21)

“A Stock Market Rotation Of Historic Proportions Is Taking Shape” (Wall Street Journal). “The stock market has suddenly turned upside down. The market’s laggards have sprung to life in recent days, while the seemingly impervious “Magnificent Seven” group of technology stocks has stumbled. Investors are even more focused than usual on corporate earnings as they try to anticipate what comes next. The Russell 2000 index of smaller stocks beat the S&P 500 over the seven days through Wednesday by the largest margin during a period of that length in data going back to 1986, according to Dow Jones Market Data. The Russell 1000 Value index, meanwhile, notched its biggest lead over its growth-stock counterpart since April 2001, after the dot-com bubble burst.”

“History Says The Wild Small-Cap Stock Rally Isn’t Going To Last” (Inc Magazine). “Small-cap stocks have been the big surprise in markets this month, fueled by a combination of rate cut expectations and rising odds for a second Trump presidency. That said, the group's blistering rally has fallen off as abruptly as it began. While the market's strength does seem to be broadening beyond mega-cap tech names, that does not mean small-caps will keep marching higher. From July 1 to July 16, the S&P 600 small-cap index recorded a 10.2 percent gain. In the last two days, however, the index fell about two percent.”

“RIP Hedge Fund Superstars” (Insider). “What is clear is that hedge funds run by an individual star, by one prodigious mind, are not raising the massive money they used to. Clients who once were proud to hand their money to a specific person are pushing back; they want to pay lower fees and see less-volatile returns. The funds that have survived rely on a stable of faceless traders testing out different ideas, brokering transactions, and harvesting the returns for the collective. Quant strategies — which are built on algorithmic trading — have also become more popular with the ultrawealthy. More robots, fewer people, lower overhead.”

“Apple Should Buy HBO” (Spyglass). “Two problems: Apple needs content, Warner Bros Discovery needs money. One solution: Apple has money, WBD has content. Come on folks, this isn't rocket science. It's not any kind of science. It's business. Well, as much as show business actually is still a legitimate business. A distinction which seems tenuous at best for most companies these days.”

“Costs From The Global Outage Could Top $1 Billion – But Who Pays The Bill Is Harder To Understand” (CNN Business). “Experts largely agree it’s too early to get a firm handle on the price tag for Friday’s global internet breakdown. But those costs could easily top $1 billion, said Patrick Anderson, CEO of Anderson Economic Group, a Michigan research firm that specializes in estimating the economic cost of events like strikes and other business disruptions.”

What we’re reading 7/20

“Where Do Economists Think We’re Headed? These Are Their Predictions” (Wall Street Journal). “The Wall Street Journal’s latest quarterly survey of business and academic economists shows forecasters remain firmly optimistic about the economic outlook, despite some hints of weakness in recent data.”

“Can Value Stocks Really Make A Comeback?” (Morningstar). “For value stock investors, 2024 looked like another “Wait ‘til next year” scenario, with mega-sized technology stocks driving the market higher. However, after months of lagging behind growth stocks (especially those riding the artificial intelligence wave), value stocks surged ahead this past week. A prime catalyst came from geopolitical concerns threatening the AI-driven boom in semiconductor stocks. At the same time, growing confidence that Federal Reserve rate cuts are finally on their way has the potential to make the dividends offered by many value stocks more attractive.”

“‘Greatest Bubble’ Nearing Its Peak, Says Black Swan Manager” (Wall Street Journal). “‘[Universa Investments’ Mark] Spitznagel predicts an even worse shakeout than a quarter-century ago because the excesses are more extreme—the “greatest bubble in human history.’ High public indebtedness and valuations make a Washington-led rescue harder to pull off. He sees today’s benign slowdown in inflation overshooting and says the U.S. economy could enter a recession by the end of the year.”

“What Presidential Election? So Far, The Stock Market Doesn’t Care.” (New York Times). “The stock market…is remarkably indifferent to the nation’s political fortunes. On Monday there were big moves in stocks perceived as benefiting from a Trump presidency, but that exuberance didn’t last. Instead, the market seems to be focused on issues that have little to do with politics, like the possibility of a Federal Reserve rate cut, heartening corporate earnings reports or the allure of artificial intelligence stocks.”

“Microsoft’s Global Sprawl Comes Under Fire After Historic Outage” (Washington Post). “A cascading computer outage that grounded planes, stymied hospitals and disrupted critical public services exposed the depth of the global economy’s dependence on a single company: Microsoft. Regulators and lawmakers across the political spectrum raised alarm that the sprawling outage that knocked out Windows showcases the danger of so much power concentrating into one firm, which drives governments, businesses and critical infrastructure around the world.”

What we’re reading (7/15)

“Powell Indicates Fed Won’t Wait Until Inflation Is Down To 2% Before Cutting Rates” (NBC News). “Federal Reserve Chair Jerome Powell said Monday that the central bank will not wait until inflation hits 2% to cut interest rates. Speaking at the Economic Club of Washington D.C., Powell referenced the idea that central bank policy works with ‘long and variable lags’ to explain why the Fed wouldn’t wait for its target to be hit.”

“Stock Dudes Risk A Market Wipeout” (Wall Street Journal). “The wave that broke was the momentum trade, which had pushed the ‘Magnificent Seven’ megacapitalization stocks and anything related to artificial intelligence to dizzying heights, leaving the rest of the market far behind. The question for investors now is whether the breakers will hit the rocks, or merely prove to be white caps far from the shore. Is the megacap trade over?”

“Unearthed 1980s Bill Gates Interview Features The Microsoft Founder Talking About The Earliest Iterations Of AI” (Business Insider). “‘Another thing that we're trying to get the computer to do is learn,’ Gates said in the interview. ‘That is, after you've used it for a while, then you'll be able to refer back to something you've done previously so you don't have to repeat those commands.’ He added that the computer will be able to recognize mistakes the same way ‘a human coworker might and aid you in the working process with the machine.’”

“As Policy Types Cheer the Demise Of ‘Inflation,’ Inflation Arrives” (Forbes). “Here lies the error, one of many, in using market prices as a proxy for what is always and everywhere a currency phenomenon. As has been said here over and over again, and for years, there’s an ocean of difference between rising prices and inflation. Inflation is a shrinkage of the monetary measure, in our case the dollar. Higher prices are at best a consequence of the inflation.”

“How Janet Yellen Became An Unlikely Culinary Diplomat” (New York Times). “There was mayonnaise mixed with ants at a gastronomic taqueria in Mexico City. The garlic at a Persian restaurant in Frankfurt was aged 25 years. And, yes, the magic mushrooms in Beijing were hallucinogenic. This isn’t an Anthony Bourdain travel show but rather a taste of what Janet L. Yellen, the Treasury secretary, has been eating on the road over the more than 300,000 miles she has logged over the last three years as she has been grappling with inflation and devising new ways to cripple the Russian economy.”

What we’re reading (7/14)

“Robert Putnam Knows Why You’re Lonely” (New York Times). “I think we’re in a really important turning point in American history. What I wrote in ‘Bowling Alone’ is even more relevant now. Because what we’ve seen over the last 25 years is a deepening and intensifying of that trend. We’ve become more socially isolated, and we can see it in every facet in our lives.”

“‘Dollarization’ In Argentina Isn't A Policy Choice, It’s A Market Condition” (RealClear Markets). “With money that’s actually used by producers, the simple, unspoken truth is that its circulation is production determined. Where there’s production there’s always “money” facilitating the movement of production as though placed there by an invisible hand. And where production is slight, there’s very little money as a reflection of scant production.”

“What If The A.I. Boosters Are Wrong?” (DealBook). “[MIT economist Daron] Acemoglu concluded that A.I. would contribute only “modest” improvement to worker productivity, and that it would add no more than 1 percent to U.S. economic output over the next decade. That pales in comparison to estimates by Goldman Sachs economists, who predicted last year that generative A.I. could raise global G.D.P. by 7 percent over the same period.”

“Pork Producer Smithfield Plans U.S. Stock Listing” (Wall Street Journal). “The Chinese parent of Smithfield Foods says it plans to take the pork company public in the U.S. WH Group, the world’s largest pork-producing company by sales, said Sunday it plans to float Smithfield’s business in the U.S. and Mexico on the New York Stock Exchange or Nasdaq.”

“Global Markets Ramp Up The ‘Trump Trade’ After Rally Attack” (Yahoo! Finance). “The series of wagers — based on anticipation that the Republican’s return to the White House would usher in tax cuts, higher tariffs and looser regulations — had already been gaining ground since President Joe Biden’s poor performance in last month’s debate imperiled his re-election campaign. But the trades were expected to take deeper hold, with Trump galvanizing supporters and drawing sympathy by exhibiting defiant resilience after being shot in the ear on stage at a Pennsylvania rally.”

What we’re reading (7/13)

“A Beautiful Inflation Report” (New York Times). “One of my go-to economic data experts emailed on Thursday morning about the latest inflation report, which showed prices actually falling in June and up only 3 percent over the past year. It was, he declared, ‘beautiful.’ Your aesthetic sense may vary, but we’ve now had two months of really good price data, enough to puncture the bubble of pessimism that, um, inflated early this year. And the implications of the good news are pretty big.”

“Big Banks And Customers Continue To Feel Pressure From Higher Rates” (Wall Street Journal). “The fight to rein in inflation continues to weigh on some of the nation’s largest banks. Higher interest rates crimped their profits and left more consumers struggling to keep up with elevated borrowing costs.”

“Jane Fraser Is Trying To Pull Chronically Struggling Citigroup Out Of The Gutter. She May Actually Pull It Off” (CNN Business). “Fraser, the first woman ever to run a Wall Street bank, inherited a behemoth that had become a laughingstock among its peers, hobbled by its unwieldy bureaucracy, a bloated staff and slim profit margins…But lately, to the surprise of Citi’s critics, things are looking up. Since September, when Fraser laid out her vision for a more streamlined Citigroup, the bank’s stock has shot up more than 50%.”

“Wall Street Is Bullish On Stocks For The 2nd Half Of The Year. Here Are Each Firm’s Exact Forecasts.” (Business Insider). “The S&P 500 has soared this year, with the index jumping about 15% to record highs in the first half. With the second half of 2024 underway, Wall Street strategists are updating their year-end price targets for the S&P 500, and nearly all of them are leaning bullish as they increase their forecasts.”

“The Class Gap In Career Progression: Evidence From US Academia” (Anna Stansbury & Kyra Rodriguez). “Unlike gender or race, class is rarely a focus of research or DEI efforts in elite US occupations. Should it be? In this paper, we document a large class gap in career progression in one labor market: US tenure-track academia. Using parental education to proxy for socioeconomic background, we compare career outcomes of people who got their PhDs in the same institution and field (excluding those with PhD parents). First-generation college graduates are 13% less likely to end up tenured at an R1, and are on average tenured at institutions ranked 9% lower, than their PhD classmates with a parent with a (non-PhD) graduate degree. We explore three sets of mechanisms: (1) research productivity, (2) networks, and (3) preferences. Research productivity can explain less than a third of the class gap, and preferences explain almost none. Our analyses of coauthor characteristics suggest networks likely play a role. Finally, examining PhDs who work in industry we find a class gap in pay and in managerial responsibilities which widens over the career. This means a class gap in career progression exists in other US occupations beyond academia.”

What we’re reading (7/10)

“An Exodus Of Investors Is Underway At Index Ventures On The Back Of A $2.3 Billion Fundraise” (Business Insider). “From the outside, things are looking rosy at Index Ventures. This week, the 28-year-old venture capital firm debuted a new pair of funds totaling $2.3 billion, a substantial sum during an abysmal time for the industry's fundraising efforts. However, a series of departures at the firm paints a darker picture of Index's state. Last week, the firm parted ways with five investors in its San Francisco office, including mid-level dealmakers and a senior dealmaker, according to four people familiar with the matter. The turnover came during management's midyear check-ins with staff.”

“Zucker Unbound! CBS News Change, Paramount Sale Points Former CNN Chief To Tiffany Network” (Showbiz 411). “Jeff Zucker is coming back! Sources tell me that today’s announcement that CBS News chief Ingrid Cipirian-Matthews is gone probably means one thing: the return of Jeff Zucker. What’s going on here? … in all likelihood, Ellison has purchased Paramount. And [Jeff] Shell [former NBC Universal chairman] is advising him. First project: give CBS some pizzazz with Zucker.”

‘“I’m Not Naive’: Inside Emma Tucker’s Rocky Wall Street Journal Reboot” (Vanity Fair). “Tucker, a personable and somewhat irreverent Brit, took over the Journal in February 2023. In a little over a year, the 57-year-old journalist has brought color, voice, and a renewed metabolism to America’s business newspaper of record. Sure, you’ll still find stories about interest-rate cuts and investment income. But you’ll also find investigations into Elon Musk’s unusual relationships with women at SpaceX and drug use, the succession battle for the luxury empire LVMH, and messages that Hamas military leader Yahya Sinwar sent to compatriots and mediators. (An attorney for Musk told WSJ that he’s never failed a drug test at SpaceX.) Tucker’s goal is to make the paper ‘audience-first’ and ‘to grow and retain subscribers,’ she told me. It might not sound like the most visionary mission. But the Journal today is, well, better—a more compelling product that a wider swath of people might pick up and read.”

“Costco Hikes Membership Fee For The First Time Since 2017” (CNBC). “The membership-based warehouse club said Wednesday that it will increase its membership fee by $5 in the U.S. and Canada as of Sept. 1. That is an increase to $65 from $60 for annual memberships. Its higher-tier plan, called ‘Executive Membership,’ will increase to $130 a year from $120.”

“The Age Question Looms Over America’s Bosses” (Wall Street Journal). “Leadership and cognitive decline are pressing issues throughout America’s aging workforce. High-powered professionals increasingly work past traditional retirement ages, even as ageism pushes others to leave careers early. There will be twice as many workers 75 and older in 2030 as there were in 2020, the Bureau of Labor Statistics projects.”